A Review of Global Reporting Initiative (GRI) Research with Sustainability Reporting: 1999-2020 dataset

ABSTRACT

Using a bibliometric analysis, this study evaluated 955 published documents retrieved from the Scopus database to find a research review structure on GRI with sustainability topics from 1999 to 2020 by utilizing the bibliometric package in VOSviewer and Harzing's Publish or Perish. This paper examined the most effective journals, authors, countries, institutions, subject area, keywords, citation, co-authorship, co-citation, bibliographic coupling, and co-occurrences networks. Also, this paper demonstrated the intellectual structure of the research and perceived obstacles to growth in the literature. The results show that the trend of publications has been growing over the past 20 years. This study offers a comprehensive understanding and publication of past studies trends and suggests that it will be a much greater number of articles in this field over the next decade which help the future direction of researchers in this area.

Keywords: Global Reporting Initiative (GRI); Sustainability reporting; Bibliometric analysis; Bibliographic; Scopus; Citation.

JEL classification: M140; M410.

Una revisión de la investigación de Global Reporting Initiative (GRI) con informes de sostenibilidad: conjunto de datos 1999-2020

RESUMEN

Este trabajo tiene como objetivo identificar las principales áreas de estudio en la investigación de Global Reporting Initiative (GRI). Mediante un análisis bibliométrico, este estudio evaluó 955 documentos publicados recuperados de la base de datos Scopus para encontrar una estructura de revisión de la investigación sobre GRI con temas de sostenibilidad desde 1999 hasta 2020 utilizando el paquete bibliométrico de VOSviewer y Publish or Perish de Harzing. Este trabajo examinó las revistas, autores, países, instituciones, área temática, palabras clave, citación, coautoría, co-citación, acoplamiento bibliográfico y redes de co-ocurrencias más eficaces. Asimismo, este trabajo demostró la estructura intelectual de la investigación y los obstáculos percibidos para el crecimiento de la bibliografía. Los resultados muestran que en los últimos 20 años la tendencia de las publicaciones ha ido en aumento. Este estudio ofrece una comprensión global y la publicación de las tendencias de los estudios anteriores y sugiere que habrá un número mucho mayor de artículos en este campo durante la próxima década.

Palabras clave: Global Reporting Initiative (GRI); Informes de sostenibilidad; Análisis bibliométrico; Bibliografía; Scopus; Citas.

Códigos JEL: M140; M410.

1. Introduction

Sustainability or sustainable development is an attitude for creating corporations' long-term value by concentrating on the social, environmental, and economic roles of organizations' activities (Carolina et al., 2016; Ashrafi et al., 2020). In this concept, corporate sustainability reporting or corporate social responsibility (CSR) reporting is a potential way of generating information on sustainability issues (Hedberg & Von Malmborg, 2003; Veronica et al., 2019). Since sustainability reporting deals with organizational performance, it can be a crucial part of the company's strategy (Niemann et al., 2017; Paun, 2018; E-Vahdati et al., 2019).

According to KPMG (2017), there is an upward trend in publishing sustainability reports by companies that make these reports mainstreams of their business practices. Besides, the growing concern of sustainability issues has led to an increasing level of attention to an organization's environmental, social, and governance (ESG) practice. Subsequently, more and more companies practice ESG information to improve their images as socially and environmentally responsible members of society (Surroca et al., 2010; Garcia et al., 2017). ESG practice provides additional information to gauge the company's performance rather than financial data (Eccles et al., 2011). However, the sustainability issues become more vital after the introduction of several initiatives such as the Global Reporting Initiatives (GRI), the Paris Agreement on Climate Change, the UN Principles for Responsible Investments (PRI), the UN Sustainable Development Goal (SDG), and guidelines on Climate-related Financial Disclosures issued by the Financial Stability Board Task Force (TCFD) (Wan-Hussin et al., 2021). These initiatives portrayed the importance of a socially responsible and environmentally friendly business model. Therefore, internal and external stakeholders expect companies to provide more reliable sustainability reports by following national and international standards.

One of the prominent guidelines for sustainability reporting is the GRI. These guidelines are provided through an organization with a non-profit and multiple-stakeholder characteristic that supports environmental, social, and governance parts of business activities (Initiative, 2016). The GRI framework was established in 1997 with the cooperation of the United Nations Global Compact (Rasche, 2009). GRI provides the world's most widely used standards on sustainability reporting and disclosure (E-Vahdati et al., 2018). Sustainability reports which use GRI guidelines are more credible than non-use GRI frameworks, and suitable to communicate with stakeholders and investors (Dawkins 2004; Boiral & Henri, 2017; Fernández-Gago et al., 2018). GRI breakdowns its guideline as follows: G1, GRI G2, GRI G3, GRI G3.1, GRI G4, and GRI Standards. The latest GRI guideline (GRI Standards) were published in 2016 which included all the main concepts and practices from the GRI G4 guidelines, developed with explicit requirements, a more flexible structure, and simpler language (Initiative, 2016). Besides, GRI Standards are enhanced by the Global Sustainability Standards Board (GSSB) which requires companies to report publicly their business activities and confirm their ability to enhance sustainable development (Initiative, 2012).

There is considerably abundant research that has been conducted concerning GRI as the first issued guidelines related to sustainability and the environment. This area has attracted researchers due to the importance of GRI disclosure towards the organization. For example, a recent study by Danisch (2021) found a positive relationship between environmental performance and environmental disclosure extent using GRI guidelines, whereby companies signal their environmental performance by increasing the extent of their reporting. Further, De Klerk et al. (2015) applied the GRI guidelines in their research and concluded that CSR disclosure provides incremental value-relevant information to investors beyond financial accounting information. On the other hand, Nguyen (2020) showed a negative significant association between firm value and a firm's GRI adherence level in reporting sustainability performance, which implies a higher adherence to GRI of firm sustainability reporting, the lower value of a firm share. Besides, Weber (2018) concluded that there were no differences in the cost of equity capital among CSR disclosers based on GRI disclosure level. It is evident that poor CSR performers, especially those reporting at the highest GRI disclosure levels, obtain the greatest cost of equity capital benefit associated with external assurance. On a different note, Knebel & Seele (2015) investigated GRI reporting challenges such as completeness, quality by disclosure frequency, and accessibility of the lack of provision of transparency toward GRI. The ongoing debates on GRI reporting, especially related to sustainability reporting motivate us to conduct a bibliometric analysis on this research area.

There has been an interesting trend in the publication of bibliometric review papers (eg., Baker et al., 2020; Petera & Wagner, 2015) which is missing in this field of study. Bibliometric reviews contribute maximum publications by offering a comprehensive evaluation of publication trends and patterns (Martínez-López et al., 2018), and identifying prominent scholars, documents, countries, and institutions. Additionally, the bibliometric analysis visualises the research field objectively through clustering and citation patterns of related documents (Vogel, 2012). Previous studies such as Petera & Wagner (2015) limited their keyword analysis on "Global Reporting Initiative" to review studies, whereas Kulevicz et al. (2020) restricted their bibliometric review in this area to a limited number of articles based on ScienceDirect. Our bibliometric review provides multiple contributions to the literature. First, it expands previous review studies through implementing the Scopus database and using the keyword of "GRI" or "Global Reporting Initiative" and "Sustainability" or "ESG" or "CSR" or "Corporate Social Responsibility". Second, this study utilizes a huge number of bibliometric analyses through different software and techniques to find more accurate and in-detail results. Third, there are a limited number of review studies on GRI, and to the best of our knowledge, this is the first review research concentrating on GRI for sustainability reports papers and analyse them with multiple techniques. The purpose of our bibliometric review is to identify and analyse descriptively publication patterns, and intellectual structures on GRI research for sustainability reporting. Our review addresses the following research objectives (ROs):

To examine the volume and growth of publication trends in GRI with sustainability reporting research based on years, countries, journals, authors, and institutions.

To understand the citation structure of research articles, journals, and countries in GRI with sustainability reporting research.

To investigate the most popular influential subject areas in GRI with sustainability reporting research among researchers.

To evaluate the influential keywords in GRI with sustainability reporting research.

To evaluate the most effective authors in GRI with sustainability reporting research.

To provide the intellectual structure in GRI with sustainability reporting research.

We employed quantitative bibliometric analysis to identify 955 Scopus-indexed documents related to GRI with sustainability reporting articles published from 1999 to 2020. We identified and analysed the extracted information from the Scopus database and documents, and examined patterns and trends of the current status of studies. The rest of our review is organized as follows. Section 2 provides a literature review on the overview of bibliometric analysis and previous studies related to GRI. Section 3 presents the methods that are conducted in this study, and section 4 shows the results. The discussion and implications are presented in section 5, and lastly, Section 6 concludes the paper with limitations and the recommendation for future research.

2. Literature review

2.1. Bibliometric analysis

A bibliometric analysis is a statistical method to quantitatively assess previous studies' growth trends through multiple domains (Rehn et al., 2007; Liao et al., 2018). Specifically, bibliometric analysis has been introduced in sustainability reports with links to global standards reviews such as Journal of Cleaner Production (Dos Santos et al., 2017; Pang & Zhang, 2019), Environmental Reviews (Kulevicz et al., 2020), Meditari Accountancy Research (Di Vaio et al., 2020), and European Financial and Accounting Journal (Petera & Wagner, 2015). There are three different classifications for bibliometric review indicators, including quantity, quality, and structural (Durieux & Gevenoi, 2010). Therefore, the productivity of publication trends is evaluated through quantity indicator, authors output is analysed through qualitative indicators, and finally, the association between publications and researchers (co-authorship, co-citation, and bibliometric coupling analysis) is referred to as structural indicator (Van Eck & Waltman, 2017). This review study gives an insight into the GRI with sustainability reporting literature leading to find and evaluate patterns and tendencies in the literature.

2.2. Past studies

Due to the importance of GRI guidelines in sustainability reporting, the number of studies related to this field of research has been increased dramatically in recent years (eg. Ballou et al., 2018; Şahin & Çankaya, 2020). Therefore, there is some bibliometric analysis in this field to document patterns for publication, authors, and the intellectual structure of current research. Table 1 depicts some of the recent studies that used bibliometric reviews concerning sustainability, CSR, or GRI in their topics, abstracts, and titles. Petera & Wagner (2015) utilized the keyword "global reporting initiative" for their review during the 2002-2014 period. They used 172 articles from Web of Science to document highly cited journals, quantities of articles and citations, influential authors, and co-citation analysis. The authors stated that the amount of literature dealing with GRI guidelines is growing. Moreover, Dos Santos et al. (2017) examined the status of sustainability and hotel business with GRI guidelines. They evaluated their review based on the Scopus database within three years from 2010 to 2012. The authors conducted their bibliometric analysis based on the frequency of keywords, publication trends, and sustainability criteria. While, Sikacz (2017) mapped the article on CSR reporting as an object of bibliometric analysis of scientific publications that they gathered information from the Web of Science database during 1995-2016 by presenting the source titles, publication growths, effective authors, and distribution of keywords for 341 papers. Besides, Pang & Zhang (2019) found environmental sustainability of 989 environmental sustainability-related papers from the Web of Science, SCI, and SSCI for 28 years. They examined their keywords based on the frequency of keyword, co-word, and clustering analysis. Moreover, Kulevicz et al. (2020) presented the bibliometric review of 53 papers from the ScienceDirect database. The authors analysed their sample in terms of publication frequency and keyword distribution from 2012 to 2017. They concluded that the latest hot topics in sustainability reporting research are related to GRI guidelines. Di Vaio et al. (2020) conducted the bibliometric analysis and content analysis on the 60 documents published in google scholar from 1990 to 2019 with keywords such as integrated thinking and reporting through the frequency of citations, clustering, and keyword distribution. Further, based on the current literature, very few review papers have used Scopus as the main source of data for bibliometric analysis. Thus, we utilize our review paper based on the Scopus data source on the term of GRI with sustainability reports.

Table 1. Past studies on bibliometric review

| Author | Domain search | Data source & scope | TDE | Bibliometric/review attributes examined |

|---|---|---|---|---|

| Petera & Wagner (2015) | "global reporting initiative" | Web of Science (2002-2014) | 172 | Co-citation analysis Highly cited journal Number of articles Number of citations High-productive authors |

| Dos Santos et al. (2017) | “Hotel”, “Planning”, “Sustainability” | Scopus (2010-2012) | 219 | Frequency of Keywords Types of publication Sustainability criteria |

| Sikacz (2017) | “corporate social responsibility report”, “integrated report”, “sustainability report*, “CSR report” | Web of Science (1995-2016) | 341 | Type of publications Source title Distribution of the authors Clustering analysis Frequency of keywords |

| Pang & Zhang (2019) | “green manufactur”, “sustainable manufactur”, “benign manufactur”, “environmentally conscious manufactur”, “environmentally responsible manufactur” | Web of Science SCI and SSCI journals (1970 to 2018) | 989 | Co-word analysis Clustering analysis Frequency of keywords |

| Kulevicz et al. (2020) | “Sustainability Report (SR)”, “Corporate Sustainability (CS)”, “Triple Bottom Line (TBL)” “Eco-innovation in business (ECO)”, “Global Reporting Initiative (GRI)” | ScienceDirect (2012-2017) | 53 | Publication frequency Keywords distribution |

| Di Vaio et al. (2020) | “Integrated thinking”, “sustainable development goals”, “Integrated reporting”, “sustainable business model”, | Google Scholar (1990-2019) | 60 | Frequency of citations Citation network and Clustering Keywords distribution Content analysis |

Note: TDE= Total Documents Examined

3. Methodology

3.1. Identification of sources

We conducted our bibliometric analysis based on the Scopus database in August 2020 since the Scopus database is termed a comprehensive abstract and citation database (Dos Santos et al., 2017) We followed a broader search strategy by conducting article titles, abstracts, and keywords with our search string. The Boolean strings selected are "GRI" or "Global Reporting Initiative" and ("Sustainability" or "ESG" or "CSR" or "Corporate Social Responsibility"). Our search string strategy is constructed to capture several facets as follows: year, author name, subject area, document type, source title, publication stage, keyword, affiliation, country, source type, and language. Having identified 976 documents between 1999 and mid-2020, we then excluded undefined, survey, note, editorial, conference review, a letter from document type, and reached final results of 955 documents. Table 2 presents our search string and data retrieval process.

Table 2. Search strategy and data retrieval process

| Date | Database | Search String |

|---|---|---|

| 3 August 2020 | Scopus (1999-2020) | TITLE-ABS-KEY("GRI" or "Global Reporting Initiative" and ("Sustainability" or "ESG" or "CSR" or "Corporate Social Responsibility") |

| Results | 976 documents | |

| Filter applied | Document Type: Article, Conference Paper, Book Chapter, Review | |

| Final Result | 955 documents | |

3.2. Methods

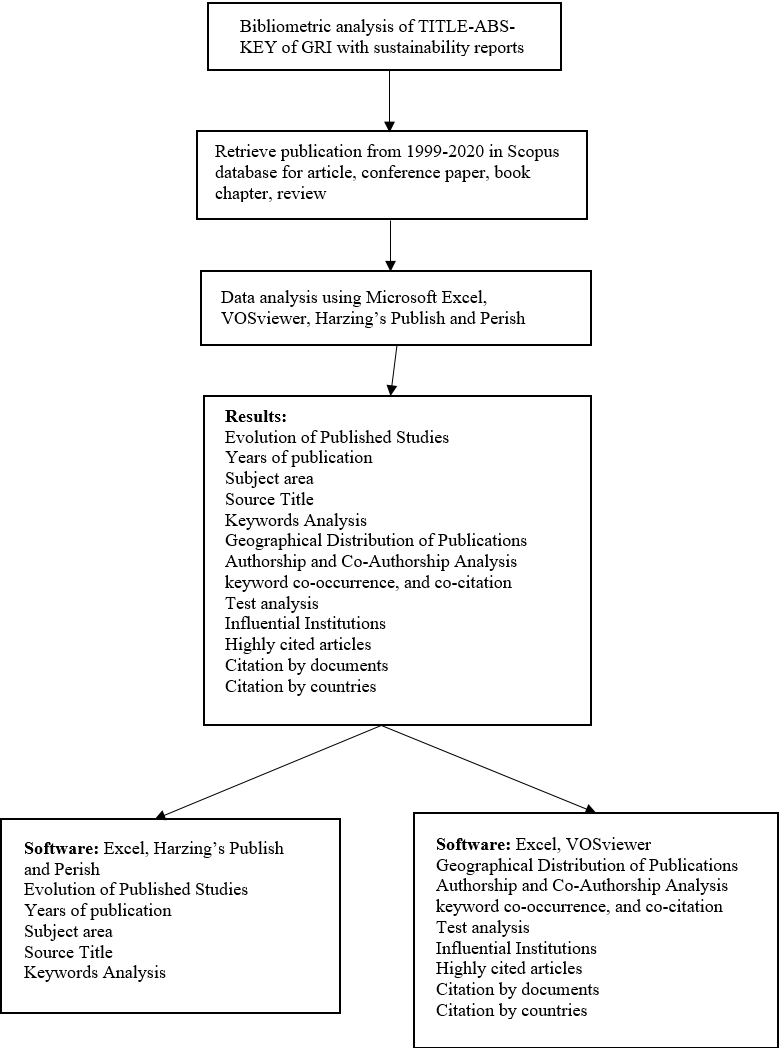

Research activity points out the shape of scientific work (Ronda-Pupo, 2017). Accordingly, the scientific field performs intellectual convergence concerning common patterns of referencing (Kessler, 1963). However, some previous studies such as Small (1973) believed that citation frequency displays common intellectual among cited and citing published papers. To conduct GRI with a sustainability research review, we used bibliometric analysis through using tools such as citation analysis, co-citation analysis, keyword co-occurrence analysis, and co-authorship analysis to respond to our research objectives (Castriotta et al., 2019). Co-authorship shows the authorship pattern and association among authors (Koseoglu, 2016). Besides, keyword co-occurrence displays the conceptual concept of previous studies (Callon et al., 1983). Co-citation analysis has also been used as the basis for the 'visualization of similarities (VOS), a powerful approach to network mapping (Van Eck & Waltman, 2014). Co-citation analysis assumes that when two scholars are frequently 'cited together' by other authors, they tend to share a similarity in theoretical perspective (White & McCain, 1998). Author co-citation analysis was performed by VOSviewer network socialization map which visualizes similarities among the authors in the past studies (Van Eck & Waltman, 2014). We used three software packages to structure our review papers: 1) Microsoft Excel to evaluate publication characteristics with proper charts/graphs (Persson et al., 2009); 2) VOSviewer to construct and visualizing the bibliometric network, and to perform co-authorship, and the co-occurrence of all keywords (Van Eck & Waltman, 2014); 3) Harzing's Publish and Perish to calculate the citations, h-index and g-index (Harzing, 1997). Figure 1 depicts the flowchart of our bibliometric study.

Figure 1. The flowchart of bibliometric analysis in GRI with sustainability research

4. Results

The findings and results of our bibliometric review on GRI with sustainability reports research for the period from 1999 to mid-2020 based on documents indexed in the Scopus database will be shown in the following sections. It covers publication trends, citation analysis, subject area analysis, keywords analysis, authorship and co-authorship analysis, and co-citation analysis, and bibliographic coupling among authors.

4.1. Publication Trend

To respond to the requirements for RO1 (to examine the volume and growth of publication trends in GRI with sustainability reporting research based on years, countries, journals, authors, and institutions), this study employs publication trends in this field and presents the results in different tables.

4.1.1. Publication by year

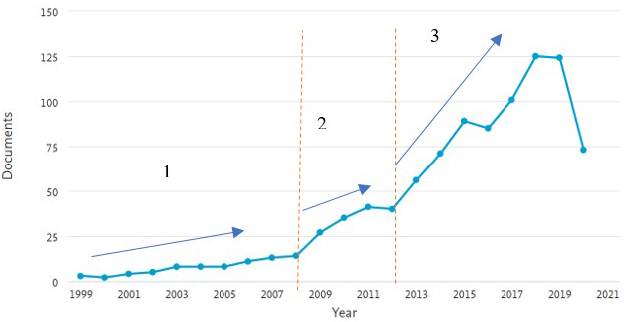

Figure 2 shows the descriptive trend of publication by year. After applying a filter for document types, we used 955 over the past 20 years to answer our research questions. Our first research objective (RO1) sought to reveal the trend trajectory for this purpose. We divided the growth pattern of the publication into three phases. As GRI launched in 1997, the number of published documents emerged slowly during the first decade with only 14 documents (phase 1). Interests in using GRI guidelines in sustainability reporting increased slowly in phase two as the number of documents reached 40 until 2012 but picked up the pace with the publication of 126 documents from 2013 until 2019 (phase 3). As a whole, 811 documents of the literature have been published from 2013 up to current which leads to the conclusion that the publication quantity and reputation in this field of research is progressing.

Figure 2. The growth pathway of GRI with sustainability reporting publications (n= 955)

4.1.2. Publication by country

Over the last 20 years, documents published in GRI with sustainability topics have been contributed from 77 geographical distributions. Accordingly, Table 3 shows the top 20 countries ranked by total publication (TP), total citation (TC), and h-index during 1999-2020. A huge number of publications have been originated from Anglo-American countries. The United States leads the list of countries that published in GRI-sustainability reporting documents with the largest TP (132) and TC (3500), followed by Spain (TP=119, TC=2746), Australia (TP=74, TC=3085), and Italy (TP=71, TC=1961). One of the reasons that many European countries such as Spain, Italy have a high publication in sustainability reporting is due to the United Nations's 2030 Agenda for sustainable development Goals (SDGs) (United Nations, 2020a; 2020b). UN sustainable development goals articulate the major issues facing humanity and aim to enhance health equality, education, and economic growth. The Spanish government will dream of achieving SDGs and therefore it is at the heart of its action. However, Poland is ranked as the 20th productive country in this field of research (TP=18, TC=120). According to Kostrzewa & Piasecki (2009) and López-Arceiz et al. (2020), the EU's Sustainable Development Strategy is implemented in the member states, including Poland, by other EU programs due to their obligatory character regarding sustainability development. Meanwhile, the United States ranked first with the h-index up to 33, while Spain ranked second with the h-index of 28, and Australia and Italy with h-index=24 ranked, as the third countries.

Table 3. The top 20 countries

| Country | TP | TC | h |

|---|---|---|---|

| United States | 132 | 3500 | 33 |

| Spain | 119 | 2746 | 28 |

| Australia | 74 | 3085 | 24 |

| Italy | 71 | 1961 | 24 |

| United Kingdom | 68 | 3579 | 21 |

| Brazil | 59 | 417 | 9 |

| Germany | 49 | 1341 | 19 |

| Canada | 45 | 2799 | 21 |

| India | 41 | 477 | 8 |

| Indonesia | 36 | 148 | 6 |

| Netherlands | 30 | 1804 | 20 |

| Malaysia | 29 | 265 | 8 |

| Czech Republic | 26 | 151 | 6 |

| France | 26 | 540 | 10 |

| China | 24 | 260 | 8 |

| Greece | 22 | 293 | 9 |

| Portugal | 22 | 427 | 11 |

| South Africa | 19 | 306 | 8 |

| Austria | 18 | 387 | 8 |

| Poland | 18 | 120 | 6 |

Notes: TP=total number of publications; TC=total citations; h=h-index.

4.1.3. Publication by journal

Table 4 lists the highest number of articles on GRI with sustainability reports topics published in journals. The 955 documents appeared in 50 journals. Most actives' source titles are categorized based on TP, TC, publisher, Scopus Cite Score, SJR, and SNIP 2019. The leading journals are the Journal of Cleaner Production (TP= 51, TC= 3032), followed by Corporate Social Responsibility and Environmental Management (TP= 44, TC= 1532), Sustainability Switzerland (TP= 34, TC= 388), Journal of Business Ethics (TP= 27, TC= 2188), Social Responsibility Journal (TP= 21, TC= 138), and Sustainability Accounting Management and Policy Journal (TP= 19, TC= 379). The subject of GRI guidelines with sustainability mostly belongs to the area of Accounting and Management which matches the scope of interest of the listed journals well. Meanwhile, the highest Cite Score is related to the Journal of Cleaner Production Cite Score of 10.9. Moreover, the highest number of publishers produced in the top 20 journals is Emerald.

Table 4. The top 20 source titles

| Source Title | TP | TC | Publisher | Cite Score | SJR 2019 | SNIP 2019 |

|---|---|---|---|---|---|---|

| Journal of Cleaner Production | 51 | 3032 | Elsevier | 10.9 | 1.89 | 2.39 |

| Corporate Social Responsibility and Environmental Management | 44 | 1529 | John Wiley and Sons Ltd | 5.9 | 0.974 | 1.625 |

| Sustainability Switzerland | 34 | 388 | Multidisciplinary Digital Publishing Institute (MDPI) | 3.2 | 0.581 | 1.165 |

| Journal of Business Ethics | 27 | 2188 | Springer Nature | 7 | 1.972 | 2.7 |

| Social Responsibility Journal | 21 | 138 | Emerald | 2.5 | 0.429 | 1.02 |

| Sustainability Accounting Management and Policy Journal | 19 | 379 | Emerald | 3.8 | 0.672 | 1.161 |

| Acta Universitatis Agriculturae Et Silviculturae Mendelianae Brunensis | 11 | 97 | Mendelova Zemedelska a Lesnicka Univerzita v Brne | 0.7 | 0.167 | 0.338 |

| Accounting Auditing and Accountability Journal | 9 | 294 | Emerald | 4.9 | 1.459 | 1.879 |

| Accounting Forum | 8 | 710 | Elsevier | 4.9 | 0.953 | 1.401 |

| Business Strategy and The Environment | 8 | 185 | Wiley-Blackwell | 8.4 | 1.828 | 1.877 |

| Corporate Communications | 8 | 167 | Emerald | 2.2 | 0.627 | 0.765 |

| Ecological Indicators | 7 | 424 | Elsevier | 7.6 | 1.331 | 1.747 |

| Gestao E Producao | 7 | 17 | Universidade Federal de Sao Carlos | 0.8 | 0.209 | 0.459 |

| International Journal of Innovation Creativity And Change | 7 | 5 | Primrose Hall Publishing Group | 0.5 | 0.225 | 5.163 |

| Environmental Quality Management | 6 | 64 | Wiley-Blackwell | 0.8 | 0.205 | 0.359 |

| Espacios | 6 | 0 | Sociacion de Profesionales y Tecnicos del CONICIT | 0.5 | 0.215 | 0.33 |

| Corporate Environmental Strategy | 5 | 88 | Elsevier | NA | NA | NA |

| Corporate Ownership and Control | 5 | 10 | Virtus Interpres | 0.2 | 0.148 | 0.268 |

| International Journal of Sustainability In Higher Education | 5 | 169 | Emerald | 3.2 | 0.635 | 1.329 |

| Meditari Accountancy Research | 5 | 55 | Emerald | 5 | 0.954 | 1.472 |

Notes: TP=total number of publications; TC=total citations;

4.1.4. Publication by contributing author

Table 5 depicts the top 20 productive authors. García-Sánchez, I.M. from Universidad de Salamanca of Spain has the highest number of publications (13) and TC of 479 with 6 h-index, and 7 g-index on GRI-related topics with sustainability. It is followed by Boiral, O. from Université Laval of Canada with TP of 9, TC of 446, h-index of 84, and g-index of 9. Besides, the highest number of TC (627) in this field of research is related to Lozano from Hogskolan I Gavle of Sweden.

Table 5. The top 20 productive authors

| Author’s Name | Affiliation | Country | TP | TC | h | g |

|---|---|---|---|---|---|---|

| García-Sánchez, I.M. | Universidad de Salamanca | Spain | 13 | 479 | 6 | 7 |

| Boiral, O. | Université Laval | Canada | 9 | 446 | 8 | 9 |

| Lozano, R. | Hogskolan i Gavle | Sweden | 8 | 627 | 6 | 8 |

| Manetti, G. | Università degli Studi di Firenze | Italy | 8 | 482 | 6 | 8 |

| Nikolaou, I.E. | Democritus University of Thrace | Greece | 8 | 87 | 5 | 8 |

| Gallego-Álvarez, I. | Universidad de Salamanca | Spain | 8 | 222 | 5 | 7 |

| Issac, B. | University of Northumbria | United Kingdom | 7 | 35 | 4 | 5 |

| Modapothala, J.R. | Monash University Malaysia | Malaysia | 7 | 35 | 4 | 2 |

| Searcy, C. | Ryerson University | Canada | 7 | 457 | 6 | 7 |

| Skouloudis, A. | University of the Aegean | Greece | 7 | 123 | 4 | 7 |

| Trenz, O. | Mendelova univerzita v Brne | Czech Republic | 7 | 90 | 4 | 7 |

| Tsalis, T.A. | Democritus University of Thrace | Greece | 7 | 83 | 5 | 7 |

| Uyar, A. | La Rochelle Business School | France | 7 | 87 | 3 | 7 |

| Greiling, D. | Johannes Kepler University Linz | Austria | 6 | 35 | 2 | 5 |

| Farneti, F. | Alma Mater Studiorum Università di Bologna | Italy | 5 | 453 | 5 | 5 |

| García-Benau, M.A. | University of Valencia, Valencia | Spain | 5 | 124 | 4 | 5 |

| Hřebíček, J. | Institute of Biostatistics and Analysis | Italy | 5 | 53 | 3 | 2 |

| Rodríguez-Ariza, L. | Universidad de Salamanca | Spain | 5 | 24 | 3 | 4 |

| Alcaraz-Quiles, F.J. | Universidad de Granada | Spain | 4 | 48 | 3 | 4 |

| Bhatia, A. | Guru Nanak Dev University | India | 4 | 8 | 1 | 2 |

| Brown, H.S. | Clark University | United States | 3 | 451 | 3 | 3 |

Notes: TP=total number of publications; TC=total citations; h=h-index; and g=g-index.

4.1.5. Publication by institutions

Table 6 lists the top institutions in GRI with sustainability reporting topics between 1999 and 2020. As shown in the table, the Universidad de Salamanca is the most influential organization with 22 publications, while other research institutions with a large number of published documents contain Brazilian Universidade de Sao Paulo - USP (19), the Università degli Studi di Firenze from Italy (12), the University of Valencia from Spain (11), and Universidade Federal de Santa Catarina from Brazil (11). Spain has the most active research institutions in GRI- sustainability reporting research with 7 institutions from the top 20 influential organizations category (ranked 1, 4,6,9,12,18,19). The second-largest productive institutions in this field of research are Brazil and Italy. Meanwhile, the highest number of TC is related to Universidad de Salamanca from Spain (624) followed by Universidad Autónoma de Madridfrom Spain (524), Alma Mater Studiorum Università di Bologna from Italy (528), Università degli Studi di Firenze from Italy (497), and the Ryerson University from the United States (476). Further, the highest C/P of 66.38 is belonged to the University of Sydney from Australia, followed by Alma Mater Studiorum Università di Bologna from Italy (66), and Ryerson University from the United States (52.89). Concerning influential level, the Universidad de Salamanca of Spain is ranked at the top with an h-index of 12, followed by Universidad Autónoma de Madrid of Spain and Université Laval of Canada with an h-index of 8, and then the Ryerson University from the United States and Alma Mater Studiorum Università di Bologna of Italy with h-index of 7, and g-index of 8.

Table 6. The top 20 influential institutions with a minimum of five publications

| No. | Affiliation | Country | TP | NCP | TC | C/P | C/CP | h | g |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Universidad de Salamanca | Spain | 22 | 20 | 624 | 28.36 | 31.20 | 12 | 22 |

| 2 | Universidade de Sao Paulo - USP | Brazil | 19 | 11 | 169 | 8.89 | 15.36 | 5 | 13 |

| 3 | Università degli Studi di Firenze | Italy | 12 | 9 | 497 | 41.42 | 55.22 | 7 | 12 |

| 4 | University of Valencia | Spain | 11 | 11 | 149 | 13.55 | 13.55 | 6 | 11 |

| 5 | Universidade Federal de Santa Catarina | Brazil | 11 | 9 | 39 | 3.55 | 4.33 | 4 | 5 |

| 6 | Universidad Autónoma de Madrid | Spain | 11 | 11 | 524 | 47.64 | 47.64 | 8 | 11 |

| 7 | Université Laval | Canada | 11 | 9 | 431 | 39.18 | 47.89 | 8 | 11 |

| 8 | University of the Aegean | Greece | 10 | 9 | 145 | 14.50 | 16.11 | 5 | 10 |

| 9 | Universidad de Granada | Spain | 10 | 9 | 177 | 17.70 | 19.67 | 5 | 10 |

| 10 | Mendelova univerzita v Brne | Czech Republic | 9 | 9 | 97 | 10.78 | 10.78 | 5 | 9 |

| 11 | Ryerson University | United States | 9 | 9 | 476 | 52.89 | 52.89 | 7 | 9 |

| 12 | Universidad de Zaragoza | Spain | 8 | 6 | 414 | 51.75 | 69.00 | 5 | 8 |

| 13 | The University of Sydney | Australia | 8 | 6 | 531 | 66.38 | 88.50 | 5 | 8 |

| 14 | Alma Mater Studiorum Università di Bologna | Italy | 8 | 8 | 528 | 66.00 | 66.00 | 7 | 8 |

| 15 | Democritus University of Thrace | Greece | 8 | 7 | 87 | 10.88 | 12.43 | 5 | 8 |

| 16 | Swinburne University of Technology Sarawak Campus | Malaysia | 8 | 7 | 48 | 6.00 | 6.86 | 5 | 6 |

| 17 | Bucharest University of Economic Studies | Romania | 8 | 6 | 45 | 5.63 | 7.50 | 6 | 2 |

| 18 | Universidad del Pais Vasco | Spain | 7 | 7 | 135 | 19.29 | 19.29 | 6 | 7 |

| 19 | Universidad Pablo de Olavide | Spain | 7 | 5 | 351 | 50.14 | 70.20 | 4 | 7 |

| 20 | Helsingin Yliopisto | Finland | 6 | 6 | 109 | 18.17 | 18.17 | 6 | 6 |

Notes: TP=total number of publications; NCP=number of cited publications; TC=total citations; C/P=average citations per publication; C/CP=average citations per cited publication; h=h-index; and g=g-index.

4.2. Citation analysis

To accomplish RO2 which is related to the citation structure of research articles, journals, and countries in GRI with sustainability reporting research, we evaluated the top 20 highly-cited documents, journals, and countries with our dataset. This is complying with Tsay (2009) who stated that citations indicate influence. Table 7 presents the top 20 cited documents in our Scopus dataset between 1999 and 2020. Our analysis shows that Clarkson et al. (2008) received the highest citation (965 citations) for their study entitled "Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis/. The authors completely focused on discretionary environmental disclosures and developed a content analysis index with GRI guidelines to assess the extent of discretionary disclosures in CSR reports. Similarly, Azapagic (2004) received 532 citations and (33.25 citations per year) for his article with the title of "Developing a framework for sustainable development indicators for the mining and minerals industry". The author developed the sustainability (ESG) framework through GRI indicators as a tool for evaluating sustainable performance. Documents with higher citations have a stronger effect on the development of GRI with sustainability reports topics. Table 8 ranked the top 20 countries and journals which cited the topic of GRI with sustainability reporting studies. Based on our results, United Kingdom, United States, Australia, Canada, and Spain lead the list. Besides, European countries dominate this list as the EU's sustainable development strategy is implemented in the member states (López-Arceiz et al., 2020). In terms of top journals, we found Journal of Cleaner Production, Journal of Business Ethics, and Corporate Social Responsibility and Environmental Management have received more than 1500 citations each. The majority of these top 20 journals have accounting, sustainability, corporate governance as their main scope.

Table 7. The top 20 highly cited articles

| No. | Authors | Title | Year | Cites | Cites per Year |

|---|---|---|---|---|---|

| 1 | Clarkson, Li, Richardson, & Vasvari | Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis | 2008 | 965 | 80.42 |

| 2 | Azapagic | Developing a framework for sustainable development indicators for the mining and minerals industry | 2004 | 532 | 33.25 |

| 3 | Milne, Gray | W(h)ither Ecology? The Triple Bottom Line, the Global Reporting Initiative, and Corporate Sustainability Reporting | 2013 | 342 | 48.86 |

| 4 | Krajnc, GlaviÄ | A model for integrated assessment of sustainable development | 2005 | 295 | 19.67 |

| 5 | Gamerschlag, Möller, & Verbeeten | Determinants of voluntary CSR disclosure: Empirical evidence from Germany | 2011 | 272 | 30.22 |

| 6 | O'Dwyer, Owen | Assurance statement practice in environmental, social and sustainability reporting: A critical evaluation | 2005 | 271 | 18.07 |

| 7 | Brown, de Jong, & Levy | Building institutions based on information disclosure: lessons from GRI's sustainability reporting | 2009 | 255 | 23.18 |

| 8 | Lozano & Huisingh | Inter-linking issues and dimensions in sustainability reporting | 2011 | 252 | 28 |

| 9 | Singh, Murty, Gupta, Dikshit | Development of composite sustainability performance index for steel industry | 2007 | 248 | 19.08 |

| 10 | Roca Laurence Clément, & Cory Searcy | An analysis of indicators disclosed in corporate sustainability reports | 2012 | 242 | 30.25 |

| 11 | Moneva, Archel, & Correa | GRI and the camouflaging of corporate unsustainability | 2006 | 240 | 17.14 |

| 12 | Chen, Bouvain | Is corporate responsibility converging? a comparison of corporate responsibility reporting in the USA, UK, Australia, and Germany | 2009 | 233 | 21.18 |

| 13 | Etzion, Ferraro | The role of analogy in the institutionalization of sustainability reporting | 2010 | 214 | 21.4 |

| 14 | Clarkson, Overell, & Chapple | Environmental Reporting and its Relation to Corporate Environmental Performance | 2011 | 207 | 23 |

| 15 | Boiral | Sustainability reports as simulacra? A counter-account of A and A+ GRI reports | 2013 | 186 | 26.57 |

| 16 | Michelon, Pilonato, & Ricceri | CSR reporting practices and the quality of disclosure: An empirical analysis | 2015 | 182 | 36.4 |

| 17 | Lim, Tsutsui | Globalization and commitment in corporate social responsibility: Cross-national analyses of institutional and political-economy effects | 2012 | 175 | 21.88 |

| 18 | Lozano | A tool for a Graphical Assessment of Sustainability in Universities (GASU) | 2006 | 174 | 12.43 |

| 19 | Lamberton | Sustainability accounting - A brief history and conceptual framework | 2005 | 161 | 10.73 |

| 20 | Reynolds, Yuthas | Moral discourse and corporate social responsibility reporting | 2008 | 158 | 13.17 |

Table 8. The top 20 highly cited countries & journals

| No. | Countries | TC | TP | Journals | TC | TP |

|---|---|---|---|---|---|---|

| 1 | United Kingdom | 3579 | 68 | Journal of Cleaner Production | 3032 | 51 |

| 2 | United States | 3500 | 132 | Journal of Business Ethics | 2188 | 27 |

| 3 | Australia | 3085 | 74 | Corporate Social Responsibility and Environmental Management | 1529 | 44 |

| 4 | Canada | 2799 | 45 | Accounting Forum | 710 | 8 |

| 5 | Spain | 2746 | 119 | Ecological Indicators | 424 | 7 |

| 6 | Italy | 1961 | 71 | Sustainability Switzerland | 388 | 34 |

| 7 | Netherlands | 1804 | 30 | Sustainability Accounting Management and Policy Journal | 379 | 19 |

| 8 | Germany | 1341 | 49 | Accounting Auditing and Accountability Journal | 294 | 9 |

| 9 | New Zealand | 585 | 16 | Business Strategy and The Environment | 185 | 8 |

| 10 | France | 540 | 26 | International Journal of Sustainability In Higher Education | 169 | 5 |

| 11 | Sweden | 508 | 12 | Corporate Communications | 167 | 8 |

| 12 | India | 477 | 41 | Social Responsibility Journal | 138 | 21 |

| 13 | Belgium | 434 | 8 | Acta Universitatis Agriculturae Et Silviculturae Mendelianae Brunensis | 97 | 11 |

| 14 | Portugal | 427 | 22 | Corporate Environmental Strategy | 88 | 5 |

| 15 | Brazil | 417 | 59 | Environmental Quality Management | 64 | 6 |

| 16 | Austria | 387 | 18 | Meditari Accountancy Research | 55 | 5 |

| 17 | South Africa | 306 | 19 | Social and Environmental Accountability Journal | 46 | 5 |

| 18 | Finland | 301 | 15 | Gestao E Producao | 17 | 7 |

| 19 | Greece | 293 | 22 | Corporate Ownership and Control | 10 | 5 |

| 20 | Malaysia | 265 | 29 | Revista De Gestao Social E Ambiental | 4 | 5 |

Notes: TP=total number of publications; TC=total citations

4.3. Subject area analysis

To accomplish RO3 (to investigate the most popular influential subject areas in GRI with sustainability reporting research among researchers), we classified documents in our dataset into different subject areas as presented in Table 9. The distribution of research on GRI with sustainability reports emerges mainly from Business, Management and Accounting (545, 57%), Social Sciences (348, 36%) Environmental Science (305, 32%), and Economics, Econometrics, and Finance (194, 20%). The least distributions are related to subjects Nursing, and Pharmacology, Toxicology, and Pharmaceutics (1, 0.1%)

Table 9. Subject area classification

| Subject Area | (TP) | (%) |

|---|---|---|

| Business, Management and Accounting | 545 | 57.06 |

| Social Sciences | 348 | 36.43 |

| Environmental Science | 305 | 31.94 |

| Economics, Econometrics and Finance | 194 | 20.31 |

| Engineering | 151 | 15.81 |

| Energy | 149 | 15.60 |

| Decision Sciences | 61 | 6.39 |

| Computer Science | 55 | 5.76 |

| Arts and Humanities | 40 | 4.19 |

| Agricultural and Biological Sciences | 35 | 3.67 |

| Earth and Planetary Sciences | 28 | 2.93 |

| Medicine | 19 | 1.99 |

| Chemical Engineering | 11 | 1.52 |

| Materials Science | 9 | 0.94 |

| Mathematics | 9 | 0.94 |

| Physics and Astronomy | 7 | 0.73 |

| Chemistry | 4 | 0.42 |

| Health Professions | 4 | 0.42 |

| Multidisciplinary | 4 | 0.42 |

| Biochemistry, Genetics and Molecular Biology | 3 | 0.32 |

| Psychology | 3 | 0.32 |

| Neuroscience | 3 | 0.32 |

| Nursing | 1 | 0.11 |

| Pharmacology, Toxicology and Pharmaceutics | 1 | 0.11 |

Notes: TP=total number of publications

4.4. Keywords analysis

Bibliometric analysis is used extensively to develop the knowledge structure of a particular domain (Aria & Cuccurullo, 2017). To achieve RO4 (to evaluate the influential keywords in GRI with sustainability reporting research), we used keyword analysis and co-occurrence since authors' keywords show documents' contents (Comerio & Strozzi, 2019). Keywords of a document are assumed to give an appropriate description of a documents' content and their co-occurrence reveals the pattern and evolution of knowledge within a domain (Aparicio et al., 2019). Besides, keyword co-occurrence is a concept that refers to similar keywords presence across an article (Li et al., 2016). Keyword co-occurrence networks are usually using a graphical visualization of potential relationships between keywords in the documents. Therefore, this type of analysis is used by scholars to measure the performance of commination channels, and information circulations (Su & Lee, 2010). Table 10 presents TP and the percentage of the top 20 authors' keywords utilized between 1999 and 2020 in the Scopus database. Global Reporting Initiative is the most frequently used author keyword in GRI with sustainability reporting research topics with (30%) with a TP of 289. The second-highest percentage (26%) is allocated to Sustainable Development with TP of 250 followed by Sustainability (25%, 240), Corporate Social Responsibility (22%, 209), Sustainability Reporting (21%, 204), and GRI (15%, 142). Among the top 20 most active authors keywords, corporate governance, social aspects, and social responsibility have emerged in the literate of this field with a low percentage of 3, and TP of 30.

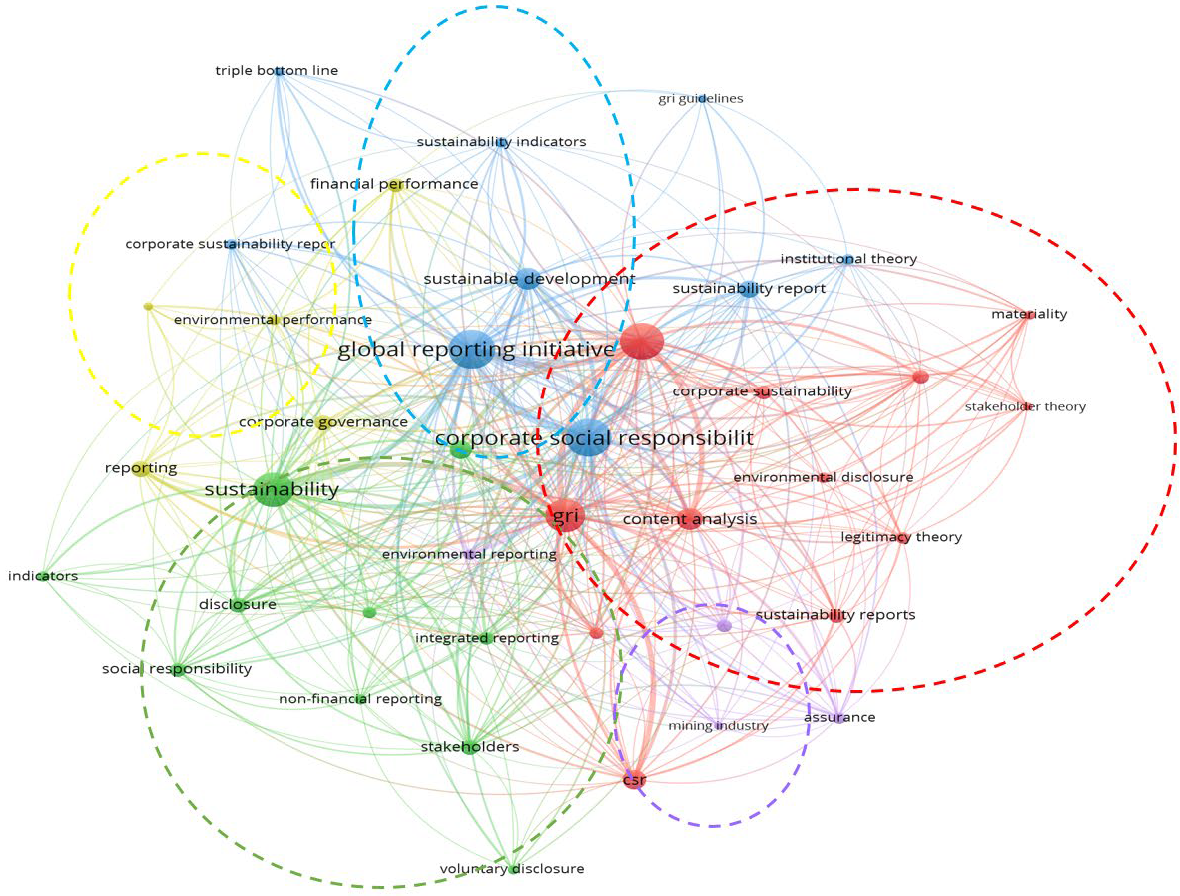

To find the co-occurrence of the authors' keywords, we utilized the VOSviewer to depict the network visualization map of the author keywords. We evaluated our co-occurrence analysis with a minimum number of occurrences of 10 keywords from 1999 which met 40 terms. As shown in Figure 3, the size of a node refers to the frequency of occurrence. Global reporting initiatives, sustainability reporting, content analysis, corporate social responsibility, and GRI are the most distinctive nodes in the network graph which depict their prominent role in this field of research. According to the network visualization map, there are five distinctive clusters depicts in different colours which are named and listed as below:

Stakeholders (red colour) representative of a keyword like accountability, GRI, stakeholder's engagement, stakeholder theory, legitimacy theory, etc.

Non-financial and integrated reporting (green colour) contains keywords such as disclosure, global reporting initiative, non-financial reporting, integrated reporting, voluntary disclosure, etc.

Corporate social responsibility (blue colour) covers corporate sustainability, corporate social responsibility, sustainability reports, sustainability development, GRI guideline, triple bottom line, etc.

Performance (yellow colour) refers to environmental performance, financial performance, corporate governance, key performance indicator, etc.

CSR reporting (purple colour) covers assurance, CSR reporting, environmental reporting, and the mining industry.

Figure 3. Network visualization map of the co-occurrence of keywords

Table 10. The top 20 active authors’ keywords

| Author Keywords | TP | Percentage (%) |

|---|---|---|

| Global Reporting Initiative | 289 | 30.26 |

| Sustainable Development | 250 | 26.18 |

| Sustainability | 240 | 25.13 |

| Corporate Social Responsibility | 209 | 21.88 |

| Sustainability Reporting | 204 | 21.36 |

| GRI | 142 | 14.87 |

| Sustainability Report | 78 | 8.17 |

| Content Analysis | 67 | 7.02 |

| CSR | 49 | 5.13 |

| Global Reporting Initiative (GRI) | 49 | 5.13 |

| Stakeholder | 43 | 4.50 |

| Environmental Impact | 37 | 3.87 |

| Corporate Social Responsibilities (CSR) | 36 | 3.77 |

| Environmental Management | 36 | 3.77 |

| Disclosure | 35 | 3.66 |

| Reporting | 34 | 3.56 |

| Stakeholders | 31 | 3.25 |

| Corporate Governance | 30 | 3.14 |

| Social Aspects | 30 | 3.14 |

| Social Responsibility | 30 | 3.14 |

Notes: TP=total number of publications

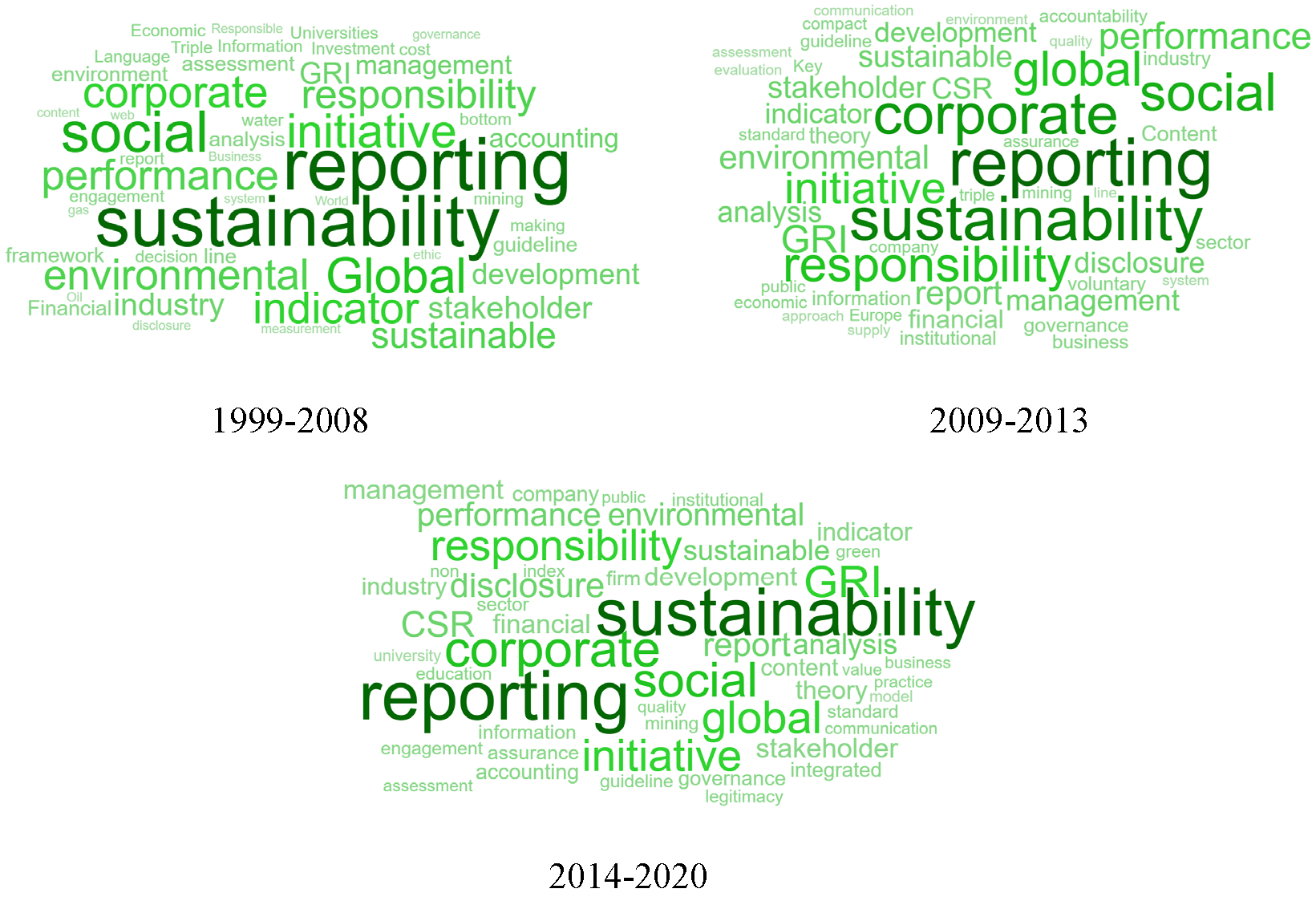

Besides, we further analysed the keyword evolution during the three phases we have discussed previously in Figure 1. Figure 4 indicates that during the first phase (1999-2008) 50 documents used environmental in their abstracts followed by sustainability (33 documents), and reporting (35). The lowest number of documents in this phase is related to GRI (7), global (17), initiative (16). Interestingly in the second phase (2009-2013), the number of documents used GRI enhanced by (64), sustainability (118), reporting (138), corporate (104), global (71), performance (41), responsibility (76), initiative (61), and social (88). Additionally, in phase three (2014-2020), the usage of keywords has increased dramatically as follows: GRI (199), sustainability (476), reporting (506), initiative (194), global (205), social performance (100), and corporate (269). It can be understood from the keyword evolution, topics related to GRI guidelines, sustainability reporting has been received much attention from scholars in the last 10 years which depicts the importance of this area in the literature.

Figure 4. The progress of the "word cloud" of GRI with sustainability reports

4.5. Authorship and Co-Authorship Analysis

To address RO5 (to evaluate the most effective authors in GRI with sustainability reporting research), we used the number of authors per document and co-authorship analysis to analyze the current state of authors' collaborations. Collaboration analysis is a tool to understand the social structure of a research domain (Aria & Cuccurullo, 2017). Table 11 shows a TP of 169 (18%) documents that have single authors in this area during 1999-2020. The highest number of TP (312) (33%) are related to two-authored documents. There are 3 documents whose author's names are not listed based on the Scopus database.

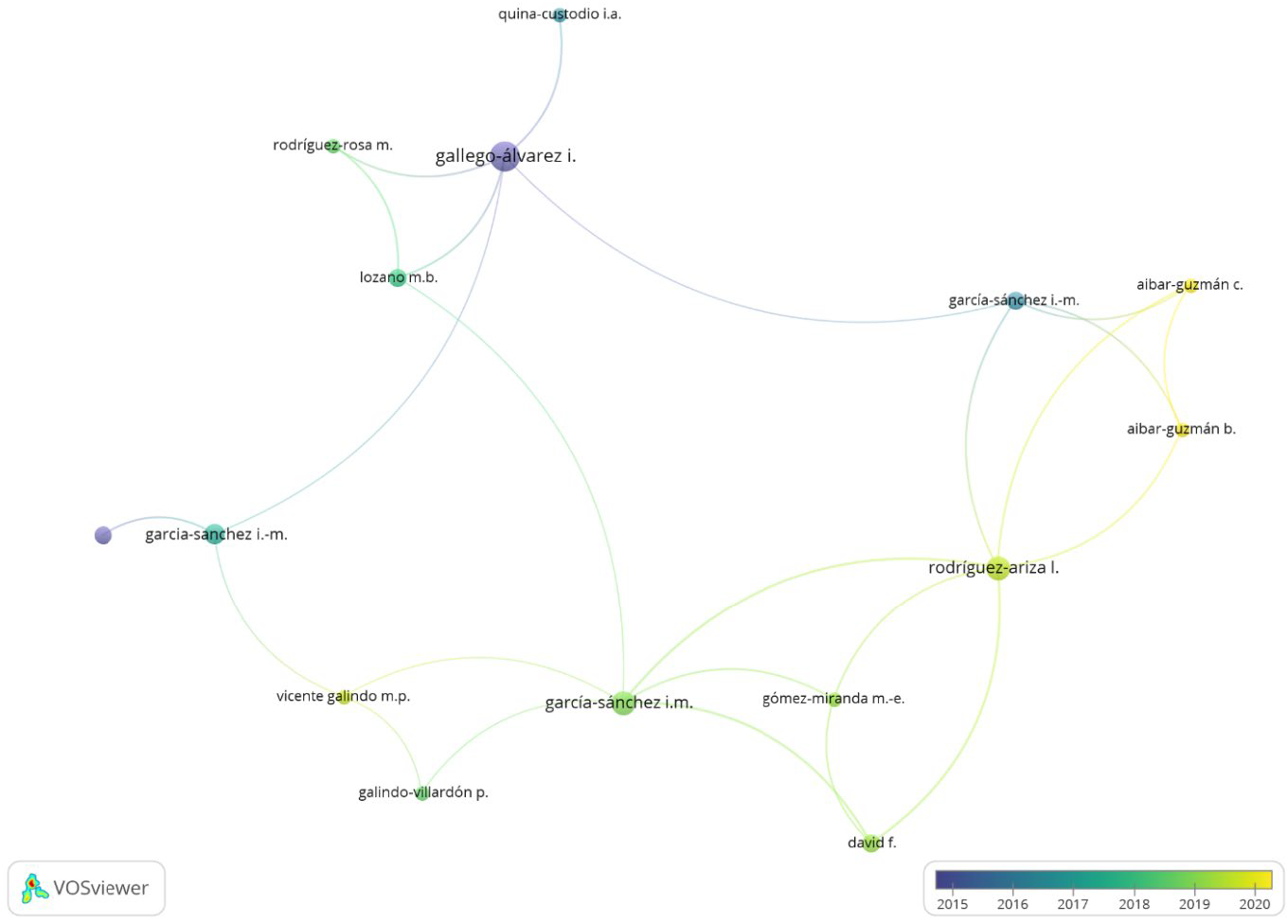

Furthermore, we interpreted co-authorship analysis using VOSviewer visualization network to uncover the author's cooperation link with this field of research. This is important due to the reason that TP and TC authors help experts in a related field of research to enhance the reliability/visibility of their research output. Indeed, having international collaboration networks helps emerging countries to enhance their maturity of ideas and quality of their works by getting some guidance from published documents in the developed countries (Palacios-Callender and Roberts, 2018). Besides, mostly multi-authored published articles have fewer mistakes in their output (Tahamtan et al., 2016). The social structure/network depicts that there are various collaboration networks among scholars in this field. Figure 5 represents the overlay visualization map of the co-authorship of authors publishing a minimum of 2 documents, minimum of 1 citation, and a total of 289 authors records. The authors are grouped into 4 clusters with 15 items concerning their co-authorship relationship. The size of the node depicts the frequency of published documents. Nodes' colours, in this case, signify research activities in terms of average publication year. Overlay of co-authorship of authors is from 2015 to 2020, and among these authors, García-Sánchez, I.M. (Universidad de Salamanca, Spain) has the highest number of publications of 13, followed by Gallego-Álvarez, I. (Universidad de Salamanca, Spain) with 8 publications, and Rodríguez-Ariza, L. (Universidad de Salamanca, Spain) with 5 publications. As can be seen, Spanish authors have the highest number of co-authorship relationships. This might be due to the importance of the implementation status of SDGs in Spain and exploring the extent to which the country can be able to meet European standards in sustainability by the year 2030 (United Nations, 2020a; 2020b; García-Sánchez et al., 2020). Therefore, the Spanish government created the position of High Commissioner intending to generate social and environmental value, and in the fight against inequalities (Boto-Álvarez & García-Fernández, 2020).

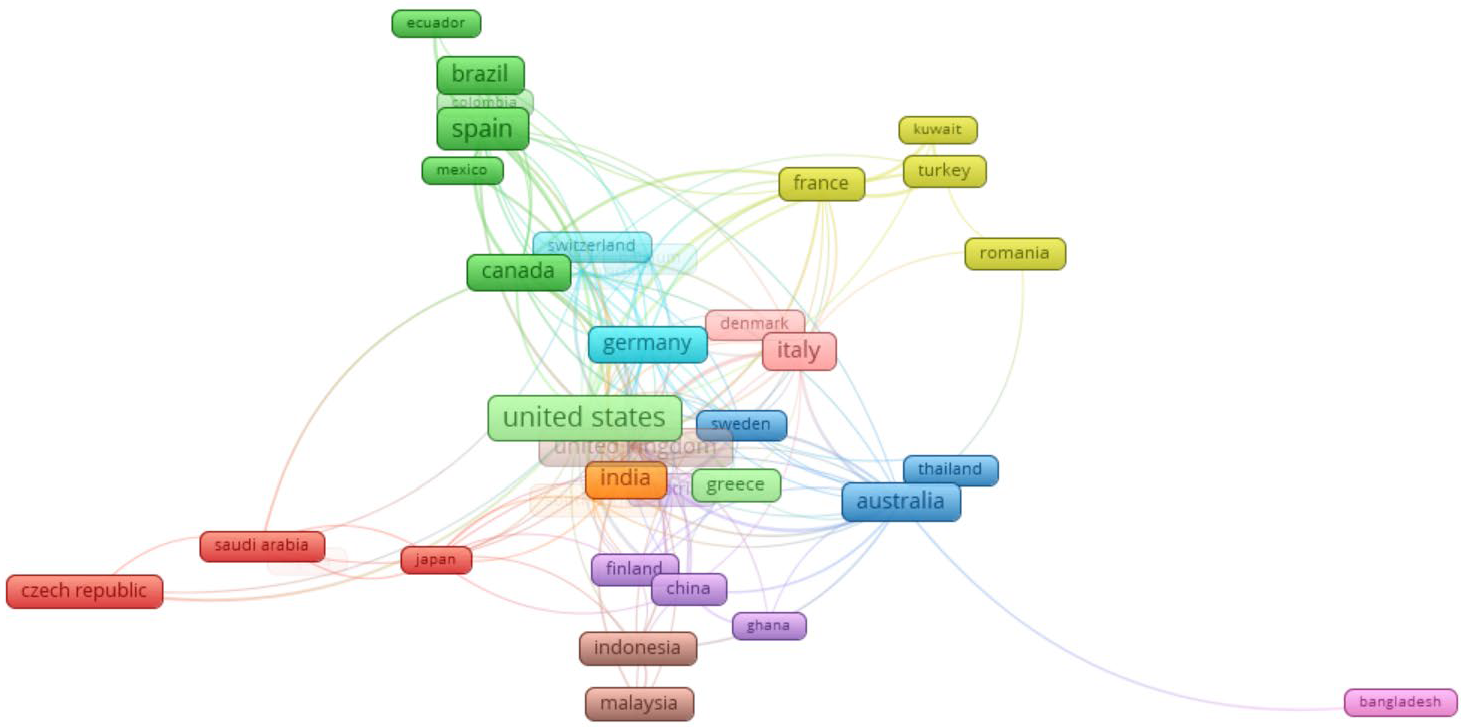

Additionally, we interpreted the co-authorship for 86 countries in Figure 6. The countries are grouped into 11 clusters with 45 items (countries). Each cluster is grouped based on similarities in published documents. Among the countries, the United States has the highest number of documents (131) followed by Spain with 119 documents, Australia with 73 documents, Italy with 71 documents, the United Kingdom with 68 documents, and Brazil with 59 documents. It is worth mentioning that size of the nodes in the map represents the quantity of research activity in each country for GRI with sustainability reports research.

Table 11. Number of the author(s) per document

| Author Count | (TP) | Percentage (%) |

|---|---|---|

| 0 | 3 | 0% |

| 1 | 169 | 18% |

| 2 | 312 | 33% |

| 3 | 281 | 29% |

| 4 | 133 | 14% |

| 5 | 35 | 4% |

| 6 | 9 | 1% |

| 7 | 9 | 1% |

| 8 | 2 | 0% |

| 17 | 2 | 0% |

| Total | 955 | 100.00 |

Notes: TP=total number of publications

Figure 5. Overlay visualization map of the co-authorship of authors

Figure 6. Network visualization map of the co-authorship of counties

4.6. Co-Citation Analysis

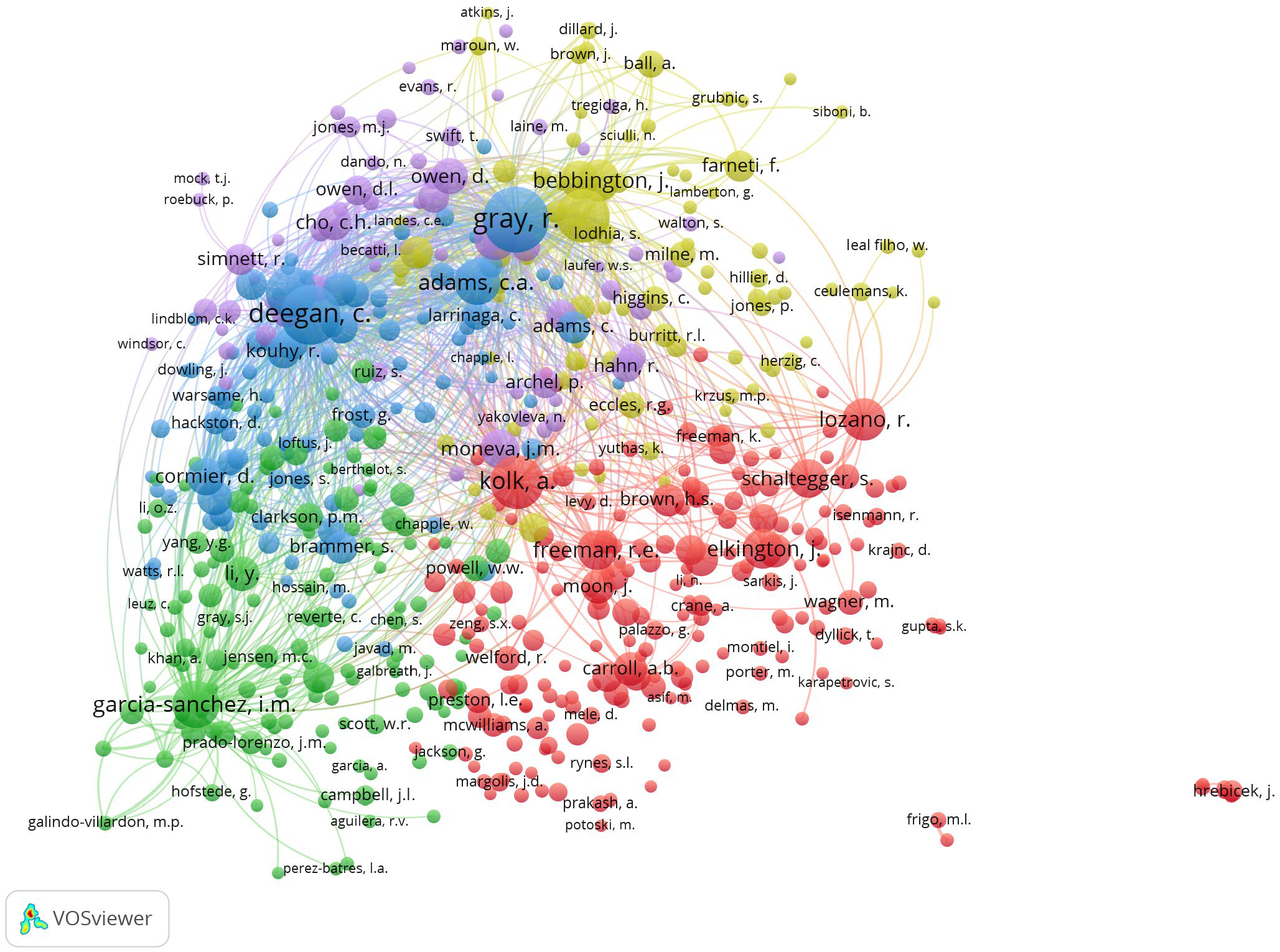

Co-citation analysis shows collaboration among scholars for the amount of papers co-cited (Small, 1973; García-Lillo et al., 2019). Co-citation is related to the intellectual structure of the bibliometric review (Rossetto et al., 2018). Co-citation usually considers references of primary documents, and thus it is implemented for cited documents and journals (Martínez-López et al., 2018). Co-citation network analysis is thus usually considered as a means to understand the historical evolution of a particular knowledge base. Therefore, we used co-citation analysis by authors to achieve our RO6 (to provide the intellectual structure in GRI with sustainability reporting research). Figure 7 depicts the network visualization map of the co-citation of authors. Our initial interpretation shows that 579 of 32687 authors with a minimum of 20 citations in GRI and sustainability reporting research topics are co-cited in the publication within the network between 1999 to mid-2020. As can be seen in the figure, authors are categorized into 5 clusters based on the relevancy of their publications. Gray, R. (University of St Andrews, United Kingdom), Kolk, A. (the University of Amsterdam, the Netherlands), Garcia-Sanchez, I.M. (University of Salamanca, Spain), Guthrie, I. (Macquarie University, Australia), and Owen, D. (Nottingham University, United Kingdom) are the authors with the highest co-citation in clusters blue, red, green, yellow, and purple respectively. Moreover, as the biggest node sizes are in cluster blue, therefore, the authors in this cluster have the highest co-citation.

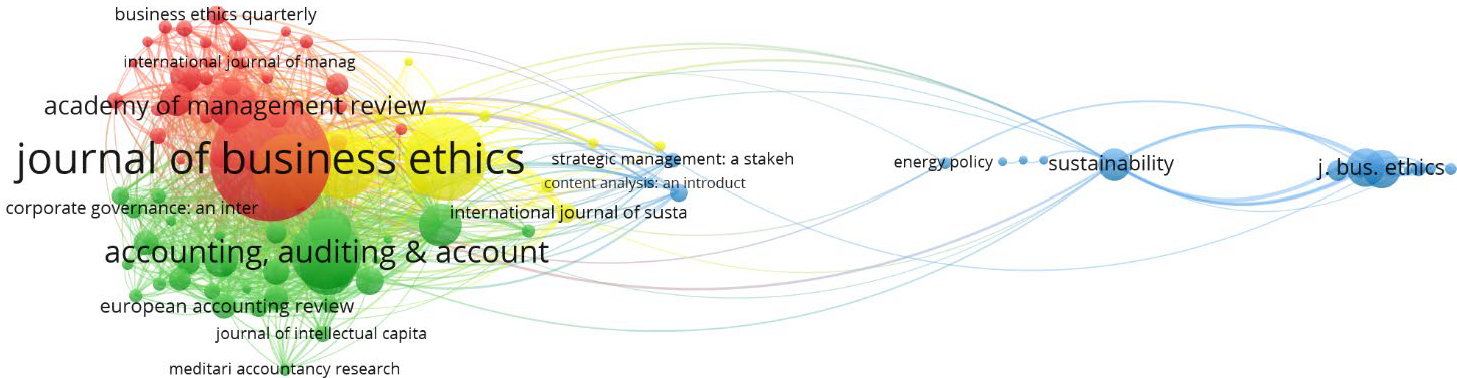

Further, we developed the co-citation of cited references. Out of the 16,800 sources, 233 met the initial criteria of a minimum of 20 citations. Among these 233 sources, we considered the top 100 sources, with a maximum link strength. Figure 8 depicts the co-citation analysis of the top 100 linked sources cited in the field of sustainability reporting with the GRI network in four clusters. This network has 3,810 links with a total link strength of 304290. Cluster one (red) is the largest and it has 34 sources. Few of these include studies from the Journal of Business Ethics, Academy of Management Journal, Strategic Management Journal, Business, and Society, Business Ethics: A European Review, Business and Society Review, California Management Review, Business Ethics Quarterly, and so on. We named this cluster as Business Ethics cluster. The second-largest cluster (Green colour) in the network has very near sources to cluster one (32) that includes for example Accounting, Auditing and Accountability Journal, Accounting and Business Research, Accounting, Organization and Society, Australian Accounting Review, British Accounting Review. We named this cluster accounting review cluster. The third cluster (blue colour) has 19 sources such as Sustainability, Sustainability Accounting, Corporate Social Responsibility, and Environmental Management, Strategic Management: A Stakeholder Approach, Sustainability Accounting, and Accountability, and hence we named this cluster Sustainability. And the last cluster (yellow colour) has 15 sources including the Journal of Cleaner Production, Business Strategy, and the Environment, Ecological Economics, International Journal of Sustainability in Higher Education, Environmental Management, Journal of Environmental Management, and therefore we called this cluster Environment.

Figure 7. Network visualization map of the co-citation of authors

Figure 8. Network visualization map of the co-citation of cited references

4.7. Bibliographic coupling among authors

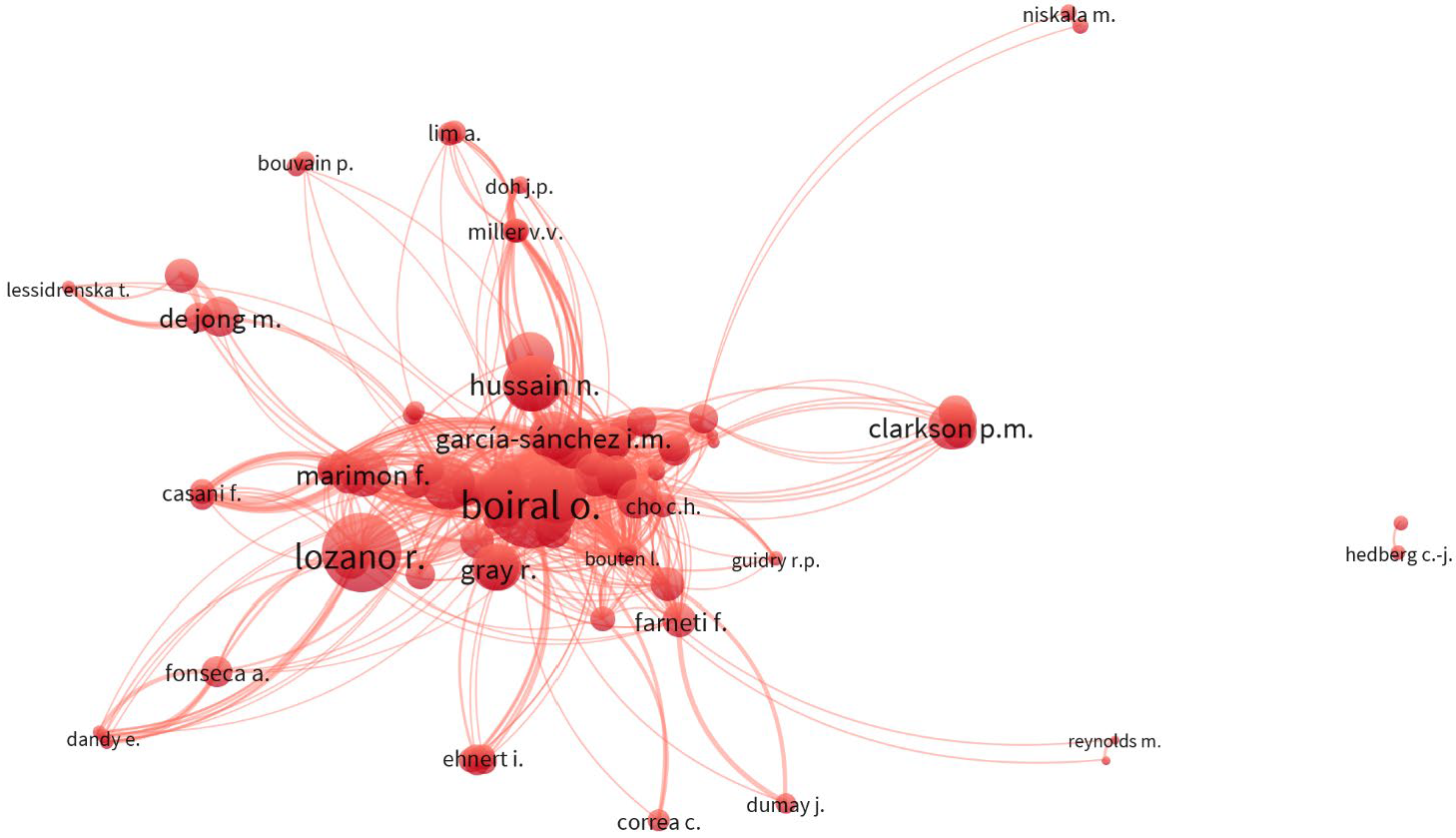

Further, to address RO6 related to the intellectual structure of documents in the domain of GRI and sustainability reporting, we developed a bibliographic coupling network among authors, which is another comprehensive approach in visualizing knowledge networks within a domain (Bamel et al., 2020). This is due to the reason that co-citation utilizes secondary documents to understand the historical focus and evolution of a field, however; bibliographic coupling considers primary documents to find the emerging topics and future directions of a field (Vogel, 2012). Figure 9 shows the authors' bibliographic network which out of 1,996 authors, 1000 met with a minimum number of 1 document and 0 citations for an author. We considered the top 100 authors. This yielded a network with one having 4,000 links and 44,246 total link strength. This cluster is mainly based on García-Sánchez, I.M, apart from a few other influential authors in this cluster, namely Boiral, O., Lozano, Gallego-Álvarez, I.M, Manetti, G. and so on. The main focus of this cluster is sustainability reporting based on GRI guidelines (Prado-Lorenzo et al., 2009; Boiral, 2013; Fuente et al., 2017).

Figure 9. Bibliographic coupling network of authors

5. Discussion and implications

The current research contributes to the literature by providing a reflection on the extent and impact of the GRI in sustainability reporting from 1999 to 2020, and utilizing a quantitative and bibliometric literature review based on the Scopus database. Considering the great advancement of using sustainability reports as an attitude for supporting and creating value for organizations, GRI guidelines and frameworks are regarded as a prominent contributor to sustainability development (E-Vahdati et al., 2018). Our bibliometric analysis suggests an opportunity to review past studies and helps in the future progression of a knowledge field, such as GRI, SDG, integrated reporting. To the best of our knowledge, this is the first study to use numerous bibliometric analysis types to review published documents in GRI with sustainability reports research. Further, we interpreted our review based on the Scopus database which is among the most extensive and high-quality bibliometric data sources for academic research online databases that index all scholarly work (Baas et al., 2020).

Respectively for this purpose, we replied to six research questions: first, we contributed to the literature by focusing on the trend of publication of topics related to GRI with sustainability reports (RO1). We found that although the number of published documents has been increased during the period, the highest number of publications in phase three (2013 to 2019) enhanced dramatically which shows the number of interests in scholars to study in this area. Further, the United States is the most predominant country by the number of documents followed by Spain, Australia, Italy, and the United Kingdom. Another feature about geographical distribution is that only a few studies have been affiliated from developing countries such as India, Indonesia, and Malaysia. Besides, the most active source titles in this field are Journal of Cleaner Production, followed by Corporate Social Responsibility and Environmental Management, Sustainability, Journal of Business Ethics, and Social Responsibility Journal. Our further analysis showed that the most productive authors are García-Sánchez, I.M. (Universidad de Salamanca, Spain), followed by Boiral, O. (Université Laval, Canada), Lozano, R. (Hogskolan I Gavle, Sweden), Manetti, G. (Università degli Studi di Firenze, Italy), and Nikolaou, I.E. (Democritus University of Thrace, Greece). Moreover, the top five influential institutions based on the higher number of total publications are Universidad de Salamanca, Spain; Universidade de Sao Paulo -- USP, Brazil; Università degli Studi di Firenze, Italy; University of Valencia, Spain; and Universidade Federal de Santa Catarina, Brazil respectively.

Second, we interpreted the results of published documents based on citation analysis as cited authors, countries, and journals can contribute to the knowledge of research in the field of GRI and sustainability reports (RO2). Our findings found that the majority of documents in this field of study, that is 78%, have received at least one citation. The top rank in terms of the prominent authors with a greater number of TCs is Clarkson et al. (2008) followed by Azapagic (2004), Milne & Gray (2013), and Krajnc & GlaviÄ (2005) whose work proposed a model and framework for sustainable development. Further, the most prominent journals with the highest citations in GRI and sustainability reporting are Journal of Cleaner Production, Journal of Business Ethics, and Corporate Social Responsibility and Environmental Management, and Accounting Forum. In terms of geographical locations, United Kingdom dominates the list, followed by the USA and Australia.

Third, we interpreted publications based on subject area classification (RO3), and we suggested that the majority of publications are classified in Business, Management, and Accounting, followed by Social Sciences, Environmental Science, Economics, Econometrics, and Finance subject areas.

Fourth, we contributed through the understanding of the conceptual structure of the GRI and sustainability reporting research base by focusing on keyword and co-word (co-occurrence) analyses in GRI with sustainability reports literature (RO4). Our findings recommended that the most frequent author keywords in this field of research are the Global Reporting Initiative followed by Sustainable Development, Sustainability, and Corporate Social Responsibility. Furthermore, the co-occurrence of words is evaluated through five clusters. In clusters red, blue, green, yellow, and purple the highest number of occurrences are connected with sustainability reporting, global reporting initiative, sustainability, reporting, and CSR reporting in order. These results sound logical as the necessity of using and implementing international guidelines (GRI) in sustainability reports has been increased interestingly.

Fifth, we contributed through conserving the important role of influential authors, in researching this field by evaluating findings based on top effective authors and the current state of collaboration (co-authorship analysis) (RO5). Our evidence shows that some two-authored have the highest number of publications along with three-authored documents. Therefore, we conclude that although the level of collaboration among two or three-authored documents is satisfactory, better collaborative efforts among academicians are required. Meanwhile, collaboration among scholars mostly happened during 2015-2020, and the highest rank of co-authorship is connected with authors namely García-Sánchez, I.M. (Universidad de Salamanca, Spain), and Gallego-Álvarez, I. (Universidad de Salamanca, Spain); and countries of the United States and Spain.

Finally, we contributed to the intellectual structure of studies in this field by performing co-citation and bibliographic coupling analyses (RO6) to guide scholars to avoid latency and move this area of research forward. Based on our findings, we concluded that the red cluster has the highest number of co-citations contains mostly articles on sustainability reporting from an accounting perspective. Further, we developed the co-citation analysis of co-cited references. Our findings offer that Cluster one (red) is the largest cluster and mostly includes studies from the Journal of Business Ethics, Academy of Management Journal, Strategic Management Journal, Business, and Society. Moreover, our results in performing a coupling bibliographic networks using authors show that there is one cluster which is highly based on García-Sánchez, I.M, followed by Boiral, Lozano, Gallego-Álvarez, and Manetti.

In brief, the result shows the importance of GRI-sustainability reports over the past 20 years where the publication trend in this area consistently increased. Our analyses offer the main research streams, their trend, and their focus which provides an understanding of the newer research patterns and leading trends in this field. Future scholars may use this study to position their future research interests and finding the research gap and current development of this issue. Further, practitioners or management may refer to this study in strategizing the companies' sustainability report by reference to GRI guidelines and identify the most relevant and current trend of reporting. The findings of this research contributed not only to the existing body of knowledge on GRI's sustainability report but also may provide future directions towards methodological and empirical evidence for future reference.

Therefore, this study enhanced the importance of the topic by combining the bibliometric techniques of co-occurrence, co-authorship analysis, co-citation, and bibliographic coupling, where the results show complementary structures and evolution of the field. These analyses offer a deeper understanding of how the field of the study is structured and evolves, and what the possible future development would be.

6. Conclusion and limitation

In conclusion, this study provides a holistic view of the GRI's sustainability reporting knowledge base by conducting a review of all published documents through bibliometric analysis. Through this contribution, researchers can access easily information on various trends and research streams of GRI-related topics with sustainability reporting/disclosure which is still an emerging topic among scholars. Further, the growth trajectory of bibliometric analysis in the interpretation of research can be implemented within many scientific communities, by funding agencies, politicians, and professional sustainability/agency communities. However, this study is also not free from certain limitations. We focused solely on bibliometric analysis with the ability to map the structure and development of this topic. The usefulness and preciseness of this study can be enhanced if a systematic review that focuses on qualitative literature analysis is integrated with bibliometric analysis. The mixed qualitative and quantitative approach in designing the future study on the development of literature review has become more popular recently. Therefore, we believe that this contribution aids scholars focus on impactful future research.