Exploring sustainability reporting assurance: Uncovering research patterns and emerging trends with a bibliometric analysis

ABSTRACT

In this paper, we conducted an extensive bibliometric analysis of the current state-of-the-art in sustainability reporting assurance (SRA). Our goal was to identify research patterns, critical areas, and emerging trends that can guide future research and development in this field. We used two advanced bibliometric software, VosViewer and Biblioshiny on R Studio, to conduct a complex bibliometric analysis. We visually analysed 633 studies from the Web of Science database from 1992 to 2023. Our study examined the trend of publications, the most influential journals, publications, authors, institutions, and interconnections among countries, keywords, and journals. Next, we conducted a bibliometric analysis of keywords and a thematic map analysis to identify emerging research themes. We then identified and ranked the 50 most influential studies in the field of SRA based on their average citations per year. Through content analysis, we highlighted the foundational theories, research methods used, and main thematic issues addressed in these studies. Finally, we suggested relevant avenues for future research in the SRA domain for each primary thematic analysis. Overall, this analysis provides valuable insights into current research trends and can help guide future research efforts in sustainability reporting assurance.

Keywords: Sustainability reporting assurance; Bibliometric analysis; Corporate governance mechanisms; Choice of assurance providers; Independence of assurance providers.

JEL classification: Q56; M40.

Explorando la verificación de los informes de sostenibilidad: Identificando patrones de investigación y tendencias emergentes mediante un análisis bibliométrico

RESUMEN

En este artículo, llevamos a cabo un extenso análisis bibliométrico sobre el estado actual del arte en la verificación de los informes de sostenibilidad (SRA, por sus siglas en inglés). Nuestro objetivo fue identificar patrones de investigación, áreas clave y tendencias emergentes que puedan orientar futuras investigaciones y desarrollos en este campo. Utilizamos dos programas avanzados de análisis bibliométrico, VosViewer y Biblioshiny en R Studio, para realizar un análisis bibliométrico complejo. Analizamos visualmente 633 estudios extraídos de la base de datos Web of Science, desde 1992 hasta 2023. Nuestro estudio examinó la evolución de las publicaciones, las revistas, autores, instituciones y publicaciones más influyentes, así como las interconexiones entre países, palabras clave y revistas. A continuación, realizamos un análisis bibliométrico de palabras clave y un análisis de mapas temáticos para identificar temas de investigación emergentes. Posteriormente, identificamos y clasificamos los 50 estudios más influyentes en el ámbito de la SRA según su promedio de citas por año. Mediante un análisis de contenido, destacamos las teorías fundamentales, los métodos de investigación utilizados y los principales temas tratados en dichos estudios. Finalmente, propusimos líneas relevantes para futuras investigaciones en el ámbito de la verificación de los informes de sostenibilidad, basándonos en cada uno de los principales análisis temáticos. En conjunto, este análisis ofrece una visión valiosa de las tendencias actuales de investigación y puede contribuir a orientar los esfuerzos futuros en este campo.

Palabras clave: Verificación de los informes de sostenibilidad; Análisis bibliométrico; Mecanismos de gobernanza corporativa; Elección de proveedores de verificación; Independencia de los proveedores de verificación.

Códigos JEL: Q56; M40.

1. Introduction

Corporate social responsibility (CSR) reporting, or sustainability reporting is a crucial tool for companies to gain legitimacy and transparency regarding environmental, social, and governance issues. Companies and stakeholders have opted for independent audits or assurance of their CSR reports to increase their credibility. This practice was initiated to meet the growing need for information and transparency and enhance their credibility and legitimacy (Simnett et al., 2009; Cohen and Simnet, 2015; García-Sánchez, 2020). Many experts argue that sustainability reporting gains more credibility when it undergoes external assurance (Zorio et al., 2013; Sierra et al., 2013; Odriozola and Baraibar-Diez, 2017). Furthermore, Martínez-Ferrero and García-Sánchez (2017a, b) have noted that stakeholders increasingly demand more credible and legitimate sustainability reporting. They suggest that external assurance can enhance stakeholders' trust in the quality of sustainability information and a company's dedication to sustainability (Lejárraga García et al., 2024; Martínez-Ferrero and García-Sánchez, 2017a, b; Simnett et al., 2009). Although there is a consensus that sustainability reporting assurance can improve the accuracy of reports, some remain doubtful about its true purpose - whether it is a mere symbolic gesture or a sincere effort to shape stakeholders' perceptions (Michelon et al., 2015). In addition, certain limitations may hinder the assurance process's effectiveness. These include auditor independence, the absence of clear criteria for avoiding conflicts of interest, insufficient expertise and training, and a lack of transparency regarding materiality and sustainability criteria that assurance providers should prioritise. (Boiral, 2013; Jones et al., 2014; Diouf and Boiral, 2017; Talbot and Boiral, 2018; Boiral et al., 2019; Boiral and Heras-Saizarbitoria, 2020; Li et al., 2023).

Many studies highlight that sustainability reporting quality will be significantly higher when assurance is provided by audit/accounting professionals (e.g., Manetti and Becatti, 2009; Al-Shaer and Zaman, 2016). Despite the rising global demand for sustainability reporting, assurance rates for sustainability information remain low, as noted by other researchers (Zaman et al., 2021). While external assurance of sustainability reporting has been criticised for its usefulness and consistency (García-Sánchez et al., 2022), recent studies (Kazim et al., 2025) suggest a growing need to enhance assurance practices and establish them as independent mechanisms to ensure transparency and credibility in CSR reporting. However, sustainability reporting assurance (SRA) lacks mandatory standards across all jurisdictions, leading to significant variability in assurance reports from different regions (García-Sánchez, 2020). For instance, before 2021, the Non-Financial Reporting Directive (NFRD) of the European Union enabled member states to demand independent assurance for non-financial data (Ştefănescu, 2025). While France, Italy, and Spain mandated that independent assurance providers verify such information, it was not explicitly stated that these providers must be professional accountants. However, starting on April 2021, the EU Commission adopted the Corporate Sustainability Reporting Directive (CSRD), which will modify the existing NFRD. To promote transparency and accountability, businesses are now required to disclose the impact of their operations on the environment and society. To ensure the reliability and accuracy of this sustainability information, the proposed directive (CSRD) seeks to establish a consistent standard for limited assurance across the EU to eventually transition to reasonable assurance in the future (Accountancy Europe, 2022). Furthermore, the first 12 European Sustainability Reporting Standards (ESRS) have been adopted and will apply to all obligated companies starting in 2025, following their introduction on July 31, 20231.

According to the International Framework for Assurance Engagements, the International Auditing and Assurance Standards Board (IAASB) outlines the definition of assurance engagements as follows: “Assurance engagement means an engagement in which a practitioner expresses a conclusion designed to enhance the degree of confidence of the intended users other than the responsible party about the outcome of the evaluation or measurement of a subject matter against criteria”2. Adhering to established global norms is crucial when carrying out assurance engagements for historical financial data. Such engagements are classified into reasonable or limited assurance categories based on the international framework (IAASB, 2013). Furthermore, in August 2023, the IAASB proposed a fresh standard for sustainability assurance engagements, signifying meaningful progress in sustainability reporting assurance. This standard is called the International Standard on Sustainability Assurance (ISSA) 5000 - General Requirements for Sustainability Assurance Engagements and is designed to serve as a pivotal and globally applicable framework for all sustainability assurance engagements. Professional accountants and non-accountant assurance practitioners are welcome to provide feedback and insights until December 1, 2023, to refine the final version of this standard. The final version of this new standard released on 12 November 2024. This standard delineates the goals of performing a sustainability assurance engagement, including providing reasonable or limited assurance regarding the integrity of sustainability data, and issuing a written report detailing the reasoning behind the conclusion. (IAASB, 2023)

Given the variety of assurance reports available and the lack of consensus in previous literature regarding the efficacy of sustainability reporting assurance, coupled with ongoing discussions about the final version of the proposed comprehensive standard for sustainability assurance engagements (ISSA 5000), a comprehensive bibliometric analysis is imperative. This analysis will facilitate a better understanding of the current state of the field and will help to identify future research opportunities that can be explored in greater depth to ensure further enhancements in the quality of sustainability information. In the past, several studies have explored the topic of sustainability reporting assurance. Examples of such studies include Maroun (2020), Velte (2021), Hazaea et al. (2022), and Oware and Moulya (2022), each with different scientific objectives. For instance, Maroun (2020) aimed to synthesize the findings on emerging forms of CSR assurance practice. The study provided a comprehensive review of the literature on the characteristics, uses, and limitations of CSR assurance services. Additionally, Maroun (2020) developed a conceptual model that distinguishes between determinants of CSR assurance at the national and firm levels. Hazaea et al. (2022) conducted a systematic review of 94 papers from the Scopus database, covering the period between 1993 and August 2021. Their review aimed to evaluate the intellectual development of the field of SRA and provide recommendations for future studies, demonstrating the role of assurance in enhancing the credibility of sustainability reports and corporate reputation. Velte (2021) used legitimacy theory to conduct a structured literature review on 66 quantitative, peer-reviewed, empirical (archival) studies. Their review focused on key corporate social responsibility assurance (CSRA) proxies, such as CSRA adoption, choice of CSR assuror, and CSRA quality. It analysed the governance-related and financial determinants and consequences of CSRA for firms. Finally, Oware and Moulya (2022) used a bibliometric approach to assess the global trend and highlight intellectual foundations in sustainability assurance studies based on a selected sample of 655 documents from the Scopus database, from 2005 to 2022. To highlight the distinctiveness and motivation of our study in comparison to previous studies, we argue that our bibliometric analysis is unique in several ways. Firstly, our research covers a more extended period, from 1992 to 2023, by using the Web of Science database, differentiating it from studies relying on other databases like Scopus. Secondly, we used two bibliometric software tools - VosViewer and Biblioshiny on R Studio to ensure a comprehensive analysis. This allowed us to study publication and citation dynamics, focus on influential journals, publications, authors, and institutions, and explore interconnections among countries, keywords, and journals. Thirdly, we have combined the bibliometric analysis with a content analysis of the 50 most influential studies in the SRA field, ranked based on average citations per year. Moreover, this content analysis helped us to highlight foundational theories, research methodologies, and main thematic issues. This sets our study apart by not only analysing trends but also highlighting the studies that have had a lasting influence on the field so far. Lastly, we suggest avenues for future research within the SRA domain for each primary thematic analysis.

Our bibliometric analysis endeavours to be at the forefront of research efforts in mapping the SRA field, utilising an extensive and comprehensive approach. This analysis aims to illuminate current research patterns and identify emerging trends. To achieve these goals, the study will address the following research questions:

RQ1: What is the trend of publication in the field related to SRA research?

RQ2: What are this field's most influential publications (journals, papers)?

RQ3: Who are the leading contributors (authors, countries, regions, and institutions) in the domain of SRA?

RQ4: What are the most frequent keywords used in this field of research, and how have the keyword trends evolved during the period analysed?

RQ5: What are the primary research directions for further development in this field?

The remainder of this paper is organised into the following sections. Section 2 describes the research framework, data source, and search protocol. Section 3 presents the main findings of the bibliometric analysis. Moving ahead to Section 4, the paper conducts a thorough content analysis of the most prestigious papers in each thematic area, focusing on pertinent sub-themes and prospects for future research. Finally, Section 5 presents the conclusions and limitations of the study.

2. Materials and Methods

2.1 Research framework of the current study

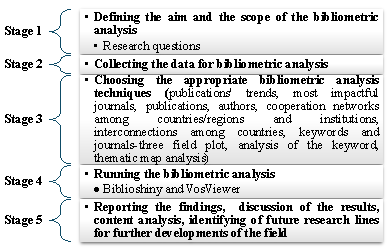

This study aims to provide a comprehensive map of the knowledge structure of the SRA field. To accomplish this, we utilised bibliometric indicators that have recently been developed (Donthu et al., 2021; Wang et al., 2021) to highlight the knowledge structure of the SRA-related research field. We aimed to detect emerging trends in the area and explore future research avenues that require further development. Many visualisation software programs can be used for bibliometric analysis, and different types of network visualisation can be obtained. As other researchers recently stated (Donthu et al., 2021; Xu et al., 2021), each software has advantages and disadvantages; therefore, scholars can opt for the software that best suits their needs. Nevertheless, combining bibliometric software for analysis and visualisation can be the optimal solution to leverage the strengths and overcome the weaknesses of each software (Donthu et al., 2021; Xu et al., 2021). Figure 1 depicts the research framework employed to conduct this bibliometric study.

Figure 1. The research framework of the current study

2.2. Data source and search protocol

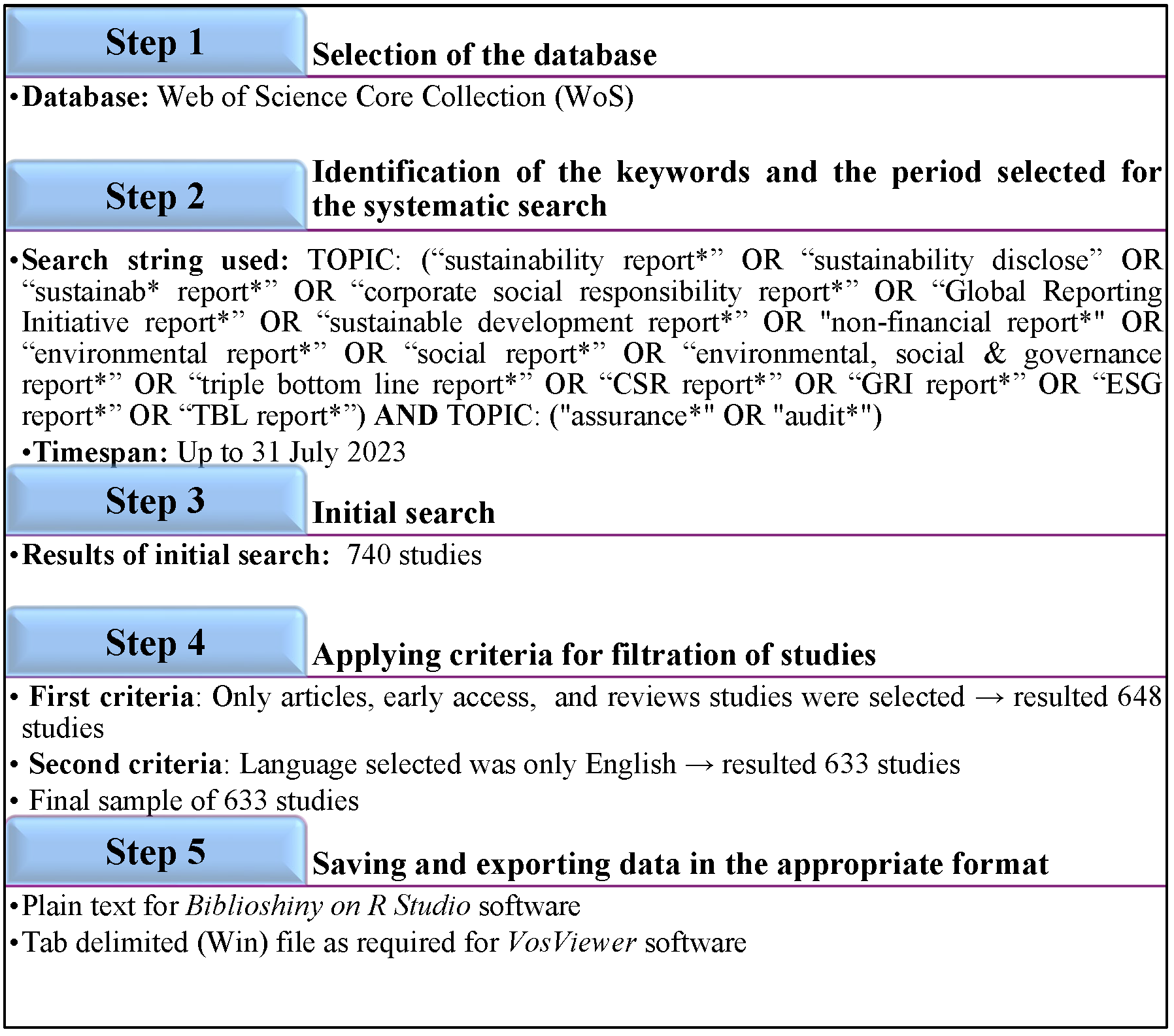

The search for studies to be incorporated into our bibliometric analysis was carried out at the beginning of August 2023, following a search protocol outlined in Figure 2, involving five sequential steps.

Step 1 is the selection of the database. The Web of Science Core Collection (WoS), owned by Thomson & Reuters Co., was considered for the current study. As other researchers noted (Xu et al., 2021; Li et al., 2022; Wang et al., 2021; Raghuram et al., 2019), WoS provides data on top-tier journals and extensive information on publications, making it a primary resource for bibliometric studies (Wang et al., 2021; Zhang and Liang, 2020). While other databases such as Scopus, PubMed, EBSCO, and Google Scholar also provide valuable data for bibliometric and systematic literature review studies, it is essential to recognise that many researchers consider WoS to be a dependable and credible source of information (Agustí and Pérez, 2023; Wang et al., 2021).

During Step 2 of the research process, it is essential to establish suitable keywords and a specific time frame for the systematic search. It's crucial to select appropriate keywords that comprehensively address the topic and are consistent with the research objectives. We devised a search phrase encompassing all conceivable sustainability reporting and assurance terms to accomplish this. As noted by previous researchers (Dienes et al., 2016), sustainability reporting has various terms in both literature and practice. These include "sustainable report*", "corporate social responsibility report*", "Global Reporting Initiative report*", "sustainable development report*", “environmental reporting”, “social reporting”, "environmental, social & governance report*", and "triple bottom line report*", along with their respective abbreviations. It's worth noting that the terms related to integrated reporting were intentionally excluded, as concluded by some previous researchers. Dienes et al. (2016) suggested that integrated reporting has a broader goal than sustainability reporting and supports a holistic approach to management decisions through integrated thinking. Meanwhile, Romero et al. (2019) analysed sustainability information reported by Spanish-listed companies from 2013 to 2015 and found that sustainability reports are higher quality than integrated reports. It is worth noting that while sustainability reports are meant for stakeholders, integrated reports are intended for shareholders. Mio et al. (2020) have effectively outlined the distinctions between sustainability reporting and integrated reporting. As per their analysis, sustainability reporting primarily conveys a company's social and environmental impacts, strategies, and goals to stakeholders. In contrast, integrated reporting is geared towards demonstrating to financial capital providers how value is generated over time. A recent study by Permatasari and Narsa (2022) delved into the debate on sustainability reporting and integrated reporting to determine which is more valuable to investors. The study analysed data from 931 firm years of sustainability reporting issuers and 922 firm years of integrated reporting issuers in Europe and Africa between 2005 and 2019. The findings showed that sustainability reporting has greater value relevance than integrated reporting. However, when integrated reporting was combined with accounting information, it became more valuable due to the reinforcement of accounting information (Permatasari and Narsa, 2022). Therefore, this study focused solely on sustainability reporting, and integrated reporting was not intentionally considered.

We also included the word "audit*" in the second category of assurance-related terms. Although we recognise that assurance and audit are not interchangeable, we felt it necessary to include "audit*" because of the importance of specific relevant papers. These papers indicate that Big-4 auditing firms often dominate the sustainability assurance field, and the selection of an auditor for sustainability assurance can sometimes be influenced by the industry (as shown in Sierra et al., 2013; Handayati et al., 2022; Al-Qudah, A.A., & Houcine, 2023). Furthermore, Sierra-García et al. (2015) suggest that the decision to disclose CSR reports depends on whether a Big-4 auditing firm audits financial statements. Therefore, we chose to include this crucial term in our search string for the second category related to assurance.

For Step 3, we began our search by using the Topic field to look for specific keywords in the titles, abstracts, and keywords of publications that align with our study's purpose. Our search focused on discussions about environmental reporting, its assurance, and environmental auditing, which have been explored in relevant papers dating back to the 1990s, such as Huizing and Dekker (1992), Duff (1992), and White et al. (1995). We limited our search to studies published between 1990 and July 31, 2023. Our initial search yielded 740 studies from the WoS database until the end of July 2023.

During Step 4 of our study, we employed several criteria to eliminate research papers that were deemed irrelevant. Our selection focused specifically on studies that underwent a rigorous peer review process, including those classified as early access or review studies. Moreover, we limited our selection to studies written in English. By utilising these filters, we could exclude 107 studies that did not meet our standards.

Finally, step 5 involves saving and exporting the collected data in the appropriate format based on the chosen bibliometric software. For Biblioshiny, the database with full details of the title, abstract, keywords, citations, and references was exported as plain text. For VosViewer, a tab-delimited (Win) file was required. The bibliometric analysis was carried out on a final sample of 633 studies, and the results will be shared in the next section. In 1992, Huizing and Dekker published the first paper on sustainability reporting and assurance in Accounting, Organisations, and Society. This study was a significant effort that drew the research community's attention to essential terms like "environmental reporting," "corporate green reporting", and "environmental auditing" and their impact on the accounting profession (Huizing and Dekker, 1992).

Figure 2. Search protocol for bibliometric analysis

3. Results of bibliometric analysis

Following the recommendations of Donthu et al. (2021), this section utilises bibliometric methods and enrichment techniques, as described in the preceding section, to thoroughly assess the history, present status, and outlook of the SRA field.

3.1. Initial data statistics

Our bibliometric analysis utilised a final set of 633 studies published in 191 journals from 1992 to 2023 and involved 1,339 authors. Of these authors, 61 contributed 67 single-authored documents. The Collaboration Index, calculated by Aria and Cuccurullo (2017) as a Co-authors per article index, was applied to the multi-authored study set and resulted in an index of 2.26 for our sample. A collaboration index of 2.26 indicates a moderate collaboration level in the SRA research field. This means that, on average, there are 2.26 co-authors per multi-authored document in that field (Elango and Rajendran, 2012; Koseoglu, 2016). The average citation per document was 34.71, which suggests that the research in the SRA field is frequently cited and has significant influence (refer to Table 1).

Table 1. Initial data of the final sample

| Description | Results |

|---|---|

| Timespan | 1992-2023 |

| No. of studies | 633 |

| Sources (Journals) | 191 |

| Average citations per document | 34.71 |

| Average years from publication | 3.88 |

| Average citations per year per doc | 5.332 |

| Type of document: Articles | 559 |

| Type of document: Articles - Early access | 43 |

| Type of document: Review | 26 |

| Type of document: Review - Early access | 5 |

| Authors | 1,339 |

| Authors of single-authored documents | 61 |

| Authors of multi-authored documents | 1,278 |

| Single-authored documents | 67 |

| Documents per Author | 0.473 |

| Authors per document | 2.12 |

| Co-Authors per Document | 2.84 |

| Collaboration Index | 2.26 |

Source: generated using Biblioshiny on R Studio on selected data

3.2. Publications’ Trend (RQ1)

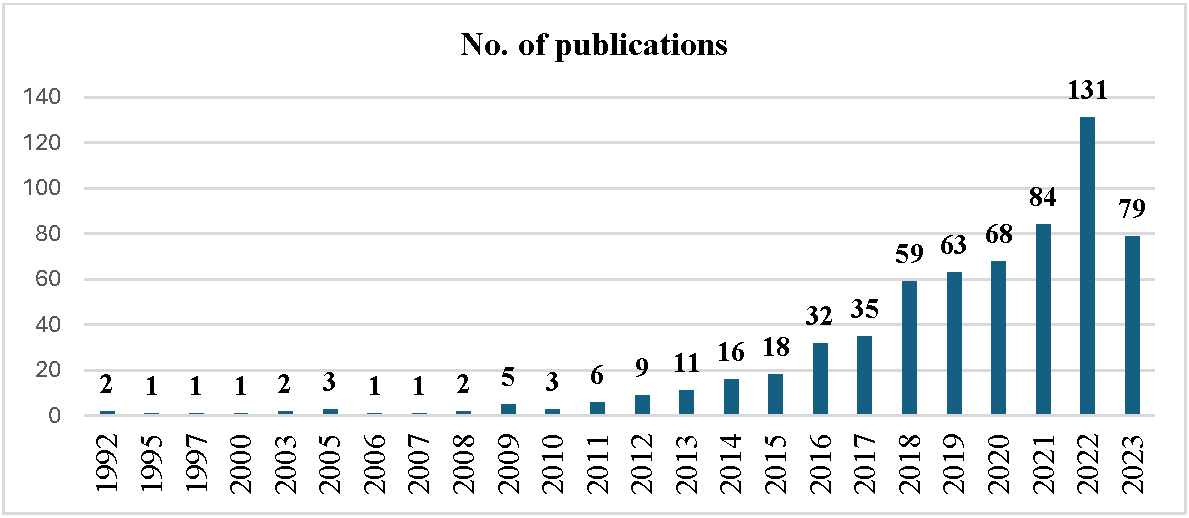

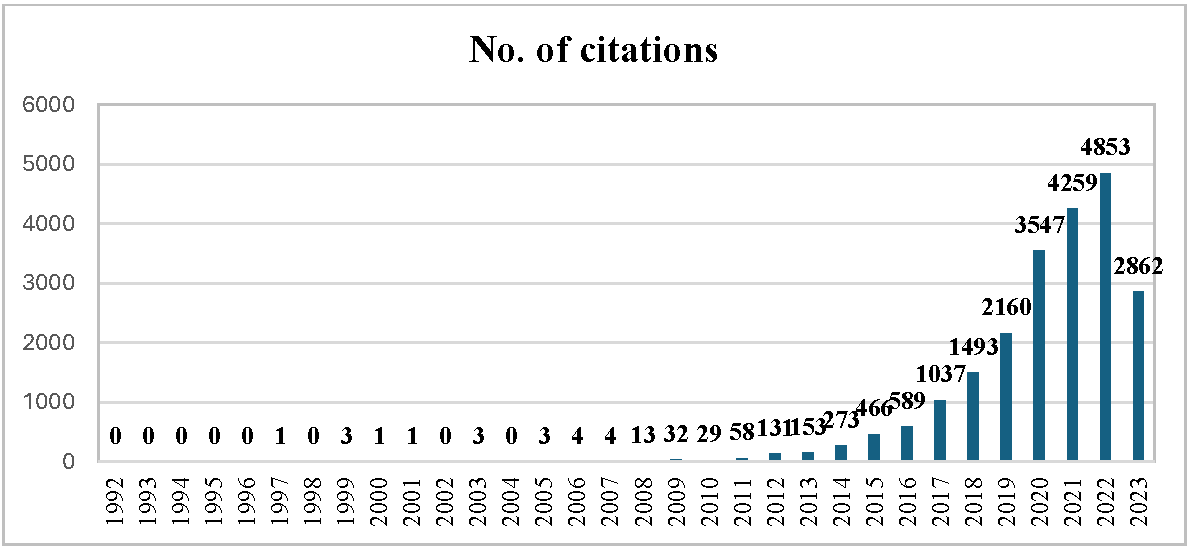

In Figure 3, we can see the number of publications per year in the field of SRA from 1992 to 2023. Figure 4 shows the trend of citations in this field. The research in this area started with a few publications from 1992 to 2010. From 2011 to 2017, there was a more noticeable increase in publications with minor fluctuations. However, there has been a significant surge in scholarly publications in SRA since 2018. Notably, the number of publications has peaked in the last three years (84 in 2021, 131 in 2022, and 79 in 2023 for the first seven months). The number of citations has also shown an upward trend, peaking in 2020-2023, indicating a growing interest in this research field.

The quantity of published works has significantly risen since 2011, with this trend mainly being attributed to the global economic crisis that impacted economies across the globe from 2008 to 2010. During this time, there was an increasing need for more dependable disclosure of financial and non-financial information, which sparked renewed conversations about the necessary assurance for such information (Yan et al., 2022). Additionally, there has been a marked increase in publications since 2018, fuelled by the heightened attention on sustainability reporting assurance among diverse institutions and professional organisations. The growing interest in sustainability reporting is connected to the increasing complexity of challenges faced by professionals who assure these reports' accuracy. While many assurance providers focus on reports from large corporations and groups, there is currently no widely accepted standard for sustainability reporting assurance (European Court of Auditors, 2019).

It's important to note that the IAASB has been working on a new standard called the International Standard on Sustainability Assurance (ISSA) 5000. This standard will be finalised by the end of 2024 and will serve as a globally applicable framework for all sustainability assurance engagements. It will apply to any sustainability information reported under multiple existing frameworks (IAASB, 2023). As discussions and debates around this new assurance standard continue, academic researchers and other stakeholders will focus on understanding the core principles, criteria, and provisions that should be included in a widely recognised sustainability report assurance standard.

Figure 3. Number of publications (yearly trend)

Source: generating using WoS on selected data

Figure 4. Number of citations (yearly trend)

Source: generating using WoS on selected data

3.3. Most impactful journals (RQ2)

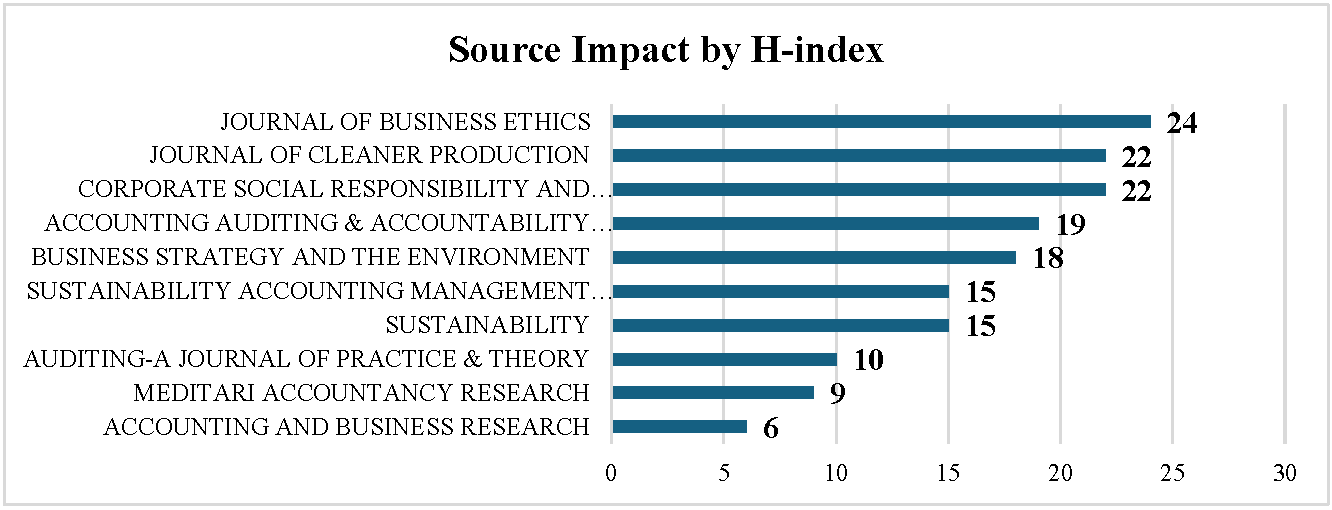

This section aims to provide a comprehensive overview of the primary sources that have contributed to the growth of the field associated with SRA. Our analysis includes a sample of 633 studies published in 191 journals indexed in the WoS database. Table 2 displays the top 20 journals based on the number of citations received for their SRA publications and their respective impact factors. These impact factors are disclosed in the Journal Citation Report (JCR) provided by Thomson Reuters. They are calculated by dividing the number of citations received in the current year by the number of source items published in that journal during the previous two years. In addition, JCR calculates the 5-year impact factor, which represents the average number of times studies from the journal published in the last five years have been cited in the JCR year. According to Xu et al. (2021), even if the impact factor is imperfect, it helps assess journal quality. In the SRA research field, the most influential journals based on publication and citation numbers are the Journal of Business Ethics, Journal of Cleaner Production, Accounting Auditing & Accountability Journal, Corporate Social Responsibility and Environmental Management, and Business Strategy and the Environment. The highest and lowest impact factors among the top 20 journals are Business Strategy and the Environment (13.4) and Accounting and Business Research (1.7). These top 20 journals contribute around 55% to the total publications used in this bibliometric analysis. It's worth noting that while some journals have a significant number of publications in SRA (e.g., Sustainability with 53 publications and 756 citations), they don't rank highly in terms of article citations.

According to Figure 5, we can see the top 10 most influential journals in the field of SRA. The ranking is based on their h-index, which measures the number of studies published by a journal that have at least the same number of citations (Hirsch, 2005). The top 5 journals listed in Table 2 also rank among the top 5 journals based on their h-index, but not necessarily in the same order. For instance, the Journal of Business Ethics has at least 24 publications cited at least 24 times. In contrast, the Journal of Cleaner Production and Corporate Social Responsibility and Environmental Management have at least 22 papers cited at least 22 times. Accounting Auditing & Accountability Journal has at least 19 publications cited at least 19 times, and Business Strategy and the Environment has at least 18 publications cited at least 18 times.

Table 2. Top 20 journals ranked by the total number of citations for the publications SRA.

| Rank | Source | N | TC | AC | IF | 5Y-IF | Publisher | WOS Index |

|---|---|---|---|---|---|---|---|---|

| 1 | Journal of Business Ethics | 29 | 2,434 | 83.93 | 6.1 | 8.1 | Springer | SSCI |

| 2 | Journal of Cleaner Production | 39 | 2,309 | 59.21 | 11.1 | 11.0 | Elsevier | SCIE |

| 3 | Accounting Auditing & Accountability Journal | 24 | 1,818 | 75.75 | 4.2 | 5.5 | Emerald | SSCI |

| 4 | Corporate Social Responsibility and Environmental Management | 39 | 1,612 | 41.33 | 9.8 | 10.6 | Wiley | SSCI |

| 5 | Business Strategy and the Environment | 28 | 1,348 | 48.14 | 13.4 | 14.3 | Wiley | SSCI |

| 6 | Auditing-a Journal of Practice & Theory | 10 | 1,113 | 111.30 | 2.8 | 3.7 | American Accounting Association | SSCI |

| 7 | Sustainability Accounting Management and Policy Journal | 32 | 802 | 25.06 | 4.5 | 4.7 | Emerald | SSCI |

| 8 | Sustainability | 53 | 756 | 14.26 | 3.9 | 4.0 | MDPI | SSCI, SCIE |

| 9 | Australian Accounting Review | 6 | 393 | 65.50 | 3.4 | 3.3 | Wiley | SSCI |

| 10 | Accounting and Business Research | 7 | 391 | 55.86 | 1.7 | 3.2 | Taylor & Francis | SSCI |

| 11 | Meditari Accountancy Research | 23 | 326 | 14.17 | 3.5 | 3.7 | Emerald | ESCI |

| 12 | Contemporary Accounting Research | 7 | 324 | 46.29 | 3.6 | 4.9 | Wiley | SSCI |

| 13 | Accounting and Finance | 5 | 233 | 46.60 | 2.6 | 3.0 | Wiley | SSCI |

| 14 | Social Responsibility Journal | 13 | 193 | 14.85 | 3.2 | 3.9 | Emerald | ESCI |

| 15 | Managerial Auditing Journal | 7 | 140 | 20.00 | 2.9 | 3.2 | Emerald | SSCI |

| 16 | Journal of Applied Accounting Research | 9 | 127 | 14.11 | 3.0 | 3.4 | Emerald | ESCI |

| 17 | Journal of Management & Governance | 5 | 121 | 24.2 | 2.7 | 2.8 | Springer | ESCI |

| 18 | Administrative Sciences | 5 | 89 | 17.80 | 3.0 | 3.0 | MDPI | ESCI |

| 19 | International Journal of Auditing | 5 | 74 | 14.8 | 2.0 | 2.4 | Wiley | SSCI |

| 20 | Sustainable Development | 5 | 73 | 14.6 | 12.5 | 10.1 | Wiley | SSCI |

Note: N- number of studies, TC-total citations, AC-average citations per publication per each journal, IF-the last journal impact factor (derived from JCR 2023), 5Y-IF – the last five years impact factor (derived from JCR 2023). ESCI - Emerging Sources Citation Index; SSCI - Social Sciences Citation Index; Science Citation Index Expanded – SCIE. It is important to note that for ESCI journals, the calculation of Journal Impact Factors has started with the Edition of Journal Citation Report (JCR) released in June 2023.

Figure 5. Publications impact by H-index

Source: generated using Biblioshiny on R Studio on selected data

3.4. Most impactful publications (RQ2)

According to several researchers (Xu et al., 2021; Wang et al., 2021), the number of citations a publication receives helps measure its quality and influence. We use bibliometric measures like the global citation score (GCS) and local citation score (LCS) to determine the most impactful papers in a particular field. The GCS is the total number of citations a publication has received from all studies indexed in the WoS database, while the LCS is the number of citations a paper has received within its field (Munim et al., 2020; Kumar et al., 2021). However, it's important to note that newer publications may not have as many citations as older ones simply because they haven't accumulated enough time. As a result, older publications may appear more impactful than more recent ones.

Based on the data in Table 3, we have classified and ranked the top 10 studies related to SRA research based on GCS and LCS. The LCS indicates the number of citations within our sample

of 633 studies. Notably, "Assurance on Sustainability Reports: An International Comparison" (Simnett et al., 2009) is top in GCS and LCS rankings. With the most global and local citations, this study is highly significant in comprehending the emerging voluntary assurance market for sustainability reports. Simnett et al. (2009) analysed data from 2,113 companies across 31 countries that published sustainability reports between 2002 and 2004. Their study revealed that companies looking to establish the credibility of their sustainability reports and corporate reputation are more likely to seek assurance for their reports. Furthermore, firms operating in stakeholder-focused countries tend to choose auditing professionals as their assurance providers. Among the most influential papers, ranking highly in terms of LCS is "Determinants of the Adoption of Sustainability Assurance Statements: An International Investigation" by Kolk and Perego (2010). This study sheds light on the factors influencing companies' decisions to adopt sustainability assurance statements. According to their findings, companies operating in countries with a stronger focus on stakeholders and less strict governance enforcement are likelier to adopt such statements. Additionally, the study highlights that companies in shareholder-oriented countries with lower levels of litigation tend to choose larger accounting firms as their assurance providers (Kolk and Perego, 2010).

Table 3. Most impactful papers

| Rank | Paper | DOI | GCS | TC/Y | Rank | Document | DOI | LCS | GCS | LCS/GCS Ratio (%) |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Simnett R, 2009, Account Rev | 10.2308/accr.2009.84.3.937 | 679 | 45.27 | 1 | Simnett R, 2009, Account Rev | 10.2308/accr.2009.84.3.937 | 270 | 679 | 39.76 |

| 2 | Hahn R, 2013, J Clean Prod | 10.1016/j.jclepro.2013.07.005 | 662 | 60.18 | 2 | Kolk A, 2010, Bus Strateg Environ | 10.1002/bse.643 | 156 | 356 | 43.82 |

| 3 | Michelon G, 2015, Crit Perspect Accoun | 10.1016/j.cpa.2014.10.003 | 420 | 46.67 | 3 | Pflugrath G, 2011, Auditing-J Pract Th | 10.2308/ajpt-10047 | 133 | 232 | 57.33 |

| 4 | De Villiers C, 2014, Account Audit Accoun | 10.1108/AAAJ-06-2014-1736 | 412 | 41.20 | 4 | Perego P, 2012, J Bus Ethics | 10.1007/s10551-012-1420-5 | 126 | 262 | 48.09 |

| 5 | Boiral O, 2013, Account Audit Accoun | 10.1108/AAAJ-04-2012-00998 | 363 | 33.00 | 5 | Hodge K, 2009, Aust Account Rev | 10.1111/j.1835-2561.2009.00056.x | 125 | 187 | 66.84 |

| 6 | Rennings K, 2006, Ecol Econ | 10.1016/j.ecolecon.2005.03.013 | 359 | 19.94 | 6 | Cohen JR, 2015, Auditing-J Pract Th | 10.2308/ajpt-50876 | 113 | 226 | 50.00 |

| 7 | Kolk A, 2010, Bus Strateg Environ | 10.1002/bse.643 | 356 | 25.43 | 7 | Hahn R, 2013, J Clean Prod | 10.1016/j.jclepro.2013.07.005 | 112 | 662 | 16.92 |

| 8 | O'dwyer B, 2011, Account Org Soc | 10.1016/j.aos.2011.01.002 | 327 | 25.15 | 8 | O'dwyer B, 2011, Account Org Soc | 10.1016/j.aos.2011.01.002 | 105 | 327 | 32.11 |

| 9 | Perego P, 2012, J Bus Ethics | 10.1007/s10551-012-1420-5 | 262 | 21.83 | 9 | Manetti G, 2009, J Bus Ethics | 10.1007/s10551-008-9809-x | 103 | 179 | 57.54 |

| 10 | Fernandez-Feijoo B, 2014, J Bus Ethics | 10.1007/s10551-013-1748-5 | 254 | 25.40 | 10 | Casey Rj, 2015, Auditing-J Pract Th | 10.2308/ajpt-50736 | 97 | 187 | 51.87 |

Source: generated using Biblioshiny on R Studio on selected data

Note: GCS-global citation score; TC/Y- total citations / year; LCS-local citation score; LCS / GCS ratio (%) – ratio between local citation score and global citation score

3.5. Most influential, productive, and collaborative authors (RQ3)

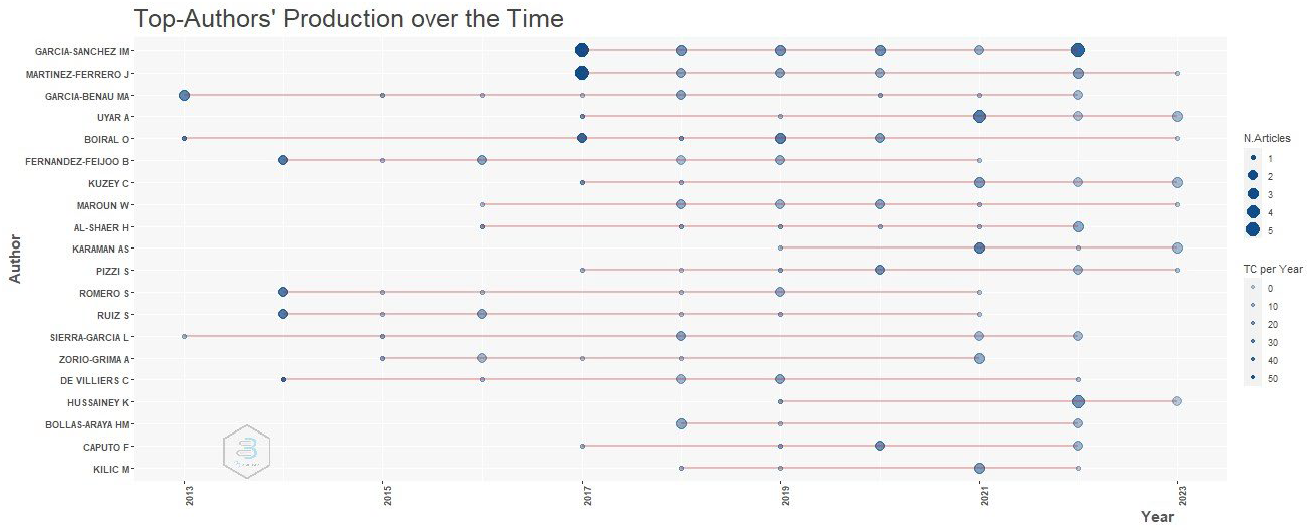

This section contains a thorough bibliometric analysis, which provides a comprehensive understanding of the most productive and influential authors who have significantly contributed to developing the SRA research field. Table 4 highlights the top 20 authors with the most citations and other relevant information, such as their impact (H-indices, G-indices, M-indices, total citations) and the year of their first publication. As Zabavnik and Verbi (2021) mentioned, evaluating a researcher's scientific production often involves considering indicators beyond the H-index. According to Egghe (2006), the G-index is an improvement over the H-index, as it offers a more comprehensive assessment of global citation performance. This index assigns greater weight to highly-cited papers within a dataset. Another variation of the H-index is the M-index, which factors in the number of years an author has been conducting research since their first publication, assuming continuous activity (as outlined by Zabavnik and Verbi, 2021). The authors with the highest total citations are Simnett R., Boiral O., and Hahn R., with 1,236, 989, and 914 citations, respectively. According to the H-index, G-index, and M-index, Garcia-Sanchez I.M. is considered the most influential author, with an H-index of 17, G-index of 21, and M-index of 2.429. Figure 6 showcases the productivity of top authors in this research field, depicting Garcia-Sanchez I.M. as the author with the most published studies. The size of the bubbles in Figure 6 represents the number of studies published by each author, providing a visual timeline of each author's scientific activity in this field of research. According to Zabavnik and Verbi (2021), the intensity of the colour of the bubbles in Figure 6 reflects the total number of citations received each year. This data shows that Garcia-Sanchez I.M., Martinez-Ferrero J., Garcia-Benau M.A., Uyar A., and Boiral A. were the most prolific authors regarding publications and citations. Garcia-Sanchez I.M. has been actively contributing to scientific discussions for over seven years. Additionally, Figure 6 indicates a positive trend in scientific activity over the past six years, which corresponds with the publication trend outlined in Section 3.2.

Table 4 . Top 20 most impactful authors in terms of the number of total citations

| Rank | Authors | TC | h_index | g_index | m_index | NP | PY_start |

|---|---|---|---|---|---|---|---|

| 1 | Simnett R. | 1236 | 6 | 6 | 0.286 | 6 | 2003 |

| 2 | Boiral O. | 989 | 8 | 9 | 0.727 | 9 | 2013 |

| 3 | Hahn R. | 914 | 4 | 4 | 0.364 | 4 | 2013 |

| 4 | Unerman J. | 835 | 4 | 4 | 0.308 | 4 | 2011 |

| 5 | Garcia-Sanchez I.M. | 815 | 17 | 21 | 2.429 | 21 | 2017 |

| 6 | Perego P. | 726 | 3 | 3 | 0.214 | 3 | 2010 |

| 7 | Chua W.F. | 679 | 1 | 1 | 0.067 | 1 | 2009 |

| 8 | Vanstraelen A | 679 | 1 | 1 | 0.067 | 1 | 2009 |

| 9 | Kuhnen M. | 662 | 1 | 1 | 0.091 | 1 | 2013 |

| 10 | O'dwyer B. | 653 | 5 | 5 | 0.385 | 5 | 2011 |

| 11 | Garcia-Benau M.A. | 632 | 10 | 12 | 0.909 | 12 | 2013 |

| 12 | Kolk A. | 618 | 2 | 2 | 0.143 | 2 | 2010 |

| 13 | Martinez-Ferrero J. | 606 | 10 | 14 | 1.429 | 14 | 2017 |

| 14 | De Villiers C. | 586 | 7 | 7 | 0.7 | 7 | 2014 |

| 15 | Fernandez-Feijoo B. | 569 | 7 | 10 | 0.7 | 10 | 2014 |

| 16 | Ruiz S. | 557 | 7 | 8 | 0.7 | 8 | 2014 |

| 17 | Michelon G. | 485 | 2 | 2 | 0.222 | 2 | 2015 |

| 18 | Romero S. | 483 | 7 | 8 | 0.7 | 8 | 2014 |

| 19 | Pilonato S. | 420 | 1 | 1 | 0.111 | 1 | 2015 |

| 20 | Ricceri F. | 420 | 1 | 1 | 0.111 | 1 | 2015 |

Source: generated using Biblioshiny on R Studio on selected data

Note: TC- total citations; PY_start - year of the first author’s publication; NP – number of publications

Figure 6. Top 20 Authors production over time

Source: generated using Biblioshiny on R Studio on selected data

Co-authorship analysis is another pertinent analysis for exploring intellectual collaboration among authors in a specific research field. This type of analysis holds particular significance as it provides insights into the patterns of scientific collaboration within a given research field (Donthu et al., 2021; Wang et al., 2021; Bota-Avram, 2023). Moreover, it offers insights into how this collaboration shapes the evolution of the research field under examination. In our dataset of 633 studies, we identified a total of 1,369 authors. We established a minimum threshold of three publications per author and a minimum of 5 citations per author. This refined set encompassed 30 authors who met these criteria. Table 5 displays the top 20 authors with the strongest connections in co-authorship, using data selected through VosViewer. Additionally, Figure 7, generated by Biblioshiny on R Studio, provides a clear visual of scientific collaboration among these authors. The collaboration network effectively highlights the main clusters of collaborative activities through author clusters. Each node represents an author, and the links show their co-authorships. This network is recognised as one of the most well-documented forms of scientific collaboration (Aria and Cuccurullo, 2017).

Upon analysing the collaborative efforts of the most productive authors among the selected 633 studies, it is evident that the authors featured in Table 5 and Figure 7 have worked alongside fellow researchers to produce a considerable body of valuable work. These collaborations have yielded notable contributions to the field of research, including:

A prominent cluster within the collaboration network, as indicated in Figure 7 (Red Cluster), comprises the authors Garcia-Sanchez I.M., Martinez-Ferrero, J., and Ruiz-Barbadillo, E. This team has played a crucial role in analysing different aspects of ensuring sustainability reports. Their research has provided valuable insights into the impact of various company governance mechanisms, including board diversity, board independence, the presence of CSR committees, and gender diversity, on the decision to externally verify CSR reports and the choice of assurance providers. Their work has been published in several papers, including García-Sánchez et al. (2022), García-Sánchez and Martinez-Ferrero (2019), and Martínez-Ferrero and García-Sánchez (2017a). Additionally, their work sheds light on the diversity of professional backgrounds and experiences among assurance providers (Ruiz-Barbadillo and Martínez-Ferrero, 2022a; Martínez-Ferrero et al., 2018; Martínez-Ferrero and García-Sánchez, 2018) and the duration of the contractual relationship between clients and assurance providers (Ruiz-Barbadillo and Martínez-Ferrero, 2022b), which results in significant variations in the quality of sustainability assurance. This team has also made valuable contributions by investigating the impact of CSR reporting, its external assurance, and the level of assurance quality on the access to financial resources for reporting firms (García-Sánchez et al., 2019) and the cost of capital (Martínez-Ferrero et al., 2021; Martínez-Ferrero and García-Sánchez, 2017b). Furthermore, their work has made significant contributions to understanding how country- and industry-specific factors may impact the decision to adopt assurance for sustainability reports (Martínez-Ferrero and García-Sánchez, 2017c) and how country-specific factors influence the level of assurance in sustainability reports—limited/moderate vs. reasonable/high assurance (Ruiz-Barbadillo and Martínez-Ferrero, 2020).

Another significant team in the collaboration network, as depicted in Figure 7 (Green Cluster), consists of the authors Uyar, A., Kuzey, C., Karaman, A.S. and Kiliç, M. (who are also ranked among the top eight positions in Table 5). Recently, these authors have examined how economic and cultural corporate characteristics relate to CSR reporting and assurance. Their work includes investigations into various aspects of firm investment (such as sales growth, R&D intensity and total tangible and intangible assets) and their connection to CSR reporting and external assurance (Meftah et al., 2023), the influence of audit committee independence and expertise (Uyar et al., 2023), the impact of ethical behaviour by firms and the strength of accountability regulations on sustainability reporting practises and external assurance in the hospitality and tourism sector (Hamrouni et al., 2023), the role of national culture in decisions to assure integrated reports (Uyar et al., 2022a), shareholders' perceptions of CSR reporting companies with higher firm value due to the attainment of assurance for CSR reports (Uyar et al., 2022b), connections among CSR performance, reporting, and external assurance in the hospitality and tourism industry (Koseoglu et al., 2021), the influence of country-specific factors associated with the decision to adopt voluntary assurance on integrated reports, the level of assurance quality and the choice of assurance provider (Kiliç et al., 2021a), connections among CSR performance, reporting, and its assurance in the energy sector (Karaman et al., 2021), the consequences of sustainability committee existence on sustainability reports and their external assurance in hospitality and tourism firms (Kiliç et al., 2021b), and exploring the factors that could impact the adoption of assurance statements in sustainability reports (Kuzey and Uyar, 2017).

Moreover, a notable cluster of influential and collaborative authors, as illustrated in Figure 7 (Orange Cluster), comprises Fernandez-Feijoo, B., Romero, S., and Ruiz, S. These authors have focused on the sustainability assurance market. Therefore, these authors have investigated the structure of the sustainability assurance market and how regional differences could impact the specialisation of the industry in this market (Fernandez-Feijoo et al., 2018). The role of professional accountants and the significance of the four major accounting firms (Big4) in the sustainability assurance market (Fernandez-Feijoo et al., 2018b; Fernandez-Feijoo et al., 2016; Fernandez-Feijoo et al., 2015) were also significant areas of focus for this group of researchers. Furthermore, they also explored how independent sustainability reporting assurance could serve as a credibility and transparency mechanism for sustainability reporting (Fernandez-Feijoo et al., 2014). Their research indicates that the quality of CSR reports is improved by adopting Global Reporting Initiative (GRI) guidelines and including an assurance statement (Romero et al., 2019).

Another significant group of authors (the Blue Cluster in Figure 7) comprises Garcia-Benau, M.A., Sierra-Garcia, L., and Zorio-Grima, A. These authors have made significant contributions in this field, including studies on sustainability reporting practices in Spanish public universities and the factors influencing their external assurance (Zorio-Grima et al., 2018; Sierra-García et al., 2015). They have also explored the impact of factors like industry, size, profitability, and leverage on a company's decision to provide external assurance for their CSR reports (Sierra et al., 2013), proposed an index for measuring the quality of CSR report assurance (Zorio et al., 2013), and investigated the effects of the 2008-2010 financial crisis on CSR reporting and assurance strategies (García-Benau et al., 2013).

Table 5. Top 20 most collaborative authors for the selected sample

| Rank | Author | Documents | Citations | Total Link Strength |

|---|---|---|---|---|

| 1 | Uyar, Ali | 11 | 286 | 25 |

| 2 | Kuzey, Cemil | 10 | 272 | 22 |

| 3 | Karaman, Abdullah S. | 8 | 125 | 20 |

| 4 | Fernandez-Feijoo, Belen | 10 | 569 | 16 |

| 5 | Romero, Silvia | 8 | 483 | 15 |

| 6 | Ruiz, Silvia | 8 | 557 | 15 |

| 7 | Martinez-Ferrero, Jennifer | 15 | 556 | 14 |

| 8 | Kiliç, Merve | 6 | 134 | 13 |

| 9 | Garcia-Sanchez, Isabel-Maria | 17 | 665 | 11 |

| 10 | Caputo, Fabio | 6 | 224 | 9 |

| 11 | Pizzi, Simone | 8 | 237 | 9 |

| 12 | Ruiz-Barbadillo, Emiliano | 6 | 124 | 8 |

| 13 | Al-Shaer, Habiba | 8 | 395 | 6 |

| 14 | Boiral, Olivier | 10 | 989 | 5 |

| 15 | Garcia-Benau, Maria A. | 5 | 415 | 5 |

| 16 | Heras-Saizarbitoria, Inaki | 5 | 217 | 5 |

| 17 | Sierra-Garcia, Laura | 8 | 296 | 5 |

| 18 | Zorio-Grima, Ana | 8 | 241 | 5 |

| 19 | Zaman, Mahbub | 5 | 339 | 4 |

| 20 | Hussainey, Khaled | 7 | 125 | 2 |

Source: generated using VosViewer on selected data

Note: Total link strength refers to the cumulative strength of the co-authorship connections between a specific author and other authors

Figure 7. The collaboration network of the authors

Source: generated using Biblioshiny on R Studio on selected data

3.6. Cooperation networks among countries/regions and institutions (RQ3)

To explore the collaborative networks among countries and regions in this research field, we will examine the selected sample of published papers from the following angles: the most prolific countries and regions, the most active institutions, and the interrelationships among countries, keywords, and journals.

3.6.1. Most productive and influential countries

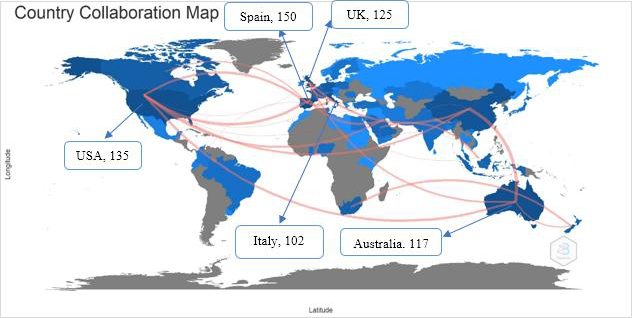

The 633 papers in our sample are related to 71 countries and regions. Next, Figure 8, produced with the aid of Biblioshiny on R Studio software, showcases a detailed map of these countries' collaborative efforts. The map's red lines denote the collaborative relationships between countries, while blue indicates the number of publications. The darker shades of blue correspond to the countries with the most publications. (Wang et al., 2021). The research of SRA has captured significant attention globally, attracting notable researchers from the United States, Australia, Asia (including China and Malaysia), and Europe (encompassing nations such as Spain, the United Kingdom, Italy, France, and Germany). The key contributors to this field are based in Spain, the United States, the United Kingdom, Australia, and Italy.

Figure 8. Countries collaboration map

Source: generated using Biblioshiny on R Studio on selected data

Table 6. The top 10 countries ranked by the number of publications

| Rank | Country | N | TC | AVA | AVY |

|---|---|---|---|---|---|

| 1 | SPAIN | 150 | 2423 | 16.15 | 31.06 |

| 2 | USA | 135 | 2375 | 17.59 | 43.98 |

| 3 | UNITED KINGDOM | 125 | 2048 | 16.38 | 46.55 |

| 4 | AUSTRALIA | 117 | 3034 | 25.93 | 45.97 |

| 5 | ITALY | 102 | 1651 | 16.19 | 35.13 |

| 6 | CHINA | 92 | 482 | 5.24 | 14.61 |

| 7 | GERMANY | 46 | 2132 | 46.35 | 66.62 |

| 8 | CANADA | 38 | 1559 | 41.03 | 74.24 |

| 9 | FRANCE | 37 | 318 | 8.59 | 31.80 |

| 10 | MALAYSIA | 33 | 115 | 3.48 | 10.45 |

Note: N-number of publications, TC-total citations, AVA-average citations per article, ACY–average citations per year

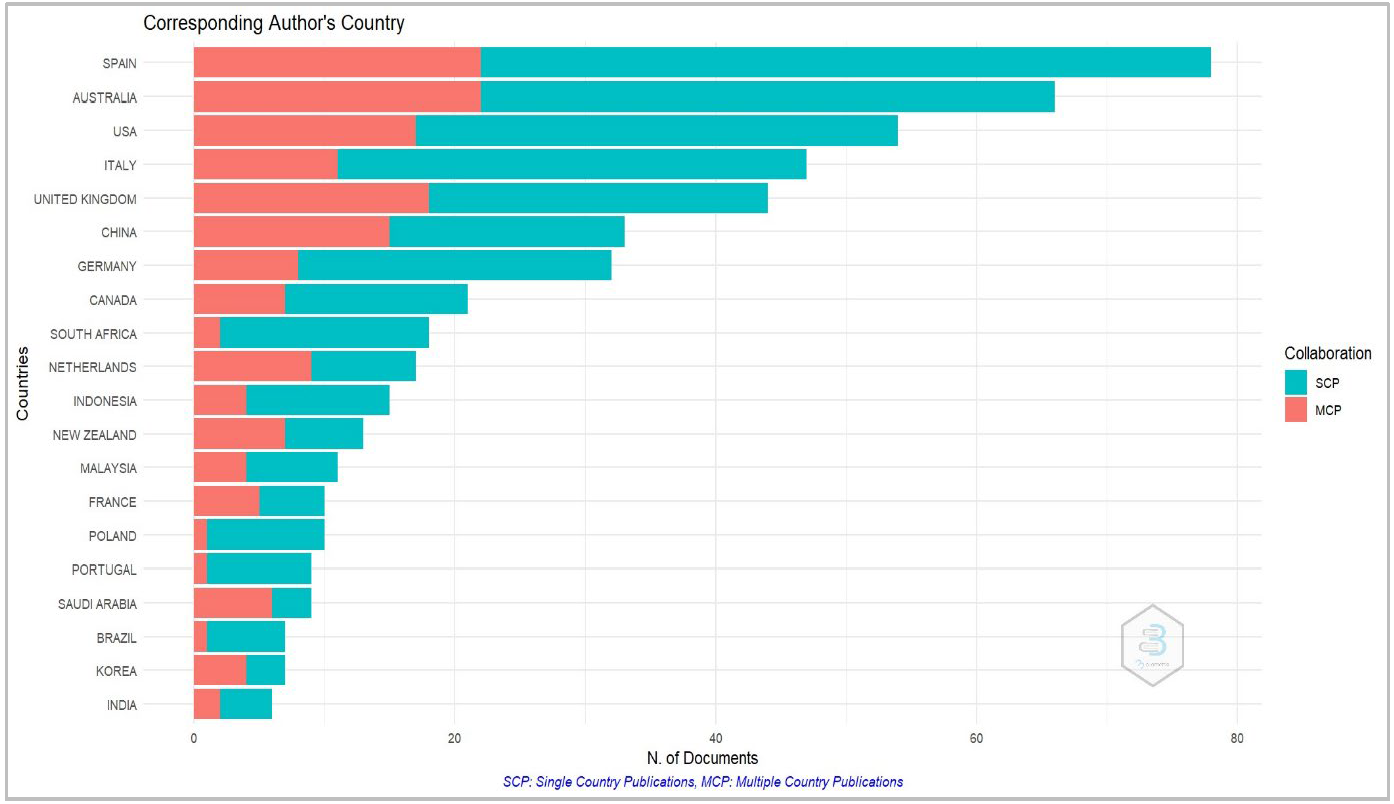

According to Table 6, the top 10 countries/regions with the highest number of publications are listed with their total citations (TC), average citations per article (AVA), and average citations per year (AVY). The leading countries in publications and citations are Spain, the United States, the United Kingdom, Australia, and Italy. It's worth noting that the countries that rank highest in citation analysis and collaboration network analysis are often the same, albeit with varying positions. It's also interesting to observe that several countries with relatively fewer published papers in this field have garnered many citations. For instance, with just 46 papers, Germany has garnered an impressive 2,132 citations, making it the country with the highest average citations per article at 46.35. Similarly, with 38 papers, Canada has the second-highest citations per article at 41.03. Finally, when analysing the most productive countries from the perspective of the corresponding author's country, Figure 9 sheds light on the top 20 most productive countries. It considers two indicators: SCP (single country publications), where all authors originate from the same country, and MCP (multiple country publications), which indicates international collaboration among authors from different countries. Interestingly, the leading countries in this perspective remain the same: Spain, Australia, the United States, Italy, and the United Kingdom.

Spain's position as a leader in research comes as no surprise, considering its longstanding reputation as a world leader in CSR reporting, as noted by KPMG (2011) and further demonstrated by Sierra et al. (2013) and Zorio et al. (2013). Spanish scholars, as discussed in Section 3.5, have also made significant contributions to this field and continue to be among its most influential and prolific authors. It is worth noting that until 2021, the EU's Non-Financial Reporting Directive allowed member states to mandate independent assurance for non-financial information. Spain, France, and Italy were among the countries that chose to have such information verified. However, the specific legal framework did not mandate the assurance provider to be a professional accountant.

Figure 9. Top 20 most productive countries from the perspective of the corresponding authors country

Source: generated using Biblioshiny on R Studio on selected data

3.6.2. Most productive institutions

This section examines the cooperation network among contributing institutions in the field of SRA research. Based on a sample of 633 studies related to SRA research, our bibliometric data reveal that 730 institutions have academics involved in developing this research field. The top five most productive institutions, in terms of the number of studies produced in this field, include the University of Salamanca in Spain (29 studies with 920 citations), followed by the University of Valencia in Spain (21 studies with 731 citations), RMIT University in Australia (11 studies with 212 citations), Vigo University in Spain (10 studies with 569 citations), and Newcastle University in the UK (10 studies with 398 citations). It is worth noting that, once again, Spanish academic institutions have significantly impacted the SRA research field, with three of the top five institutions hailing from Spain.

3.6.3. Interconnections among countries, keywords, and journals - Three fields plot

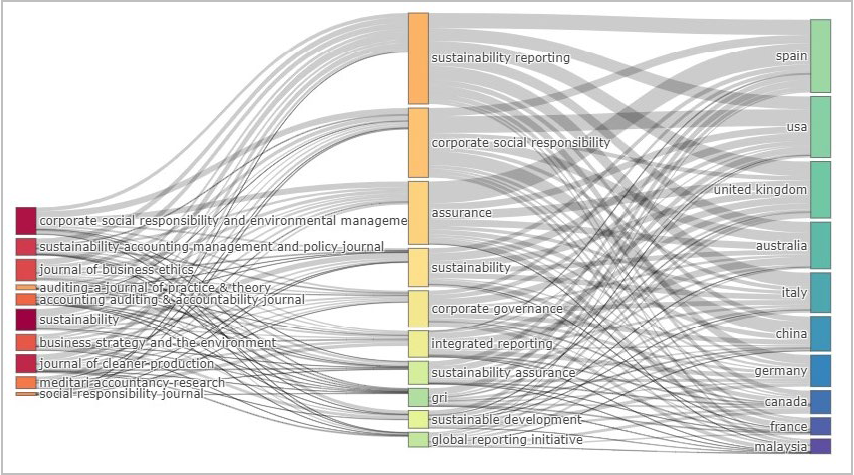

The interconnections among the most relevant journals (left), author keywords (middle), and countries (right) can emphasise helpful information about the proportion of research topics most developed for each country and the primary publication outlets where these studies were disseminated. Based on the Sankey diagram, this innovative visualisation can be crafted using Biblioshiny on R Studio software. Notably, the size of the boxes in the plot is contingent on the frequency of their occurrences (Abhishek and Srivastava, 2021).

Figure 10 presents a three-field plot for journals, author keywords, and countries within the SRA research field. This figure shows that studies on SRA are predominantly published in journals such as Corporate Social Responsibility and Environmental Management, Journal of Business Ethics, Sustainability, Sustainability Accounting Management and Policy Journal, Business Strategy and the Environment, and Journal of Cleaner Production. Many of these studies are authored by scholars from Spain, the United States, the United Kingdom, Australia, and Italy. The valuable contributions of Spanish researchers in the field of SRA are once again evident. Many of the studies authored by Spanish researchers focus on topics such as "assurance", "sustainability reporting" and "sustainability assurance”. The issues of "sustainability reporting," "assurance," and "sustainability assurance" are primarily explored by researchers from Spain, the United States, the United Kingdom, Australia, and Italy. At the aggregate level, Figure 10 illustrates those European countries (Spain, the United Kingdom, Italy, Germany, and France) that show a greater interest in topics such as "corporate social responsibility," "assurance," "sustainability reporting," and "sustainability assurance."

Figure 10. The three-field plot of journals, author keywords, and countries

Source: generated using Biblioshiny on R Studio on selected data

3.7. Analysis of the keywords (RQ4)

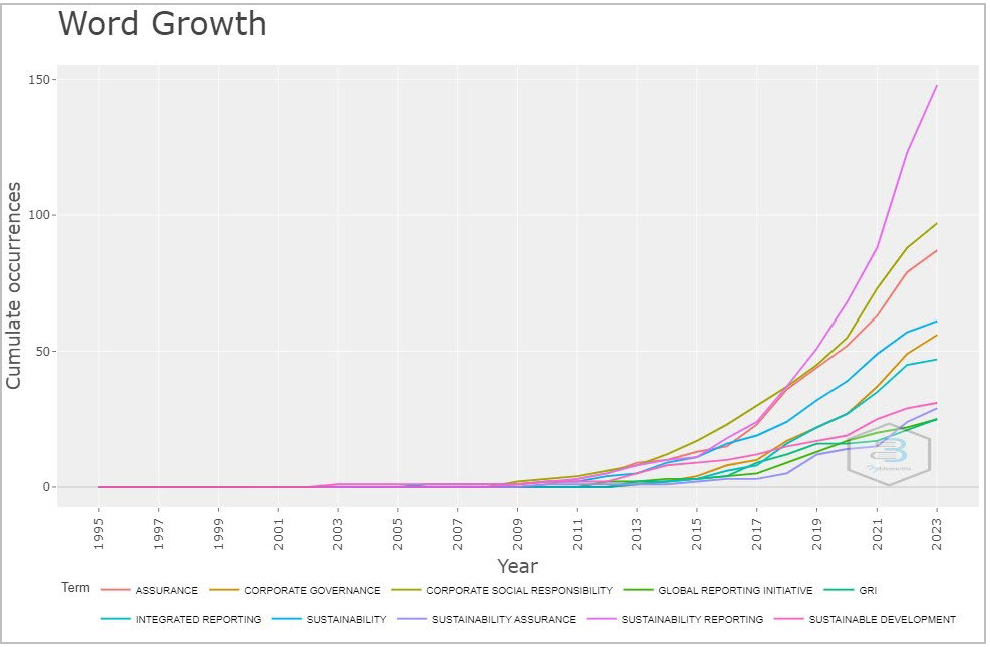

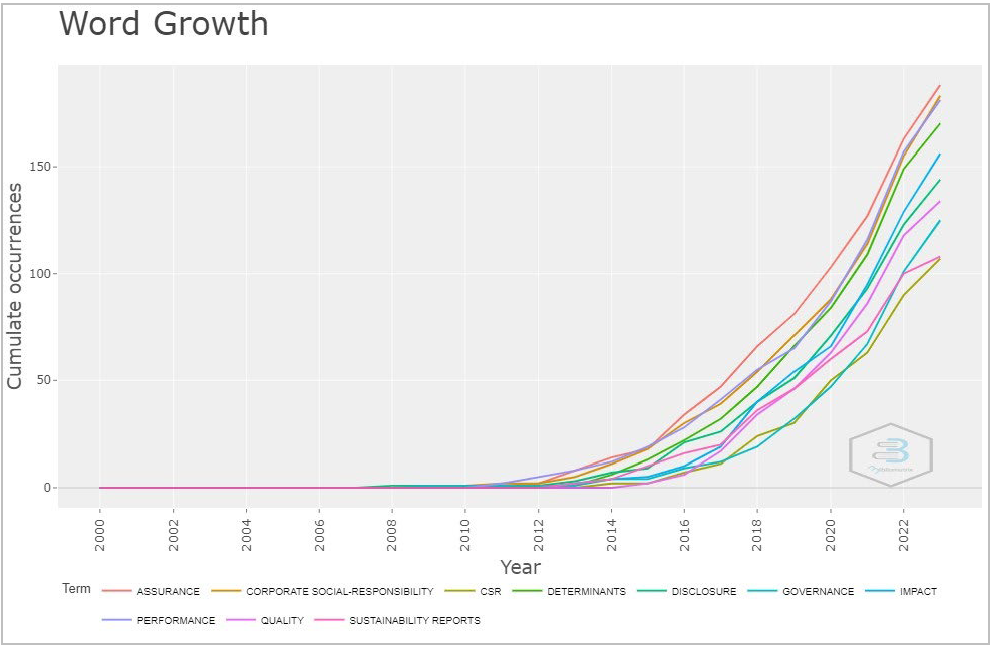

This section aims to provide insights into developing literature in the SRA research field. We analysed the most frequently used keywords using the bibliometric software tool Biblioshiny in R Studio to achieve this. The keyword analysis highlights the most significant research trends. Therefore, we used a comparative approach to identify the most critical keywords in SRA literature by analysing the frequency of authors' keywords compared to Keywords Plus. An analysis of the most frequently used words in the authors' keywords revealed that the term “sustainability reporting” was used 148 times, followed by “corporate social responsibility’ (212 times) and “assurance” (87 times). The same analysis applied to Keywords Plus revealed that the following terms were found to be more frequent: "assurance" (188 times), "corporate social responsibility" (183 times), "performance” “determinants" (170), and "impact" (156 times). Next, Figure 11 a) reveals a visual representation of the most frequently used author keywords in the form of a word cloud, along with a graphical representation showing the cumulative growth of occurrences of author keywords over the analysed period of nearly 30 years. Figure 11 b) provides the same visual representations but for Keywords Plus. Figure 11 a) shows that the term "sustainability reporting" has experienced a significant surge in usage since 2015-2016. Additionally, other words like "corporate social responsibility", "assurance", and "sustainability" have shown a notable increase in their use within author keywords since 2017-2018, with a particularly pronounced uptick in the last three years (2021-2023). Continuing with the same analysis for Keywords Plus, as shown in Figure 11 b), it's noticeable that terms like "assurance," "corporate social responsibility," and "performance" experienced a remarkable surge in their usage from 2016 onwards. When comparing author keywords with Keywords Plus, it's noteworthy that the most frequent words, "assurance" and "corporate social responsibility," appear at the top of the lists for both sets of keywords. For Keywords Plus, terms like "determinants," "impact," "disclosure," and "quality" suggest that researchers in the SRA field are primarily focused on investigating the determinants of CSR performance, how assurance can enhance CSR reporting quality, and examining the impact of external assurance on CSR disclosure.

Figure 11 a) Word cloud and word growth of author keywords cumulates over the analysed period

Source: generated using Biblioshiny on R Studio on selected data

Figure 11 b) Word cloud and word growth of Keywords Plus cumulates over the analysed period

Source: generated using Biblioshiny on R Studio on selected data

3.8. Emerging trends (RQ4)

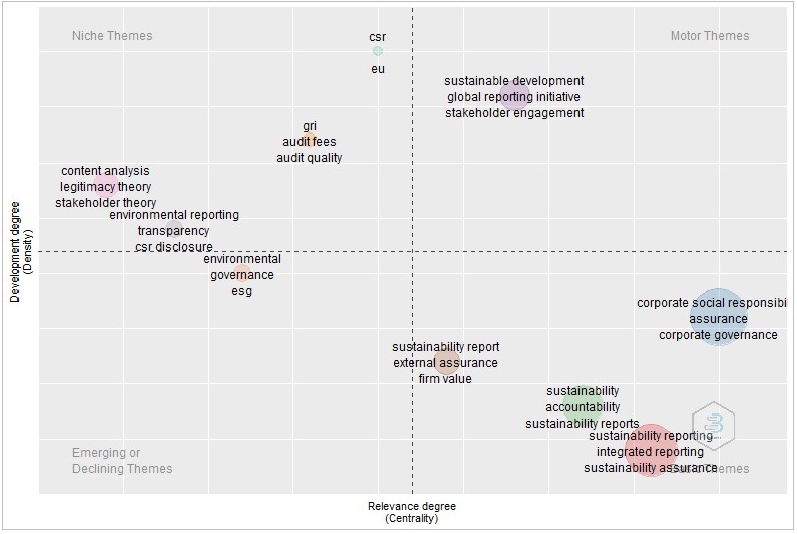

To enhance our understanding of evolving topics and emerging trends in the research field under investigation, we conducted a thematic map analysis of research themes using the Biblioshiny software in R Studio. Thematic map analysis was carried out with 400 keywords and a minimum of 10 cluster frequencies (per thousand documents), generating 7 clusters. The thematic map analysis provided by Biblioshiny is based on two dimensions: centrality and density. Each cluster is depicted as a circle, with its size corresponding to the number of terms it encompasses (Abhishek and Srivastava, 2021). Within a cluster, centrality signifies the impact of its links with other clusters. The greater the amount and strength of these links, the more prominent the cluster is as a crucial research topic within the scientific community in that particular field of study (Callon et al., 1991; Abhishek and Srivastava, 2021). Density measures the strength of connections within a cluster, indicating development and integrating research themes (Callon et al., 1991; Abhishek and Srivastava, 2021). Thus, according to centrality and density, the thematic map is divided into quadrants, allowing classification into 4 categories of themes (Cobo et al., 2011). The motor themes emphasised in the upper right quadrant are characterised by the highest levels of centrality and density, indicating that these themes are well-developed and significant for a research field. Higher levels of centrality describe the basic themes revealed in the lower right quadrant but lower levels of density, indicating transversal and general basic themes that are significant for a research field but insufficiently developed (Cobo et al., 2011). The niche themes are noted in the upper-left quadrant, with high density (well-developed internal links) but lower centrality (insignificant external links), designating the high-developed themes but of only marginal significance for the research field. Finally, the themes in the lower left quadrant have low density and centrality, indicating the emerging or declining themes that are weakly developed and of marginal significance for the research field (Cobo et al., 2011). Figure 12 shows the visualisation of thematic map analysis performed through Biblioshiny on R Studio on our data. Based on this analysis, it becomes evident that "sustainable development," "Global Reporting Initiative," and "stakeholder engagement" are the motor themes in this research field, given their well-established internal connections (high density) and substantial external connections with other clusters (high centrality). The themes associated with "corporate social responsibility," "assurance", and "corporate governance" lie on the border between basic and motor themes. This indicates that these themes hold significant importance within the research field (high centrality). Still, internal connections are developed within the research field (medium density with a tendency to increase). The themes associated with "content analysis," "legitimacy theory," "stakeholder theory," "environmental reporting," "audit fees," and "audit quality" are situated in the niche themes quadrant with high density but lower levels of centrality. This suggests that these themes are well-established and developed within the field but hold relatively less significance in the broader research landscape. Lastly, themes like "corporate social responsibility," "sustainability reporting," "sustainability assurance", and "external assurance" are categorised as basic themes. These themes hold substantial relevance within the research field but are still in development, suggesting the need for further attention and research by scholars in the SRA field.

Figure 12. Thematic map analysis

Source: generated using Biblioshiny on R Studio on selected data

4. Content analysis of highly influential studies in the field of SRA

This section follows the approach recommended by other relevant bibliometric studies (Zabavnik and Verbi, 2021). We conduct a content analysis of the most influential studies from the sustainability reporting assurance research field, identified and ranked based on their average annual citations. This section is structured as follows. First, we introduce the fundamental theories that have served as the foundation for these studies. The second subsection delves into the research methodologies employed in these studies. The third subsection summarises the main thematic issues these studies address and highlights their critical contributions to the existing body of knowledge in the research field under investigation. Lastly, the concluding subsection provides relevant avenues for future research within the SRA domain, addressing each primary thematic analysis separately. The list of 50 highly influential studies in the field of SRA can be found in the Appendix.

4.1. Key theories

Analysing the top 50 influential studies in the field of SRA, focusing on the fundamental theories underpinning these studies, we can observe that a broad range of theories is at play, although a few still dominate the foundational basis.

Legitimacy theory is among the most frequently employed theories in the field of SRA, and it features prominently in many of the most influential studies (O’Dwyer et al., 2011; Braam et al., 2016; Kuzey and Uyar, 2017; Odriozola and Baraibar, 2017; Boiral et al., 2019; Deegan, 2019; Li et al., 2023). This theory posits that managers with lower environmental performance are more inclined to actively manage stakeholders' perceptions and the public's trust in the credibility and reliability of their environmental reports to secure organisational legitimacy. External assurance often provides this legitimacy (Braam et al., 2016). In this context, a noteworthy portion of SRA's top 50 influential studies have produced substantial findings that align with legitimacy theory. For instance, Kuzey and Uyar (2017) discovered that companies with reduced sustainability performance must enhance the credibility of their reports. This goal can be achieved through the external assurance of sustainability reports. Similar outcomes were also reached by Braam et al. (2016) and Odriozola and Baraibar (2017), who contended that CSR disclosures and their validation, often through external assurance, serve as a tool to showcase the legitimacy of corporate actions, potentially garnering the support and endorsement of stakeholders. Stakeholder theory is embraced as a more comprehensive perspective that assigns equal importance to all company stakeholders. In this context, CSR information disclosure and independent external assurance are regarded as tools to address better stakeholders' expectations (Kolk and Perego, 2010; Odriozola and Baraibar, 2017; Beske et al., 2020). Agency theory is based on informational imbalances between a company and its various stakeholder groups. Often, this theory has been employed to advocate for the incorporation of sustainability reporting into a company's strategy as a mechanism to mitigate information disparities between managers (agents) and investors (principals) (Clarkson et al., 2019; Simnett et al., 2009; Odriozola and Baraibar, 2017; Reimsbach et al., 2018). Institutional theory has been employed to elucidate the impact of the social environment in which a company operates. It suggests that companies may shape their behaviour concerning CSR practises disclosure and subsequent assurance in response to this social context (Martínez-Ferrero and García-Sánchez, 2017c). Therefore, it is anticipated that institutional factors could significantly influence the pursuit of legitimacy for corporate actions through sustainability assurance. Additionally, the demand for external assurance of sustainability reporting tends to be higher in countries where corporate practices are more closely monitored by market and institutional mechanisms (Simnett et al., 2009; Kolk and Perego, 2010; Perego and Kolk, 2012; Martínez-Ferrero and García-Sánchez, 2017c). Furthermore, neo-institutional theory represents an expanded framework that incorporates elements from earlier theories but goes beyond them by encompassing organisational isomorphism and other previously overlooked cultural values (Martínez-Ferrero and García-Sánchez, 2017c). Hence, companies can attain legitimacy through the disclosure and external assurance of CSR reports, driven by the coercive force of law, moral compliance (normative), or by adopting a mimetic approach, which involves compliance with widely accepted practises within the same sector (Kolk and Perego, 2010; Martínez-Ferrero and García-Sánchez, 2017c; Baalouch et al., 2019).

Other theories identified as foundational among the top 50 influential studies in the SRA field include those related to resources: the resource-based view and resource dependency theory. While the resource-based view primarily focuses on a company's strategies to effectively utilise its internal resources and capabilities in response to external threats and opportunities (Li et al., 2023), resource dependency theory is orientated towards resources obtained from external sources, including the environment. Additionally, within the context of resource dependency theory, the strategies and structures adopted by the board of directors and its committees can be significant resources that can generate value and sustainable advantages. This contributes to building external relationships with critical third parties and gaining easier resource access (Al-Shaer and Zaman, 2018). Finally, the signalling theory is another relevant theory used by the authors of the 50 most influential studies in the SRA domain. According to this theory, firms with a high level of commitment to CSR are expected to be more inclined to seek external assurance for their CSR reports as a mechanism to enhance the credibility of CSR reports and effectively signal their strong commitment to sustainability (Clarkson et al., 2019; Karaman et al., 2021).

4.2. Research methodology

In terms of the research methodology used by the most influential studies, content analysis was the most frequently used research method, encompassing both quantitative and qualitative approaches (e.g. Moroney et al., 2012; Michelon et al., 2015; Stolowy and Paugam, 2018; Boiral et al., 2020; Beske et al., 2020). Therefore, content analysis was applied in 20 of the 50 most influential SRA studies to assess assurance quality in sustainability/CSR reports (Kolk and Perego, 2010). Quantitative content analysis was the predominant approach, often employed to assess various samples of sustainability/CSR reports, establishing a disclosure score/index. Subsequently, these scores were analysed in relation to other variables, depending on the study objectives. Furthermore, content analysis was frequently coupled with various empirical research methods such as sequential logit analysis (Simnett et al., 2009), linear regression (Fernandez-Feijoo et al., 2014), probit model (Muslu et al., 2019), general pooled ordinary least squares (OLS) regression (Braam et al., 2016), logistic regression model (Peters and Romi, 2015), and multiple linear regression analyses (Lock and Seele, 2016; Mohamed Adnan et al., 2018). Qualitative content analysis of sustainability reports was also commonly employed, with a primary focus on comprehending and interpreting the comparability and credibility of the presented information (Perego and Kolk, 2012; Boiral, 2013; Jones et al., 2014; Turker and Altuntas, 2014; Boiral and Henri, 2017; Talbot and Boiral, 2018; Boiral et al., 2019; Boiral and Heras-Saizarbitoria, 2020). It is worth noting that many of the qualitative content analyses were centred around samples of companies from the mining and energy sectors, providing a comprehensive perspective on the primary outcomes of the sustainability assurance process, including its deficiencies (e.g.Talbot and Boiral, 2018; Boiral et al., 2019; Boiral and Heras-Saizarbitoria, 2020).

The second category of methodological approaches involves various regression models employed in statistical analyses. These include sequential logit models, used to examine whether CSR reports were issued, assured, and the type of provider (Casey and Grenier, 2015), as well as logistic or probit regression models when dealing with dichotomous or binary outcome variables (Sierra-García et al., 2015; Liao et al., 2016; Odriozola and Baraibar-Diez, 2017; Al-Shaer and Zaman, 2018; 2019; Clarkson et al., 2019).

Finally, the third significant category of research methods involves experimental studies investigating the effects of sustainability reporting assurance on various aspects. For instance, Reimsbach et al. (2018) conducted an experimental study using a sample of 104 professional analysts as proxies for professional investors. Their research aimed to investigate, among other factors, the impact of sustainability assurance on the assessments made by professional investors regarding corporate performance. Furthermore, Pflugrath et al. (2011) conducted a behavioural experiment involving financial analysts from Australia, the United Kingdom, and the United States. The study aimed to gather insights from these analysts on the credibility of CSR reporting, mainly when it is subject to voluntary assurance, and to examine their perceptions regarding the type of assurance provided.

4.3. Key theoretical and empirical contributions

4.3.1. Legitimacy of Sustainability Reporting and Its Assurance Practices

One of the most frequently discussed thematic analyses in the observed papers pertains to comprehending the sustainability assurance process and strategies for legitimising these relatively new assurance practices (O’Dwyer et al., 2011). As presented in Section 4.1, legitimacy theory was often employed to explain the advantages of external assurance for sustainability reporting. This is particularly evident in the case of companies with lower environmental performance, including those with higher greenhouse gas (GHG) emissions. Companies aim to establish credibility on sustainable practices via reports. (Kolk and Perego, 2010; Pflugrath et al., 2011; Sierra-García et al., 2015; Braam et al., 2016; Kuzey and Uyar, 2017; Reimsbach et al., 2018). Furthermore, this increases their chances of being acknowledged as a company with a more robust corporate image (Odriozola and Baraibar, 2017).

However, a critical perspective questions the effectiveness of external CSR/sustainability reporting assurance in providing a credible guarantee of its quality and transparency. This scepticism arises partly from commercial considerations that can influence this certification process, often referred to as a "rational myth". (Boiral and Henri, 2017; Talbot and Boiral, 2018; Boiral and Heras-Saizarbitoria, 2020). Talbot and Boiral (2018) contended that the external assurance process is ineffective in this context. They based this argument on their analysis of 93 CSR reports audited by a third party, revealing a significant level of non-compliance with the referenced framework (GRI guidelines) in more than 92% of the analysed reports. Hence, a noteworthy portion of the CSR reports verified by external assurors still exhibit incomplete, non-compliant, or missing elements, particularly regarding climate performance (Talbot and Boiral, 2018). Similar findings were also corroborated by Boiral and Heras-Saizarbitoria (2020), who, through a qualitative content analysis of 337 assured sustainability reports issued by companies in the mining and energy sectors, highlighted that assurance statements often appear to be a disconnected practice that doesn't align well with the specific requirements of sustainability reporting. As it's not uncommon for sustainability reporting and the auditing process to be heavily influenced by managers, Boiral et al. (2019) recommended that assurance providers should increasingly rely on information not controlled by reporting companies. This might involve conducting interviews with various stakeholders, investigating complaints, and reviewing reports and analyses from governmental agencies. Additionally, Boiral and Heras-Saizarbitoria (2020) found that most assurance statements in the mining and energy industry did not offer a high level of assurance. The assurance reports often did not explain the reason for the lower level of assurance. This may be a way for the assuror to limit their liability. Still, it also suggests that the evidence available for scrutinising sustainability reports was often insufficient for a thorough investigation and higher levels of assurance (Boiral and Heras-Saizarbitoria, 2020).

4.3.2. Corporate governance

A theme extensively discussed in the 50 most influential studies in the field of SRA refers to how corporate governance mechanisms influence corporate decision-making concerning the adoption of voluntary assurance and the selection of assurance providers (whether accounting professionals or sustainability specialists). Examining the relationship between specific characteristics of the board and the disclosure and assurance of CSR frequently emphasised their significant influence. For instance, in their analysis of the correlation between board characteristics and CSR assurance decisions for a sample of 2054 firm-years among Chinese listed companies, Liao et al. (2016) found that larger board sizes, the presence of female directors, and the separation of CEO and chairman positions are more likely to result in the hiring of CSR external assurance. Gender diversity and board independence were found quite frequently to have a significant and positive association with the decision to adopt voluntary CSR/sustainability assurance in many studies among those observed (Al-Shaer and Zaman, 2016; Liao et al., 2016; Baalouch et al., 2019; Rosati and Faria, 2019; Arayssi et al., 2020). Although most studies unanimously conclude about the positive influence of gender diversity and board independence on the external assurance process, the existing literature does not adequately address the possibility of a critical threshold in the number of women on corporate boards that could lead to negative impacts on sustainability reporting and its assurance. Furthermore, the factors that could determine or moderate this critical threshold remain unexplored.