Bibliometric study of the link between Sustainability and Circular Economy: A contribution for current business model from the collaboration Enterprise-University

ABSTRACT

A business model (BM) is a new unit of analysis distinct from the product or the company, with broader boundaries than the traditional way to regard a company. More exactly, it can be defined as a systemic and integrated view to create and deliver value to its customers. However, issues related to social and environmental aspects have been neglected by the BM approach. Most of the traditional business models (BMs) have only one goal, which is to create financially profitable companies. This “narrowness of mind” has been tackled by several authors due to the rising of Corporate Social Responsibility (CSR) strategies, which have been amplified, due to the rising of the Circular Economy (CE) paradigm. CSR actions are part of predominantly linear BMs, in which the overall achievement of the organization has been measured following the grade of implementation of said measures. The literature demonstrates that the CSR actions applied have been effective. However, we must question whether this is enough, and that leads us to three questions linking CSR and sustainability with BMs under a triple theoretical framework. Owing to the need to study the change of model, the goal of this paper is to perform a bibliometric analysis of the existing literature about CSR, sustainability, and CE simultaneously which can help us to put the need for and importance of this line of research into context. This paper is also a contribution for the new BMs that stem from the collaboration between enterprises and Universities.

Keywords: Sustainability; Circular economy; Bibliometric analysis; Business models.

JEL classification: M14; M41.

Estudio bibliométrico del vínculo entre Sostenibilidad y Economía Circular: Una aportación para el modelo de negocio actual desde la colaboración Empresa-Universidad

RESUMEN

Un modelo de negocio (MN) es una nueva unidad de análisis diferente del producto o la empresa, con límites más amplios que el punto de vista tradicional de la empresa. Más concretamente, puede ser definido como una visión integrada y sistémica para crear valor para los clientes. Sin embargo, los problemas sociales y ambientales han sido descuidados por los MN. Gran parte de los MN tradicionales solamente tienen un objetivo, crear empresas financieramente rentables. Esta “estrechez de miras” ha sido analizada por varios autores debido al surgimiento de estrategias de Responsabilidad Social Corporativa (RSC), bajo un punto de vista sostenible que ha ido más allá con la creación del paradigma de la Economía Circular (EC). Las prácticas de RSC forman parte de MN predominantemente lineales, en los que el grado de éxito de la empresa se mide según el éxito de implementación de dichas prácticas. La literatura demuestra que las acciones de RSC aplicadas han sido efectivas; sin embargo, debemos preguntarnos si es suficiente, lo que nos lleva a hacernos tres preguntas que vinculan la RSC y la sostenibilidad con los MN bajo un triple marco teórico. Debido a la necesidad de estudiar el cambio de modelo, el objetivo de este trabajo es llevar a cabo un análisis bibliométrico de la literatura existente sobre RSC, sostenibilidad y la EC simultáneamente, lo que ayuda a contextualizar la necesidad y la importancia de esta línea de investigación. Este trabajo también contribuye a la literatura de los nuevos MN surgidos de la colaboración entre empresas y la Universidad.

Palabras clave: Sostenibilidad; Economía circular; Modelos de negocio; Estudio bibliométrico.

Códigos JEL: M14; M41.

1. Introduction

When mass production and consumption started, the industries transformed the manufacturing processes in a mechanism that accelerated the global use of materials and resources via the application of linear business models (BMs), which are considered a waste of resources today (Steffen et al., 2015; Marco-Fondevila et al., 2021; Llena-Macarulla et al., 2023). Recently there has been a need of creating an alternative economic model, known as Circular Economy (CE), to face the environmental problems caused by the linear models and separate the consumption of resources from economic activity (European Commission, 2020; Schaltegger et al., 2023; Marco-Fondevila et al., 2021; Llena-Macarulla et al., 2023) and based on resources cycling. By adopting circular models, companies can preserve an important part of the economic value added to products during manufacturing, as well as reduce the environmental damage associated with said products (Korhonen et al., 2018; Marco-Fondevila et al., 2021; Scarpellini, 2022; Llena-Macarulla et al., 2023). Companies may be willing to invest in additional manufacturing or designing costs to create more lasting products which reduce future costs, for example maintenance costs, although there is a risk of not recovering the investment if the products are prematurely obsolete (Nyström et al., 2021).

One of the main research areas of CE nowadays is the transition from linear models (obtaining raw materials, manufacturing of products, consumption, and waste) to circular models, an essential solution to avoid the increasing use of finite resources and the increasing amount of waste (Marco-Fondevila et al., 2021; Sopelana et al., 2021; Schaltegger et al., 2023; Llena-Macarulla et al., 2023). Many sustainability researchers have affirmed that CE has emerged because of the needs of the current BMs, with companies going further than positioning sustainability in the centre of their business strategies (Rauter et al., 2017; Witjes & Lozano, 2016; Scarpellini, 2022; Llena-Macarulla et al., 2023). Moreover, several theoretical frameworks have been created and are at the disposal of organizations to help them establish effective and sustainable circular models (Sopelana et al., 2021). Literature proposes diverse frameworks and methodologies to measure the performance linked with CE (Garza-Reyes et al., 2019; Llena-Macarulla et al., 2023), and the analyses differ in terms of the researched context, such as sectors (Rossi et al., 2020), geographical regions (Sánchez-Ortiz et al., 2020; Yadav et al., 2020) or application levels (Moraga et al., 2021; Moraga et al., 2019).

The concept of CE emerged in the 90s, as a link between environmental preservation and economic performance (Merli et al., 2018), although it has been only recently when CE has gotten significant (Kirchherr et al., 2017; Llena-Macarulla et al., 2023), because the manufacturing sector has understood the need of reducing the use of resources, of minimizing waste and of decreasing its environmental impact (Dey et al., 2020; Marco-Fondevila et al., 2021; Scarpellini, 2022; Schaltegger et al., 2023). The CE can be applied in three levels: micro (products, companies and consumers), meso (integrated economic agents) and macro (cities, regions and governments), and it implies the inclusion of waste hierarchy (prevention, reduction, reuse, recycling, recovery and elimination) (Geissdoerfer et al., 2017; Scarpellini, 2022; Negri et al., 2021). The CE is strongly linked with sustainability, and having a correct understanding of the relationship between both is necessary to have a complete idea of CE as a concept regarding the new business models (NBMs) (Mura et al., 2020; Fehrer & Wieland, 2021; Scarpellini, 2022; Schaltegger et al., 2023; Llena-Macarulla et al., 2023).

Although BMs lack theoretical grounding in economics or business studies (Teece, 2010), the topic has increasingly been tackled by several scholars (Scarpellini, 2022). The traditional view of BMs defines them as a logical structure that connects some technical potentiality with a viable economic value perspective (Chesbrough & Rosenbloom, 2002). Nevertheless, according to Zott et al. (2011), the literature on BMs has brought to the fore several relevant topics such as the recognition that a BM is a new unit of analysis distinct from the product or the company itself, with broader boundaries than the traditional way to look at a company. Recent discussions outline a BM as a systemic and integrated view to create and deliver value to its customers (Teece, 2010; Osterwalder & Pigneur, 2011). The so-called Business Model Canvas (BMC), created by Osterwalder & Pigneur (2011) is the better known example of that view.

However, issues related to social and environmental aspects have been neglected in most of the BMs approach (Stubbs & Cocklin, 2008; Llena-Macarulla et al., 2023). According to Upward (2013), most of the traditional BMs have only one goal: to create financially profitable companies. This “narrow-mindedness” has been tackled by several authors more recently (Stubbs & Cocklin, 2008; Upward, 2013; Boons & Ludeke-Freud, 2013; Bocken et al., 2014). We cannot say that this way of operating has not been adequate and beneficial for businesses. In fact, a significant amount of research has shown how companies that are carrying out CSR actions are achieving better results, better performance, higher productivity, more competitiveness, better reputation and image, while having a more motivated and satisfied human capital. All of the above indicates that the CSR applied has been effective. However, we have to question whether this is enough, leading to these research questions:

RQ1: Are CSR, sustainability, and CE current lines of research capable of contributing to current business models that stem the company-University collaboration?

RQ2: Can the current business models be supported by company-University collaboration to give effect to their circular strategies?

RQ3: Can the perspective of circular business models satisfy the demands of companies and stakeholders and legitimize them?

Within this perspective, we are oriented towards a circular BM, which implies reducing the dependence on raw materials, the transition to renewable sources of energy and the adoption of sustainable processes in the companies' value chain (Zamfir et al., 2017; Scarpellini, 2022; Llena-Macarulla et al., 2023). The management of circular BMs will cause changes in the accounting systems, specially in non-financial information (Scarpellini et al., 2020; Barnabè & Nazir, 2021), and it will also motivate changes in the accounting management and control (Scarpellini, 2022; Llena-Macarulla et al., 2023). Universities can contribute to all these research lines, giving knowledge and developing projects from research groups.

The expansion of this field of research is caused by the increase of available literature and by the apparition of diverse schools of thought, like performance economics, clean production, industrial ecology, or sustainability (Sopelana et al., 2021), which is the topic analyzed in this paper, which objective is to perform a bibliometric study of the existing literature about both CSR, sustainability and EC simultaneously which can help us to put the need and importance of this line of research into context and constituting a contribution to new BMs (NBMs) that stem from the collaboration between organizations and universities.

Results show that obtaining objective data about the research undertaken during the analyzed period is one of the reasons to use bibliometric methods, giving them more value than to subjective ideas (Corsini et al., 2019). To achieve the paper's goal, a sample of 1132 papers from the Scopus database has been selected, which have been published between 2013 and 2022 and that study the topics of CSR, sustainability and CE or a combination of the three topics. This will help us evaluate the scientific production, contributing to improve the existing literature about sustainability and CE (Alvarez-Etxeberria et al., 2023; Correa, 2011; Leal et al., 2019; Blanco-Zaitegi et al., 2022), with an application oriented to new BMs that stem from the collaboration between enterprises and universities, and it also opens the path to the orientation, both of companies and of CSR research, to perform their management under the prism of CE. Moreover, the paper makes the results available to different stakeholders such as researchers, politicians, and others (Ellegaard & Wallin, 2015). At the same time, it wants to be part of the paths towards the publication of sustainability report in a context of circular BMs, joining previous research such as that done by Scarpellini (2022). Finally, it will allow the new BMs to offer new research areas and demand niches that can be covered, as well as institutions that can provide support and promote research.

This paper is structured in six sections. After this introduction, we present the concepts of sustainability, CSR and CE and the theoretical framework. In the next section, we present the methodology we have applied, and then the results of our study, divided in three clusters. Later, we posit the discussion, and in the final section we present the conclusions, limitations and future lines of research.

2. Sustainability, corporate social responsibility and circular economy

The concept of sustainable development emerged in the seventies, when the planet was facing problems such as the fast increase of the population or the depletion of natural resources (Hoang et al., 2021). According to Our Common Future report (World Commission on Environment and Development, 1987), authored by the so-called "Brundtland Commission", sustainable development can be defined as "the ability to fulfil the needs of the present generations without compromising the ability of future generations to fulfil theirs" (Brundtland, 1987, p. 16). More recently, the 2030 Agenda approved by the UN in 2015, highlighted the need for businesses to be oriented towards sustainability, noting that this implies “eradicating poverty in all its forms and dimensions, fighting against inequality in and within countries, preserving the planet, creating sustained, inclusive and sustainable growth and fomenting social inclusion” (UN, 2015, p. 8).

The relevance of sustainability motivates its fundamental character in business management research due to its link with the possibility of obtaining an increased competitive advantage (Hoang et al., 2021). Recently a lot of advancements have been made, mainly the change of the definitions of sustainability and competitive advantage based in a better economic performance for another meaning that acknowledges the importance of the link with economic, social, and environmental impacts (Greco et al., 2015). This change covers the dimensions which define the Triple Bottom Line model, defined as economic prosperity, environmental quality and social justice (Elkington, 2004; Colbert & Kurucz, 2007; Shum & Yam, 2011; Henry et al., 2019; Kravchenko et al., 2019), increasing the value of the product.

CSR has also attracted the attention of researchers in recent decades, and it has been considered a mechanism by which organizations can assume their commitment to sustainability (Gallardo-Vázquez & Sánchez-Hernández, 2014a, 2014b; Valdez-Juárez et al., 2018; Blanc et al., 2019; Daddi et al., 2019; Galant & Cadez, 2017; Buhr et al., 2023). According to some researchers, nowadays CSR consists in maintaining high standards and giving back a product to communities (Wong & Kim, 2020). The concept is of a special importance to the European Union (EU), and the European Commission defines CSR as the voluntary responsibility of organizations of their impacts on society (European Commission, 2001). According to The Green Book: Promoting a European framework for Corporate Social Responsibility (European Commission, 2001, p. 4), companies decide to voluntarily contribute to achieving a better society and a cleaner environment by integrating social and environmental aspects in their commercial operations and the interactions with their stakeholders (COM 2001, p. 6). Later, this definition was renewed by the EU Commission (2011) itself, pointing out the responsibility of companies for their impact on society and making explicit reference to the need for collaboration with stakeholders to integrate social, environmental and ethical concerns, respect for human rights and consumer concerns within their strategy and business activities (European Commission, 2011). Linked with the development and publication of sustainability reports, it is worth highlighting the work undertook by international initiatives such as the Global Reporting Initiative (GRI) and the International Integrated Reporting (IIR) Framework, which have contributed to the creation of standards for the divulgation of non-financial information (Blanco-Zaitegi et al., 2022).

Generally, commitment to CSR implies that organizations must work in a way that promotes the links between society and the environment, as well as contribute to sustainable development in a positive way (Khaskheli et al., 2020). Organizations can not only strengthen their brands, but also benefit society in other ways, such as creating new jobs, promoting education and economic growth, and creating a positive public image that facilitates their social acceptance (Galant & Cadez, 2017; Macassa et al., 2017). CSR focuses in creating a new social conscience in business that is compatible with maximising profits, even if said maximisation occurs indirectly (Moon & Parc, 2019; Nave & Ferreira, 2019); but it is not easy, because CSR does not increase profits directly but indirectly by increasing respect for the company and its products in the market, which can cause an increase of sales, greater customer loyalty and better talent attraction, which can also cause share prices to increase and shareholders to earn more (Strielkowski et al., 2021). Despite the numerous references to CSR, these actions are proposals to be included in a predominantly linear BM, in which the overall achievement of the organization has been measured from the implementation of these actions. However, the linear model based in the assumptions of abundance, availability, ease of obtaining and cheap disposal of resources is no longer possible. This poses a threat to the competitiveness of Europe and other regions, and a more global and sustainable model is needed (EC, 2014).

CE is receiving an ever-increasing level of attention, with the goal of integrating economic activity and environmental wellbeing in a sustainable way (Yang et al., 2019; Scarpellini, 2022; Marco-Fondevila et al., 2021; Llena-Macarulla et al., 2023). The focus of CE is maintaining resources in the economy during a longer period of time, generating economic growth and minimizing the consumption of finite natural resources (Ishii, 2018; Llena-Macarulla et al., 2023). The CE represents a paradigm change in the way that human society interacts with nature, and it has the goal of avoiding the depletion of resources, closing the circuits of energy and materials and substituting the concept of end of life with the concepts of reducing, reusing, recycling and recovering materials in manufacturing, distribution and consumption processes (Scarpellini, 2022; Scarpellini et al., 2020; Scarpellini et al., 2019; Marco-Fondevila et al., 2021; Llena-Macarulla et al., 2023). CE refers to the reuse of subproducts, to the use of shared infrastructures and to the use of shared services, to achieve a better exploitation of resources, which can be beneficial not only in the economic sense but also in the environmental sense. Obviously, CE is linked with good management and production practices in organizations, and in human resource management.

We conclude this section reasoning the relationship between sustainability and CE, as well as their similarities and differences (Geissdoerfer et al., 2017; Marco-Fondevila et al., 2021). Some authors are oriented to studying whether the CE model addresses a different concept of environmental sustainability (Marco-Fondevila et al., 2021; Stewart & Niero, 2018). Literature indicates that these concepts are not substitutes or equivalents (Geissdoerfer et al., 2017: Stewart & Niero, 2018), while considering them complementary (Sauvé, Bernard, & Sloan, 2016). Given this, actions that integrate the CE economic model will help achieve business sustainability (Marco-Fondevila et al., 2021). But, obviously, the CE model must be integrated into the corporate strategy, so it is considered necessary to work towards a holistic vision of sustainability, encompassing the three classic dimensions, and observing how the CE is beneficial for each of them (European Commission, 2015).

3. Theoretical background

3.1. Stakeholder theory

The stakeholder theory has been traditionally used in accounting research (Larrinaga, 2017; Alvarez-Etxeberria et al., 2023; Buhr et al., 2023). The set of relationships in NBMs is formalized in contracts defining rights, objectives, expectations, and responsibilities and thereby configuring organizations' strategies (Alvarez-Etxeberria & Garayar, 2007; Fassin et al., 2016; Kravchenko et al., 2019; Gallardo-Vázquez & Valdez-Juárez, 2022). In this structure, the importance of stakeholders, as well as their identification and the dialogue with each of them, is a key element (Scarpellini, 2022; Stewart & Niero, 2018). The work they develop in BMs is fundamental, and their contribution will help towards the transition from a linear economy to CE (Rossi et al., 2020; Kirschherr & Piscicelli, 2019). As for the social and corporative governance dimensions, the positive and well defined relationships with employees, customers, suppliers and the community as a whole will determine the success of the strategic communication of the new circular BMs (Iacovidou et al., 2017; Daddi et al., 2019). This will reflect the organizational commitment that has been generated (Turker, 2008), which will also determine the value creation (Ahlers et al., 2020).

As NBMs integrate the CE in their design, they must consider the pressure of the different stakeholder groups and should develop a discourse that motivates them and allows for the integration of their points of view in the management of the company and the obtention of profit (Martínez-Martínez et al., 2017; Pomponi & Moncaster, 2016; Richter & Dow, 2017; Rattalino, 2017; Vaitoonkiat & Charoensukmongkol, 2020).

3.2. Theory of dynamic capabilities

Based on the Resource-Based Theory, the theory of dynamic capabilities focuses on a new scenario where organizations must accept a higher level of responsibility (de los Ríos, Ruiz, Tirado, & Carbonero, 2012). With the necessities detected in the markets as a starting point, the NBMs must incorporate the CE when detecting new opportunities that can give sustainable results (Kachouie et al., 2018; Teece, 2018; Gallardo-Vázquez & Valdez-Juárez, 2022). These resources, or dynamic capabilities, materialize in strategic opportunities which can increase growth and competitiveness for circular BMs (Ledesma-Chaves et al., 2020).

The abilities needed to develop the knowledge that allows the resource extraction, processing, manufacturing, marketing, sale, use, recycling, disposal, identification of social concerns, management of values, and a transparent accountability are dynamic capabilities which facilitates the execution of strategic plans (Sarkar et al., 2016; Gallardo-Vázquez & Valdez-Juárez, 2022). These capabilities are essential activities in CE processes able to improve the social problems detected and the environmental ones (Dentoni et al., 2016; Zbuchea & Pînzaru, 2017). At the same time, these activities generate more accountability reports reflecting the stakeholders´ influence (Ramachandran, 2011; Marco-Fondevila et al., 2021). Globally, these dynamic capabilities exercised by the organizations are an indicative of the commitment both with sustainability and CE, and they have caused an increase of the sustainability reports published, increasing and bettering divulgation (Orazalin & Mahmood, 2018; Schaltegger et al., 2017). In short, the adoption of a CE model represents a paradigm shift that requires the support of the theory under study, as numerous and specific skills and capacities are necessary (De los Ríos & Charnley, 2017; Marco-Fondevila et al., 2021).

3.3. Legitimacy theory

This theory has also been extensively used in accounting research (Larrinaga, 2017; Alvarez-Etxeberria et al., 2023). The acquisition of legitimacy by organizations is a benefit derived from the application of CSR actions (Campbell, 2007). Together with sustainability, CE will also allow the companies to have a better position in the market, since they incorporate activities subject to international trade regulations, global market forces, and improve the companies' internal governance (Scherer & Palazzo, 2011; Odriozola & Baraibar‐Diez, 2017). Legitimacy is a key element for innovative organizations positioned in extremely competitive globalized markets, so implementing CE actions has a key strategic importance in circular BMs (Carroll & Shabana, 2010; Du & Vieira, 2012). The automatic adoption of CE social actions, considered a need in the organizations for the daily work, determines a cognitive legitimacy. At the same time, the companies that have adopted CE are convinced of the possibility of having certain benefits, which determines a pragmatic legitimacy (Scherer et al., 2013). Goergen et al. (2016) affirm that sustainability and competitiveness are necessary criteria for legitimacy, an idea extensible to CE and the competitive advantage it generates.

In terms of the divulgation of information about sustainability and accountability, the adoption of CSR and CE in the NBMs has an influence, because it represents communication tools that legitimate the operativity of the business in its market (Anwar et al., 2019; Daddi et al., 2019; Hahn & Kühnen, 2013; Stewart & Niero, 2018).

In the next section the methodology used for the bibliometric analysis is explained and, later, we will give an answer to the research questions.

4. Methodology

4.1. Selection of sources and search criteria

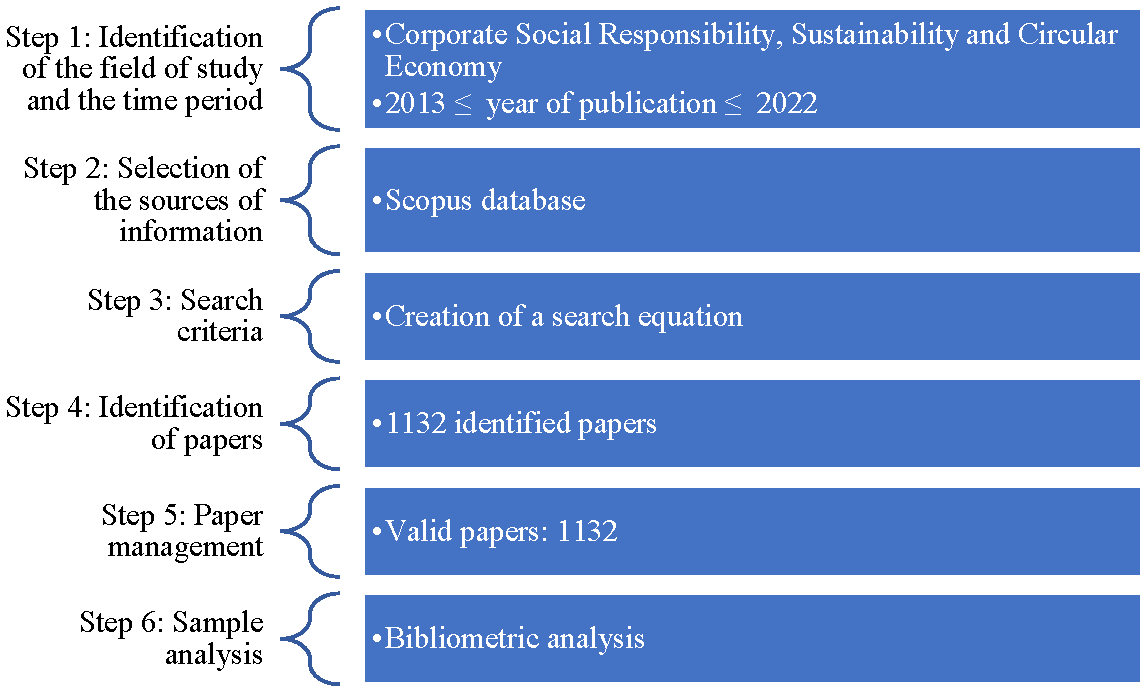

The database from which the papers for the analysis are extracted is Scopus, for various reasons: a) the application of rigorous quality standards like the Scimago Journal Rank (SJR; Hernández-González et al., 2016), b) the greater temporal coverage of Scopus, which makes this database more adequate since it has approximately 20% more results than its main competitor, Web of Science (Falagas et al., 2008) and c) the possibility of downloading simultaneously a high number of detailed references as metadata (Fernández et al., 1999). These reasons validate the indexed information and justify the selection of Scopus (Harzing & Alakangas, 2016). Once the database was selected, a paper search was performed in May 2023, following the search equation shown in Table 1. To filter the results, we selected open access papers, published between 2013 and 2022, and which contained one or several of the following keywords: CSR, sustainability, or circular economy. To be part of the sample, a paper must present either one of the three keywords or any combination of them. The asterisk is used so that Scopus presents results containing not only circular economy but also circular economics. The selected papers are all written in English. With all these criteria, the sample is formed by 1132 papers. Figure 1 shows the steps of the analytic process.

Table 1. Paper search strategy

| Keywords | Corporate Social Responsibility AND Sustainability AND Circular Econom* |

| Category | ALL |

| Knowledge area | Social Sciences |

| Type of document | Open Access papers |

| Time period | 2013 ≤ year of publication ≤ 2022 |

| Language | English |

| Search equation | (ALL("corporate social responsibility") AND ALL("sustainability") AND ALL("circular econom*")) AND PUBYEAR > 2012 AND PUBYEAR < 2023 AND (LIMIT-TO(SRCTYPE, "j")) AND (LIMIT-TO(OA, "all")) AND (LIMIT-TO(DOCTYPE, "ar")) AND (LIMIT-TO(LANGUAGE, "English")) AND (LIMIT-TO(EXACTKEYWORD, "Sustainability") OR LIMIT-TO(EXACTKEYWORD, "Sustainable Development") OR LIMIT-TO(EXACTKEYWORD, "Circular Economy") OR LIMIT-TO(EXACTKEYWORD, "Corporate SocialResponsibility")) |

| Date of search | May 2023 |

Source: Own elaboration.

Figure 1. Steps of the analytic process

Source: Own elaboration.

The literature review process presented in Figure 1 is a key tool in management research, used to manage the diversity of knowledge for a specific enquiry. The aim of this is usually to map and assess the existing intellectual landscape, and to specify a research question (three in the case of this study) to further develop the existing body of knowledge (Tranfield et al., 2003). The bibliometric analysis we have performed studies several aspects of the sample. The number of papers published in each year of the selected period shows whether the topic being studied is current and of interest to researchers. Citations are also analyzed, and they are used as a measure of influence, because if a paper is heavily cited, it is considered important. This assumption rests on the proposition that authors cite papers that they deem important for their work (Zupic, 2015). Although citation analysis lacks the ability to identify networks of connections amongst scholars (Usdiken & Pasadeos, 1995), we have used a distance-based mapping tool that, as we explain in the next subsection, allows for the mapping of the relationship between the different elements of the sample. We have also performed a performance analysis of the different institutions, financing institutions and countries. By doing this, we evaluate the research and publication performance of said elements (Zupic, 2015). Our study ends with a co-word key word analysis, where we constructed a semantic map of the most used key words in the sample (Zupic, 2015). As described by Zupic (2015), analysing key words poses a problem called indexer effect, where the validity of the map is dependent on whether the indexed key words capture all relevant aspects of the text. We solved this problem by not only analysing the indexed key words, but also the key words selected by the authors themselves.

This type of analysis is proving to be very useful in social areas. Some studies are aimed at sustainability, social and environmental information (Alvarez-Etxeberria et al., 2023; Larrinaga et al., 2019; Blanco-Zaitegi et al., 2022) and others at social and environmental accounting as a process of social creation (Correa, 2011). Through them, an examination of scientific production is carried out and academic knowledge is generated, equally useful for business areas.

4.2. Analytic software used

The analytic software used for the bibliometric analysis is VosViewer1. The program creates maps based on distance, which are bibliographic maps on which the distance between two components reflects the strength of the link between them, so the smaller the distance, the stronger the link between components. The elements are distributed very unequally, and that facilitates the identification of clusters of related components, although it makes it more difficult naming all the components without them superposing one another (van Eck & Waltman, 2010). The graphs represent a network of elements through circles (and frames), whose size varies according to the importance of the element, while the network connections represent the closeness of the link between elements. The spatial position of the circles and different colours are used to cluster the items (Pizzi et al., 2020).

The advantages of using bibliometric analyses and visual tools are the following (Ye et al., 2020): 1) the results are based on a quantitative statistical analysis and on a reliable database formed by a high quantity of papers evaluated by pairs which cover a big part of both disciplines and regions of the world (Zemigala, 2019), 2) the visualization can help classify the reach and structure of the disciplines and discover which are the most influent papers or authors, as well as the main clusters of current research (Ye et al., 2020) and 3) the quantitative models are better adapted to areas with a high number of publications than qualitative models, specially to study the internal relationship that exists between the literature (Zhao et al., 2018).

The next section presents the results of the analysis.

5. Results

The results will be analysed classified in three clusters, with which we gave an answer to the research question proposed earlier and with which we present the contribution of the analysis to the NBMs that stemmed from the collaboration between companies and universities.

Cluster 1: Current topics and relevance of the lines of research

In the first cluster we give an answer to RQ1, Are CSR, sustainability, and CE current lines of research capable of contributing to current business models?

With this study we support the promotion of socially responsible, environmentally sustainable and economically viable in the long-term practices, present in the topics of the search performed, focused on sustainability and the CE (Hoang et al., 2021; Barnabè & Nazir, 2021). These strategies can foster innovation while improving efficiency and organizational performance (Boons & Ludeke-Freud, 2013; Clark, 2021; Ghosh & Van de Vrande, 2020; Rattalino, 2017; Schaltegger & Wagner, 2011). They will also allow companies to rethink their BMs, adopting circular and sustainable approaches without being dependent on resources (Schaltegger & Wagner, 2011; Scarpellini et al., 2019; Scarpellini et al., 2020). Sustainable and circular practices will decrease environmental impacts and in distribution, as well as improving the relationship with stakeholders (Pomponi & Moncaster, 2016; Scarpellini, 2022; Stewart & Niero, 2018).

The topics of sustainability and CE affect current BMs from different approaches of companies' lives which are also studied in academic research: i) Efficiency in the use of resources (energy, water, and raw materials): BMs focus on the minimization of resouce consumption, the optimization of manufacturing processes, the reduction of waste, reutilization and recuperation of materiales, recycling, etc. (Scarpellini, 2022; Scarpellini et al., 2020; Scarpellini et al., 2019) ; ii) Implementation of CE: BMs with the focus explained in i) above can transform waste of a specific part of the manufacturing process in raw materials for another (Esfahbodi et al., 2016; iii) Sustainable management of the supply chain: both points above have caused the implementation of socially responsible practices by suppliers, because of the sharing of responsible values, (Zamfir et al., 2017; Scarpellini, 2022); and iv) Innovation: making steps towards sustainability implies the need of undertaking innovations with a smaller impact, and this should be considered by NBMs (Clark, 2021; Ghosh & Van de Vrande, 2020; Hoang et al., 2021; Seppänen et al., 2019).

The results of the study supports the reasoning made above, the most frequent topic being the environmental science, with 787 papers and 13381 citations, followed by social sciences with 598 papers and 8259 citations and by energy, with 583 papers and 8863 citations (Table 2). The sample has no common topic. The search performed can help satisfy all the needs of NBMs, focused on the environment, social sciences and energy. Those three topics are the most frequent, a fact that can help decide the projects that should be developed in the collaborations between universities and enterprises.

Table 2. Main topics of the sample

| Topic | Frequency | Citations | Average citations | h index |

|---|---|---|---|---|

| Environmental Science | 787 | 13381 | 17 | 62 |

| Social Sciences | 598 | 8259 | 13.81 | 46 |

| Energy | 583 | 8863 | 15.20 | 51 |

| Engineering | 472 | 7862 | 16.66 | 52 |

| Business, Management and Accounting | 365 | 10316 | 28.26 | 59 |

| Computer Science | 273 | 2172 | 7.96 | 28 |

| Economics, Econometrics and Finance | 104 | 4582 | 44.06 | 32 |

| Decision Sciences | 69 | 1901 | 27.55 | 22 |

| Mathematics | 40 | 344 | 8.6 | 12 |

| Medicine | 32 | 186 | 5.81 | 9 |

| Agricultural and Biological Sciences | 26 | 199 | 7.65 | 11 |

| Materials Science | 23 | 116 | 5.04 | 7 |

| Psychology | 23 | 359 | 15.61 | 11 |

| Chemical En<gineering | 17 | 236 | 13.88 | 9 |

| Arts and Humanities | 12 | 1052 | 87.7 | 7 |

| Earth and Planetary Sciences | 9 | 111 | 12.3 | 7 |

| Physics and Astronomy | 8 | 74 | 9.25 | 4 |

| Chemistry | 6 | 58 | 9.7 | 4 |

| Multidisciplinary | 5 | 7 | 1.4 | 2 |

| Pharmacology, Toxicology and Pharmaceutics | 2 | 4 | 2 | 26 |

| Biochemistry, Genetics and Molecular Biology | 1 | 6 | 6 | 1 |

Average citations: Total citations / Papers that analyse the topic.

Source: Own elaboration.

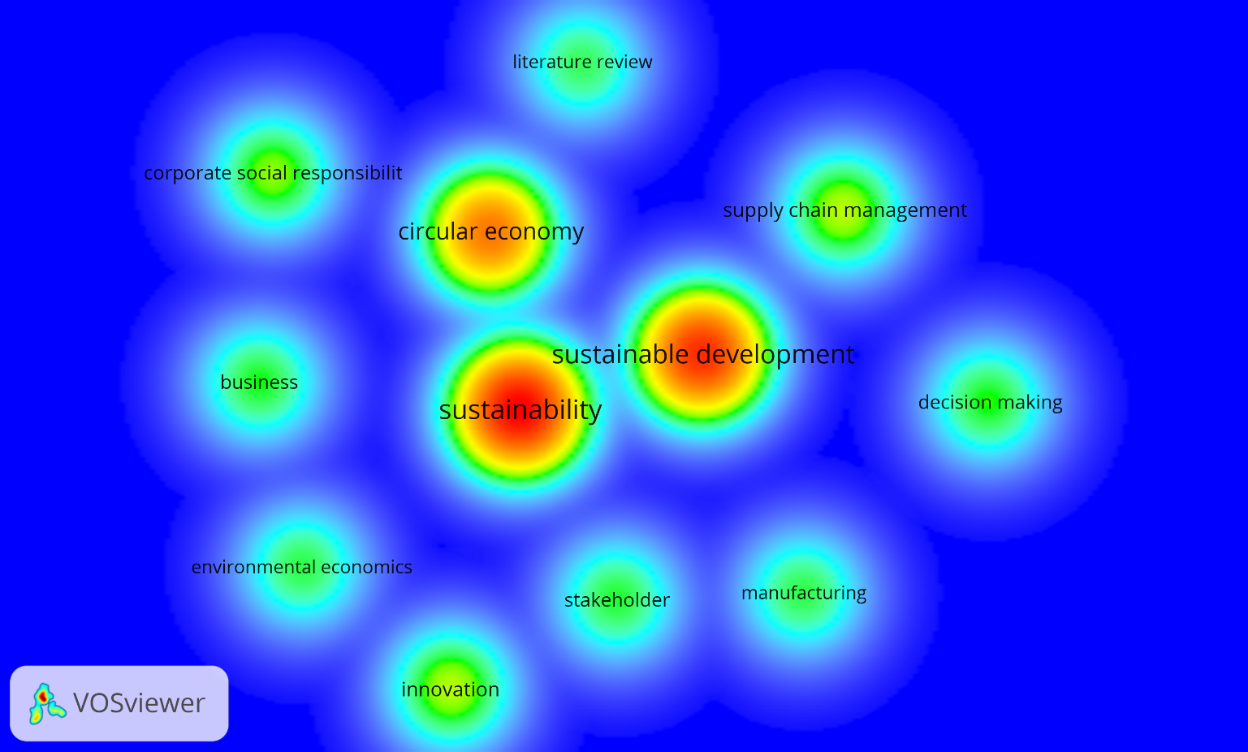

The analysis of the keywords of the sample highlights the importance of the search equation and justifies its analysis by BMs, with the figure of the stakeholders also being present, a part of the theoretical framework of the study. Figure 2 shows the 12 keywords that are cited a minimum of 64 times. The most repeated, those represented with the warmest colours, are sustainability, sustainable development and circular economy, with the fourth being corporate social responsibility, the four keywords that were defined in the search equation shown in Table 1.

Figure 2. Top 12 keywords of the analyzed sample

Source: Own elaboration.

Analyzing the citations is relevant and can affect current BMs. Because of the increasingly frequent collaboration between companies and universities, NBMs can use the support of researchers to guide them in the development of certain research projects. In this search of the most adequate research team for each new BM the organization will evaluate a certain group of aspects, such as i) the identification of lines of research and work areas in the universities and research centres, which can benefit from knowing how many citations each paper has, deducing from them the importance of the researcher or researchers, as well as how current the line of research is. NBMs develop multidisciplinary and transversal strategies formed by different knowledge fields, so it is needed to develop the link that allows the optimal development of new opportunities for business (Clark, 2021; Etzkowitz & Klofsten, 2021); ii) The quality of the research: this aspect is measured by citations, which also determines the impact of the research and its relevance. A NBM should be supported by high quality authors, sufficiently cited, which will be a warranty for the proper development of the business idea (Guerrero et al., 2020; Meoli et al., 2020) and iii) Position of the competence: the number of citations is public and easy to observe, so each author can know the researching activity of the competence. This comparison will allow NBMs to know how strong a piece of research is and value the convenience of its development.

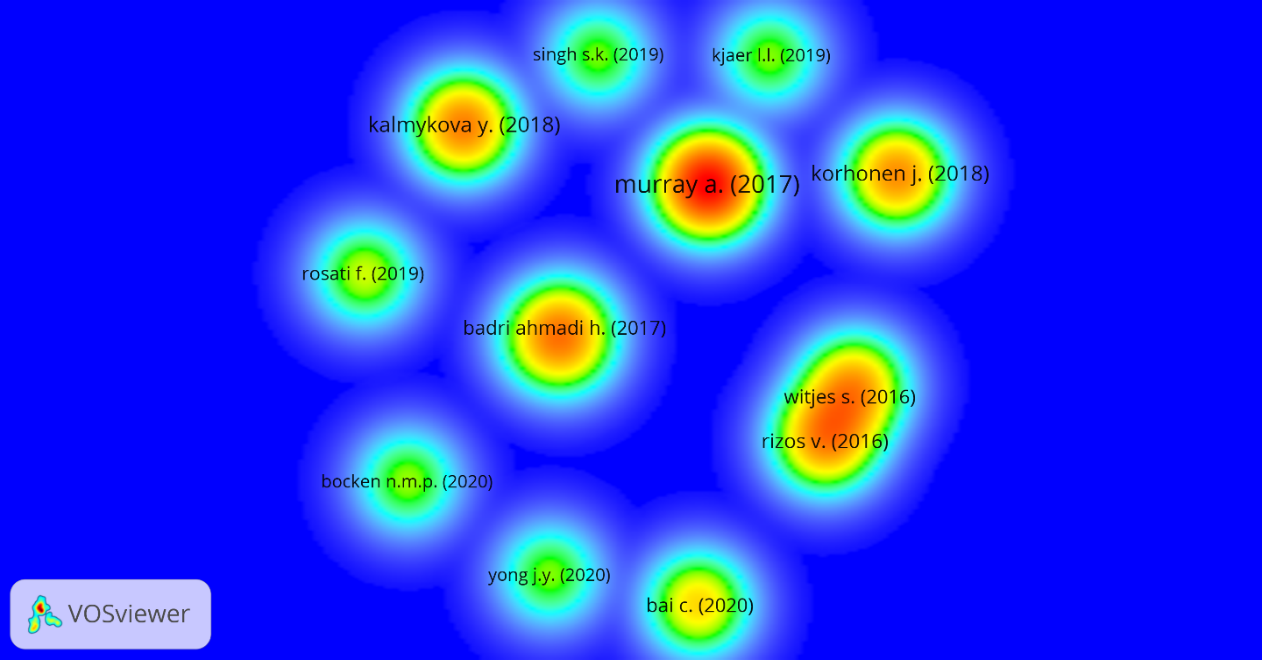

The most cited paper, as shown in Table 3, is the paper by Murray et al., (2017) which explores the concept of CE from a multidisciplinary point of view and its application on a global context, with 983 citations. The second most cited paper is by Kalmykova et al. (2018), which reviews the CE theories to develop tools for its implementation, with 539 citations, and the third most cited paper is from Korhonen et al. (2018), about the existing debate around the concept of CE. Figure 4 shows the 16 most cited papers, with a minimum of 174 citations. Two groups of papers which cite each other can be identified, one being formed by the papers of Ahmadi et al. (2017), Esfahbodi (2016) and Kusi-Sarpong et al. (2019), and the other by the papers of Ranta et al. (2018), Witjes & Lozano (2016), Tura et al. (2019) and Rizos et al. (2016). The papers of Esfahbodi (2016), Kusi-Sarpong et al. (2019), Ranta et al. (2018) and Tura et al. (2019) are not visible due to the scaling of the figure. The warmest colours represent the most cited papers. In the list of most cited papers one can observe that the main research current nowadays is the theoretical aspect of CE, from multidisciplinary exploration and the global application proposed by Murray (2017) to the barriers that prevent the implementation of EC by SMEs (Rizos et al., 2016). Other aspects studied during the analyzed period are the sustainable assessment of Industry 4.0 technologies (Bai et al., 2020) and a comparison between the institutional barriers and the impulsors of the implementation of CE in China the United States and Europe (Ranta et al., 2018), among others.

Table 3. Top 16 most cited papers

| Author(s) | Year | Age | Title | TC | C/Y |

|---|---|---|---|---|---|

| Murray et al. | 2017 | 5 | The Circular Economy: An Interdisciplinary Exploration of the Concept and Application in a Global Context | 983 | 196.6 |

| Kalmykova et al. | 2018 | 4 | Circular economy - From review of theories and practices to development of implementation tools | 539 | 134.75 |

| Korhonen et al. | 2018 | 4 | Circular economy as an essentially contested concept | 467 | 116.75 |

| Rizos et al. | 2016 | 6 | Implementation of circular economy business models by small and medium-sized enterprises (SMEs): Barriers and enablers | 369 | 61.5 |

| Witjes & Lozano | 2016 | 6 | Towards a more Circular Economy: Proposing a framework linking sustainable public procurement and sustainable business models | 315 | 52.5 |

| Ahmadi et al. | 2017 | 5 | Assessing the social sustainability of supply chains using Best Worst Method | 296 | 59.2 |

| Bai et al. | 2020 | 2 | Industry 4.0 technologies assessment: a sustainability perspective | 270 | 135 |

| Esfahbodi et al. | 2016 | 6 | Sustainable supply chain management in emerging economies: Trade-offs between environmental and cost performance | 215 | 35.83 |

| Tura et al. | 2019 | 3 | Unlocking circular business: a framework of barriers and drivers | 207 | 69 |

| Ranta et al. | 2018 | 4 | Exploring institutional drivers and barriers of the circular economy: A cross-regional comparison of China, the US and Europe | 206 | 51.5 |

| Rosati and Faria | 2019 | 3 | Addressing the SDGs in sustainability reports: The relationship with institutional factors | 192 | 64 |

| Kusi-Sarpong et al. | 2019 | 3 | A supply chain sustainability innovation framework and evaluation methodology | 174 | 58 |

| Kjaer et al. | 2019 | 3 | Product/Service Systems for a Circular Economy: The Route to Decoupling Economic Growth from Resource Consumption? | 149 | 49.7 |

| Bocken & Geradts | 2020 | 2 | Barriers and drivers to sustainable business model innovation: Organization design and dynamic capabilities | 148 | 74 |

| Yong et al. | 2020 | 2 | Pathways towards sustainability in manufacturing organizations: Empirical evidence on the role of green human resource management | 145 | 72.5 |

| Singh et al. | 2019 | 3 | Environmental ethics, environmental performance, and competitive advantage: Role of environmental training | 142 | 47.3 |

Total citations. C/Y: Yearly citations.

Source: Own elaboration

Another aspect that can help us prove that the topics of CSR, sustainability and CE are relevant is the yearly productivity of papers. For current BMs, and based in the context of collaboration between companies and universities, there are some aspects of yearly productivity that are worth highlighting: i) The generation of knowledge: this new knowledge makes available for the organizations updated information that shows the technological advances and current practices, which help NBMs find new opportunities for growth, based on modern and current research, the development of innovations and their incorporation to their strategies (von Hippel, 2016; Schindehutte et al., 2019); ii) to become an impulsor of innovation: the different lines of research allow for the implementation of practices of diverse nature; in our case, socially responsible practices are studied. The yearly production of papers is positive for current BMs, which are supported by the ideas explained above to develop new opportunities (Boons & Ludeke-Freud, 2013; Clark, 2021; Ghosh & Van de Vrande, 2020; Rattalino, 2017; Schaltegger & Wagner, 2011); iii) The relationship of collaboration between enterprises and universities that we explained earlier gets strengthened when knowing the yearly productivity of papers. A high level of productivity encourages companies to start projects with the authors, to hire them for consultancy, formation programs and, finally, achieve the transference of results (Chesbrough, 2003); and iv) The digital transformation that nowadays is part of the development of NBMs doubtlessly entails the incorporation of socially responsible practices. To undertake a real adoption of digital technologies, academic research is a needed input which contributes to a better development of BMs (McAfee & Brynjolfsson, 2017).

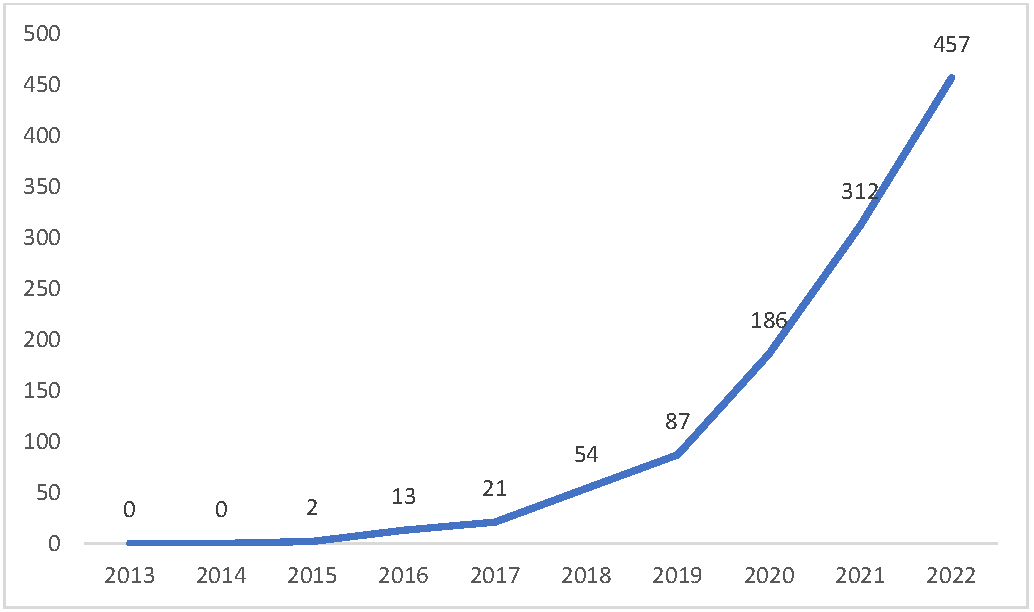

Figure 3 shows the yearly publication of papers about CSR, sustainability, and CE jointly. During the first two years of the period analyzed there were not any papers published, and 2015 was the year in which publication of papers about CE started. The most productive years are the last three years of the period, with 2022 being the most productive with 457 papers published. Table 4 shows the percentage of papers which form the total sample published each year of the period. The great majority of the papers, 92.05% of them, were published during the last four years of the period, and the other 7.95% was published during the first years of the period. Data shown both in Figure 2 and in Table 2 prove that the topic selected for the analysis is not only current, but also relevant and of interest for researchers.

Figure 3. Yearly production of papers about CSR, sustainability, and CE in the period 2013-2022

Source: Own elaboration.

Table 4. Frequency of the publication of papers about CSR, sustainability and CE in the analysed period

| Year | Relative frequency | Cumulative frequency |

|---|---|---|

| 2013 | 0% | 0% |

| 2014 | 0% | 0% |

| 2015 | 0.18% | 0.18% |

| 2016 | 1.15% | 1.33% |

| 2017 | 1.86% | 3.18% |

| 2018 | 4.77% | 7.95% |

| 2019 | 7.69% | 15.64% |

| 2020 | 16.43% | 32.07% |

| 2021 | 27.56% | 59.63% |

| 2022 | 40.37% | 100% |

Source: Own elaboration.

Figure 4. Top 16 most cited papers

Source: Own elaboration.

Journals play a fundamental role in the development of NBMs by generating an impact that helps companies make decisions. The knowledge they gain access to is a source of innovation and change, with some aspects worth highlighting: i) Possibility of accessing current research: based on the collaboration between organizations and universities, current research offers emergent practices and tendencies which offer the chance of improving or transforming a BM (Ghosh & Van de Vrande, 2020), responding to dominant patterns linked with research (Boiral & Heras-Saizarbitoria, 2016; Alvarez-Etxeberria et al., 2023) ; ii) Support for decision making: academic research is of the highest quality, and their contributions can be useful for making decisions about innovation, technology, sustainability, CE (Scarpellini et al., 2020; Schaltegger & Wagner, 2011; Scarpellini et al., 2019) etc, all of them aspects relevant for current BMs. This can help spreading new knowledge, entrepreneurship and generation of NBMs, and dynamic capabilities to achieve the adaptation to different environments (Teece, 2018; Schindehutte et al., 2019; Nambisan, 2021); and iii) Identifying best practices: research published in academic journals influence the design of BMs, applied theories, theoretical framework to support a model, focus of the problem, case studies, etc., contributing to an improvement of practices in NBMs, as well as learning from the practices of competitors and develop new businesses based on the openness and external collaboration derived of an open innovation system (Seppänen et al., 2019; Sieg et al., 2017).

Most of the papers that form the sample of the study, 414, are published in Sustainability, followed by the Journal of Cleaner Production, with 100 papers, and Business Strategy and the Environment, with 64 papers. Data are shown in full in Table 5. The journals have a high impact factor and are all in the first or second quartile.

Table 5. Journals of the sample

| Journal | Country | Quartile | h index | Frequency | Relative frequency | Total citations |

|---|---|---|---|---|---|---|

| Sustainability | Switzerland | Q1 | 33 | 414 | 36.57% | 4236 |

| Journal of Cleaner Production | United Kingdom | Q1 | 37 | 100 | 8.83% | 3898 |

| Business Strategy and the Environment | United Kingdom | Q1 | 25 | 64 | 5.65% | 1378 |

| Energies | Switzerland | Q1 | 11 | 32 | 2.83% | 305 |

| International Journal of Environmental Research and Public Health | Switzerland | Q2 | 8 | 28 | 2.47% | 160 |

| Resources, Conservation and Recycling | The Netherlands | Q1 | 15 | 21 | 1.86% | 2011 |

| Technological Forecasting and Social Change | United States | Q1 | 10 | 13 | 1.15% | 324 |

| Corporate Social Responsibility and Environmental Management | United Kingdom | Q1 | 8 | 12 | 1.06% | 175 |

| Others | - | - | - | 448 | 39.58% | - |

Source: Own elaboration.

Analyzing the lines of research, topics, keywords, citations, yearly productivity and journals has allowed us to answer the first research question, so we can affirm that CSR, sustainability, and EC are current lines of research that are able to contribute to current BMs from a collaboration between enterprises and universities approach.

Cluster 2: Company-University collaboration to support the strategies of circular business models

In the academic context the creation of networks and the collaboration between academics, businesspeople and other internal and external agents is very valuable. These networks serve to exchange ideas, experiences, the development of projects and the joint organization of different activities that contribute to the creation of synergies that contribute to the development of NBMs. With this second cluster we give an answer to RQ2 can the current BMs be supported by collaborations between companies and universities to give effect to their circular strategies? For that, we will analyse the top publishing institutions, the top publishing countries and the top external financing institutions.

Universities play a vital role in the development of NBMs, because they have both scientific and entrepreneurial talent, and they have an environment that promotes organizational innovation (Guerrero et al., 2020; Meoli et al., 2020; Clark, 2021). The collaboration between companies and universities materializes in a diverse range of actions, such as i) Development of courses: training is one of the basic goals of universities, which offer knowledge programs that will allow students to learn the management of NBMs. The collaboration between companies and universities entails the creation of joint programs directed to professionals, who can update their competencies and abilities (Clark, 2021), ii) Promotion of R&D: the generation of knowledge by groups and centres of research causes the creation and development of innovative ideas and processes. Within the framework of the specified collaboration, the university will provide the scientific basis offering solutions for diverse challenges, in the different knowledge fields, and with different reach. These solutions are well received by the companies, generating a practice-research synergy which helps NBMs to develop (Clark, 2021; Etzkowitz & Klofsten, 2021; Guerrero et al., 2020), iii) Creation of incubators: the existence of entrepreneurial incubators in universities gives support to the initial development of BMs, transforming an idea in a viable business by combining financial resources and expert mentors (Etzkowitz & Klofsten, 2021; Meoli et al., 2020) and iv) Transference of knowledge. One of the main missions of a research group, and of the university as a whole, is to transfer knowledge and technology to the businesses, which will be very positive for NBMs.

The topics are studied by European institutions mainly, by southern countries such as Portugal and Spain, by the Netherlands and by institutions from the northern countries (Norway and Finland). The Eastern countries, such as Romania and Poland, have also published a high number of papers about CSR, CE and sustainability (16 and 13 respectively). As for Asia and Oceania, three of the top publishing institution are from Australia and one comes from New Zealand. The rest come from China, Taiwan, Saudi Arabia, and Thailand. Five of the eight most productive American universities come from Brazil, one from Chile one from the United States and another from Guyana, as shown in Table 6. Even if CSR is a topic of global interest, the same as CE, data from Table 6 prove that European researchers have published the most literature of the three continents analysed. European researchers have published the most. The institutions that have published more papers will be the ones calling the attention of BMs to be formed by them, studying the creation of incubators and collaborate in the creation of knowledge. Data as those shown in Table 6 prove that both CSR and CE are topics of current interest.

Table 6. Top publishing institutions in the period 2013-2022

| Europe | ||

|---|---|---|

| Institution | Country | Number of papers |

| Delft University of Technology | The Netherlands | 17 |

| LUT University | Finland | 16 |

| Bucharest University of Economic Studies | Romania | 16 |

| Universiteit Utrecht | The Netherlands | 13 |

| Silesian University of Technology | Poland | 13 |

| Norwegian University of Science and Technology | Norway | 13 |

| Universidade Nova de Lisboa | Portugal | 13 |

| University of Zaragoza | Spain | 12 |

| University of Almería | Spain | 12 |

| Copernicus Institute of Sustainable Development | The Netherlands | 12 |

| Asia and Oceania | ||

| Institution | Country | Number of papers |

| Asia University | Taiwan | 12 |

| University of Technology Sydney | Australia | 10 |

| Queensland University of Technology | Australia | 8 |

| Dalian University of Technology | China | 7 |

| King Abdulaziz University | Saudi Arabia | 6 |

| China MedicaL University | China | 6 |

| RMIT University | Australia | 6 |

| Mahidol University | Thailand | 6 |

| Chongqing University | China | 6 |

| Auckland University of Technology | New Zealand | 6 |

| America | ||

| Institution | Country | Number of papers |

| Universidade de São Paulo | Brazil | 12 |

| Universidade Estadual Paulista Júlio de Mesquita Filho | Brazil | 8 |

| Universidade Federal Fluminense | Brazil | 7 |

| Universidade Estadual de Campinas | Brazil | 6 |

| Universidad Autónoma de Chile | Chile | 6 |

| The Business School Guyana | Guyana | 6 |

| Pontifícia Universidade Católica do Rio de Janeiro | Brazil | 5 |

| Duquesne University | United States | 4 |

Source: Own elaboration.

Academic research is carried out internationally (Barnabè & Nazir, 2021; Daddi et al., 2019), and some countries stand out from others because of the position their universities have in rankings (Chesbrough, 2018; Schindehutte et al., 2019; Nambisan, 2021). In relation to BMs that incorporate CSR, sustainability and CE one of the first countries that comes to mind is the United States, with the centre of innovation and entrepreneurship that is Silicon Valley, where numerous NBMs are developed. In Northern Europe, Finland stands out due to their highlighting of new technologies, more specifically, telecommunications and mobile applications. Germany focuses in engineering and industry, useful for the development of BMs in said areas, including sustainability and CE. The Netherlands stands out for their sustainability and circularity approaches. In Spain numerous research has been conducted by different research groups about sustainability and CE (Scarpellini et al., 2019; Scarpellini, 2022), from different knowledge fields due to the transversality of research. China is also worth highlighting, because it is a country where research has grown very quickly, as well as BMs focused on technology, e-commerce, online sales, artificial intelligence, etc., which has generated innovation both of ideas and of processes, helped by the contributions of groups, research institutes and universities. The relationship between enterprise and university will transform traditional BMs in current models, developing new opportunities that will create value derived from knowledge and that will allow to tackle numerous challenges (Chesbrough, 2018; Nambisan, 2021).

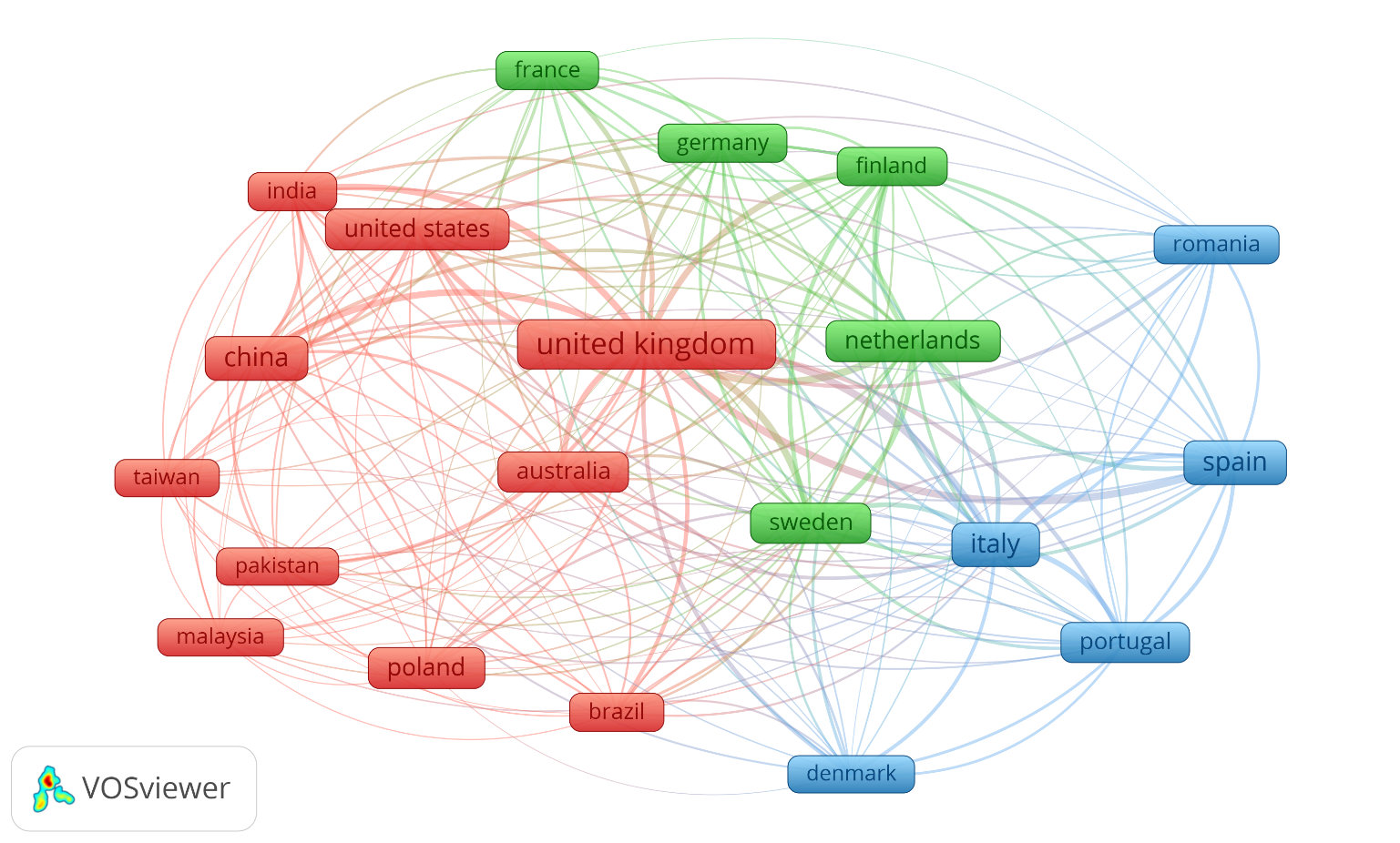

The 1132 papers that form the sample have been authored by 1906 researchers of 86 countries. Table 7 showns the 20 top publishing countries which have published a minimum of 32 papers with 388 citations about CSR, CE and sustainability. Figure 5 also shows the 20 countries that have published a mínimum of 32 papers with 388 citations. Several clusters of countries which work together can be observed: United States and India, China and Taiwan, Pakistan and Malaysia, the UK and Australia, and Italy and Portugal. In Figure 5, the countries that have published together the most appeared linked by the greatest number of lines.

Table 7. Countries whose researchers have published the most in the period 2013-2022

| Country | Frequency | Relative frequency | Total citations | h index |

|---|---|---|---|---|

| United Kingdom | 216 | 11.33% | 6590 | 45 |

| Italy | 130 | 6.82% | 2473 | 31 |

| China | 124 | 6.51% | 2397 | 26 |

| Spain | 116 | 6.09% | 1772 | 26 |

| The Netherlands | 78 | 4.09% | 2481 | 28 |

| Poland | 71 | 3.73% | 817 | 19 |

| United States | 69 | 3.62% | 1786 | 24 |

| Australia | 58 | 3.04% | 1198 | 21 |

| Sweden | 56 | 2.94% | 2147 | 23 |

| Portugal | 55 | 2.89% | 552 | 15 |

| Brazil | 52 | 2.73% | 653 | 13 |

| Finland | 51 | 2.68% | 1969 | 23 |

| Germany | 49 | 2.57% | 991 | 18 |

| India | 47 | 2.47% | 1170 | 21 |

| Romania | 46 | 2.41% | 294 | 11 |

| France | 40 | 2.10% | 872 | 17 |

| Malaysia | 38 | 1.99% | 502 | 13 |

| Pakistan | 36 | 1.89% | 479 | 13 |

| Denmark | 34 | 1.78% | 1066 | 18 |

| Taiwan | 32 | 1.68% | 388 | 12 |

Source: Own elaboration.

Figure 5. Countries that have published the most in the period 2013-2022

Source: Own elaboration.

Financing institutions play a key role in the relationship between universities and enterprises, contributing to the development of current BMs. This support materialises in different areas: i) Initial support of entrepreneurship of a BM: The start of every BM needs financial support, which can be given by financial institutions, business angels, university foundations, national and international entities and other venture capital firms in collaboration with universities (Cumming, 2020; Colombo & Grilli, 2021; Ahlers et al., 2020; Hornuf & Schwienbacher, 2021); ii) Mentorship, both professional and financial: the development of the BM needs a mentorship that can be given by universities, organisms and institutions linked to universities. Entrepreneurs can learn knowledge, advice and ways of working, process development, and how to start sustainable and circular activities, things currently done by universities and consulting firms relating to viability, risk assessment, and opportunity analysis (Ahlers et al., 2020) and iii) The access to knowledge and research networks from the mentioned entities, and based on collaboration agreements and investing consortia, the NBMs can connect with key actors in the business ecosystem. These collaborations will define opportunities for development and expansion of NBMs (Ahlers et al., 2020).

According to the results of the bibliometric analysis, 645 of the 1132 papers that form the sample have received external financing. In Europe there are some relevant supranational financing institutions, such as the Horizon 2020 Framework Programme, the European Commission and the European Regional Development Fund (ERDF), with 78, 39 and 19 papers respectively. As for national institutions, the most committed is the Academy of Finland. It is worth noting that, in Asia, the institutions that have financed the most papers all but two come from China, and in America, they are all Brazilian except from one from the United States (Table 8). The European institutions are the most committed to CSR and CE research. The analysis will allow NBMs to get support from financial institutions to start a new business, receive support and get access to networks that can give them the necessary means to develop circular and sustainable processes.

Table 8. Top financing institutions in the period 2013-2022

| Institution | Country/region | Number of papers |

|---|---|---|

| Europe | ||

| Horizon 2020 Framework Programme | Europe | 78 |

| European Commission | Europe | 39 |

| European Regional Development Fund | Europe | 19 |

| Academy of Finland | Finland | 12 |

| Asia | ||

| National Natural Science Foundation of China | China | 30 |

| Ministry of Science and Technology | Taiwan | 12 |

| National Office for Philosophy and Social Sciences | China | 10 |

| Fundamental Research Funds for the Central Universities | China | 9 |

| Ministry of Higher Education | Malaysia | 5 |

| America | ||

| Fundação para a Ciência e a Tecnologia | Brazil | 25 |

| Coordenação de Aperfeiçoamento de Pessoal de Nível Superior | Brazil | 22 |

| Conselho Nacional de Desenvolvimento Científico e Tecnológico | Brazil | 17 |

| Fundação de Amparo à Pesquisa do Estado de São Paulo | Brazil | 6 |

| College of Science and Engineering, University of Minnesota | United States | 3 |

Source: Own elaboration.

Cluster 3: Opportunity of the theoretical framework to support circular business models

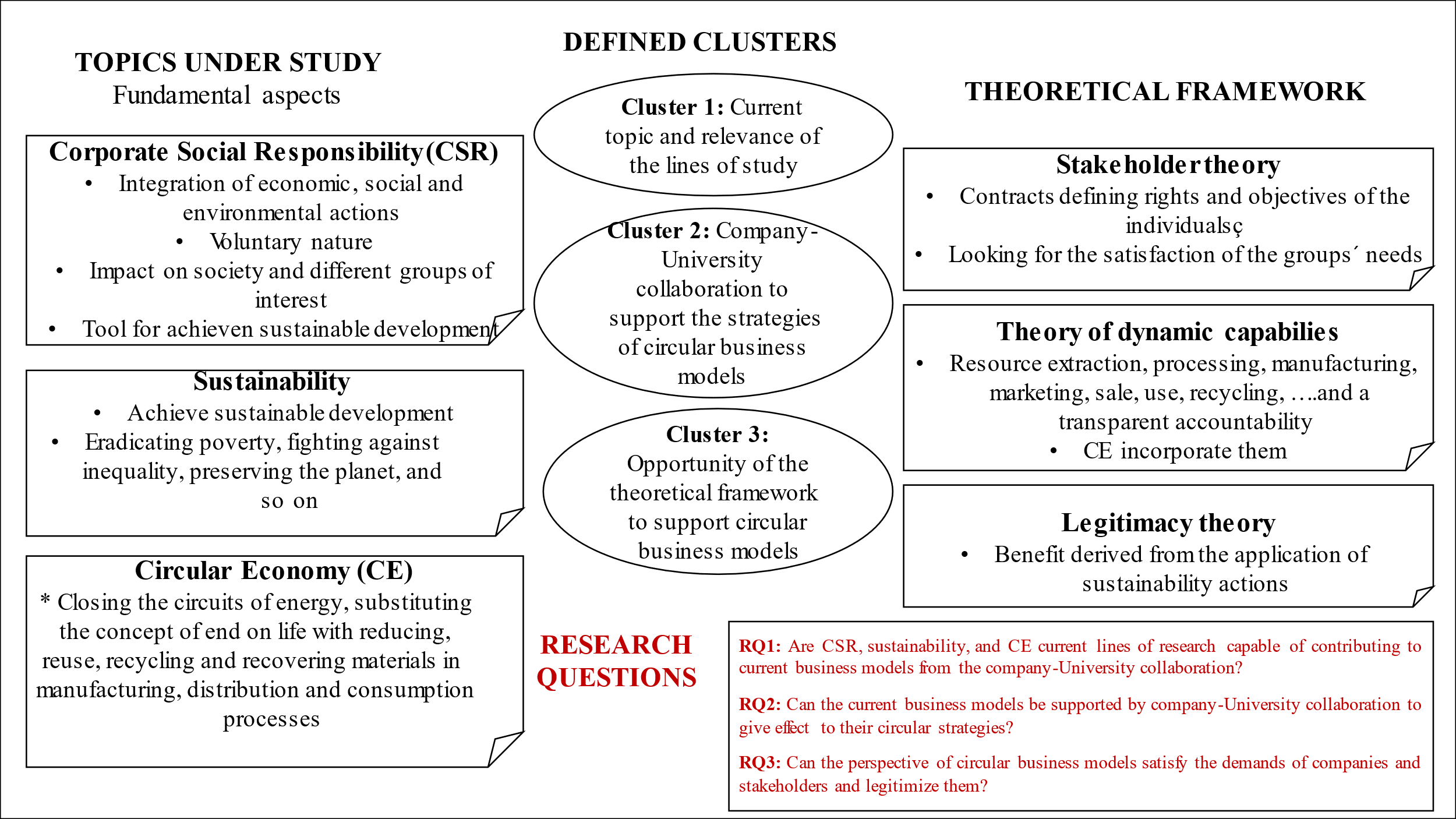

In the third and last cluster we answer RQ3 Can the perspective of circular business models satisfy the demands of companies and stakeholders and legitimize them? This is our own contribution because no previous theoretical frameworks exist that explain the integration of stakeholders in NBMs and the ability of said models to legitimize. This cluster is supported by the anaylisis of the stakeholders, dynamic capabilities and legitimacy theories, and we link the theoretical constructs with NBMs practice. The explanation is shown in full in Figure 6.

Figure 6. Theoretical framework to support circular business models

Source: Own elaboration.

NBMs with a circular perspective present a strategic positioning in business, because they highlight the important need of defining a holistic structure that incorporates sustainability and CE (Zott et al., 2011). At the same time, they can not lose the chance of getting a good economic performance nor of satisfying stakeholders' needs (Teece, 2010; Osterwalder & Pigneur, 2011; Chesbrough & Rosenbloom, 2002). Circular models can decrease damages caused by social and environmental impact (Pomponi & Moncaster, 2016; Rauter et al., 2017; Witjes & Lozano, 2016; Scarpellini, 2022), which affects all stakeholders and society.

The use of dynamic capabilities associated with resources and that can minimise the generated impact will improve the position of stakeholders, as well as generate legitimacy for the BMs which implement it (Dey et al., 2020; Schaltegger et al., 2023). We reference the ability to decrease raw materials use, use renewable energy and all type of sustainability resources (Zamfir et al., 2017; Scarpellini, 2022) which imply a link with the suppliers of said resources, with society, customers and other stakeholders. From the point of view of sustainability accounting, the resources and dynamic capabilities employed will be reflected in non-financial accounting information (Scarpellini et al., 2020; Barnabè & Nazir, 2021), constituting other value-generating added resources.

Based on the company-University approach, and as a manifestation of the collaboration between both parties, it is observed how the NBMs need research resources that will be provided by the universities, while these, in addition to offering lines of research, find coverage in market niches. Therefore, the orientation of the present study, under the perspective of the CE incorporated in the NBMs, involves attending to the numerous interest groups (shareholders, customers, suppliers, public administration, researchers, politicians, and so on) under sustainable strategies of lower impact (Korhonen et al., 2018), being a clear manifestation of how the NBMs support the theory of stakeholders (Pomponi & Moncaster, 2016; Rossi et al., 2020; Kirschherr & Piscicelli, 2019; Iacovidou et al., 2017; Daddi et al., 2019). The integration of the points of view of all stakeholders and the pressure to which they are sometimes subjected are aspects also taken into account by NBMs (Martínez-Martínez et al., 2017; Richter & Dow, 2017; Rattalino, 2017; Vaitoonkiat & Charoensukmongkol, 2020).

Finally, circular and sustainable strategies are beneficial for NBMs in many aspects, which ultimately increase respect for the company and improve its competitive position, with the consequent gain of legitimacy (Campbell, 2007; Scherer & Palazzo, 2011; Odriozola & Baraibar‐Diez, 2017). With respect to accountability, NBMs carry out an operational and responsible communication process, addressing it with transparency and gaining legitimacy equally (Anwar et al., 2019; Daddi et al., 2019; Hahn & Kühnen, 2013; Stewart & Niero, 2018).

6. Discussion

CSR and CE continue to be topics of great interest for the accounting and management of current BMs. While CSR is a mechanism for the voluntary implementation of actions in the triple sense (economic, social and environmental), CE is receiving increasing attention, because it aims to integrate economic activity and environmental well-being (Negri et al., 2021; Scarpellini, 2022; Schaltegger et al., 2023; Llena-Macarulla et al., 2023). This approach involves minimizing the consumption of finite natural resources by keeping resources in the economy for longer, thus generating economic growth (Merli et al., 2018; Korhonen et al., 2018; Scarpellini, 2022). This represents a change in the concept of the interaction of human society with nature, and the new concept aims to change the idea of the end of life of products by a reduction, recycling and reuse of materials (Sopelana et al., 2021; Dey et al., 2020; Llena-Macarulla et al., 2023).

This is the approach we have approached from a bibliometric analysis of the existing literature on sustainability and CE simultaneously. Specifically, a search was carried out in May 2023 in the Scopus database, identifying 1132 papers containing one or more of the keywords "Corporate Social Responsibility", "Sustainability" or "Circular Economy", published between 2013 and 2022, that were open access and written in English. To study the sample, VosViewer software version 1.6.19 was used. We can affirm that this is the first paper in the literature with these characteristics, thematic, wide period, while analyzed from a triplet of theories (stakeholders, dynamic capabilities, and legitimacy), and that it constitutes a contribution for the NBMs from the company-University collaboration.

Working on CSR and CE is of fundamental importance for current BMs, and these strategies must be placed at the center of their business (Rauter et al., 2017; Witjes & Lozano, 2016; Scarpellini, 2022). In this context, we refer to circular BMs as those that must work on sustainability with a strategy that goes beyond those established for linear models (European Commission, 2020; Schaltegger et al., 2023). These circular businesses will work on reducing environmental burdens, as well as investing to generate more durable products, while maintaining the creation of value, both economic and operational in the company (Korhonen et al., 2018; Nyström et al., 2021; Ahlers et al., 2020; Llena-Macarulla et al., 2023). This transition towards circular models, generating the value that every company wants to obtain, defines CE as an area of obligatory study as well as of current relevance in all aspects (Sopelana et al., 2021; Schaltegger et al., 2023). In this way, the vision of all BM is given meaning as an integrated model that creates value and delivers it to its customers (Teece, 2010; Osterwalder & Pigneur, 2011).

We would like to highlight the broad theoretical framework, integrated by the stakeholders, dynamic capabilities, and legitimacy theories, which underpins the study. First, the stakeholders theory defines NBMs as stakeholders that, depending on their responsibilities, will be able to generate the transition to the circular economy (Pomponi & Moncaster, 2016; Rossi et al., 2020). This determines commitment on the part of the company and the other stakeholders, as well as the ability to carry out social and environmental actions that will have an impact on responsible accounting management (Turker, 2008; Daddi et al., 2019; Vaitoonkiat & Charoensukmongkol, 2020; Llena-Macarulla et al., 2023). Second, the dynamic capabilities theory shows that NBMs reflect new business opportunities, using the company's idoneous resources and capabilities (Kachouie et al., 2018; Gallardo-Vázquez & Valdez-Juárez, 2022), and generating sustainable strategic results by executing the different actions of extraction, use, recycling, sale, and accountability (Orazalin & Mahmood, 2018; Schaltegger et al., 2017). Third, the legitimacy theory supports the achievement of a better positioning from the exercise of circular actions in the BMs (Scherer & Palazzo, 2011; Odriozola & Baraibar‐Diez, 2017). Both from a cognitive and pragmatic point of view, the incorporation of CE is supported, generating sustainable competitive advantages, as well as accountability (Daddi et al., 2019; Stewart & Niero, 2018). Therefore, we can affirm that linear business models are not enough today, it is necessary to move towards circular models, which will allow to achieve the satisfaction of all stakeholders and achieve legitimacy, from a good use of their dynamic capabilities.

7. Conclusions, limitations, and future lines of research

Being aware of the importance of research in sustainability, and more recently and more particularly, in CE, we have approached the present study, trying to know the increasing number of existing publications in an ample period of time. At the same time, we have tried to make the study e useful for NBMs, if not directly in the way of undertaking their daily management, then in the sense of providing them with ways of getting closer, through the universities that, based on that coloration between both entities, can serve as guidance for the work they have to initiate and manage.

The set of results obtained has allowed us to define 3 clusters: i) Cluster 1: Current topic and relevance of the lines of study; ii) Cluster 2: Company-University collaboration to support the strategies of circular business models, and iii) Cluster 3: Opportunity of the theoretical framework to support circular business models, from which research questions have been answered. The first one (RQ1) tells us that CSR, sustainability, and EC turn out to be current lines of research, capable of contributing to the needs of NBMs, and can be answered from Cluster 1. Sustainability strategies should be incorporated into NBMs for the adoption of circular approaches, and the knowledge generated in universities will be an input of great value for them. This contribution will be possible given the large number of papers and citations that we find in areas from which to focus the issues that concern us, as well as the annual productivity observed. The second research question (RQ2) tells us if the BMs can rely on company-university collaboration to make their circular strategies effective and can be answered from Cluster 2. The generation of networks and concerts will facilitate the development of initiatives and projects for NBMs, constituting an attraction for both parties. This contribution will be possible given the ranking of the university institutions and the funding entities. The third research question (RQ3) tells us whether the perspective of circular BMs can satisfy the demands of the company and legitimize them and can be answered from Cluster 3.

Results from Cluster 1 that are worth noting are that the most frequent topic in the sample is Environmental Science, with 787 papers and 1338 citations, the most cited paper is Murray et al. (2017) with 983 citations in 5 years, and that 92.05% of the papers of the sample were published during the last three years of the decade we have analysed (2020, 2021 and 2022). 26.57% of the sample comes from Sustainability. In Cluster 2, it is worth highlighting that the university that has published the most is the Delft University of Technology, in the Netherlands (17 papers), that the UK has the most researchers present in the sample (216 of 1906 researchers) and that the top external financing institution is the Horizon 2020 Framework Programme from the European Commission, with 78 papers.

The study presents several contributions of interest. First, it provides an improvement of the literature on CSR, sustainability and CE, expanding possibilities for studies beyond more traditional ones that address social and environmental information (Alvarez-Etxeberria et al., 2023; Correa, 2011; Leal et al., 2019; Blanco-Zaitegi et al., 2022; Llena-Macarulla et al., 2023). Secondly, the methodology used begins to show interest in the areas of business management and administration (Boiral, Guillaumie, Heras-Saizarbitoria, & Tayo, 2018; Blanco-Zaitegi et al., 2022), opening doors to the search for findings that link social, environmental and management issues with the business world, based on their application to NBMs based on company-university collaboration. In this way, it links to previous research related to sustainability reporting (Scarpellini, 2022; Alvarez-Etxeberria et al., 2023; Llena-Macarulla et al., 2023). Thirdly, the study is based on a theoretical framework, based on three theories, which manages to explain the research questions raised. In this way, the paper makes the results available to different stakeholders such as researchers, politicians, and other groups of interest.

We consider our research to be original because it addresses a current topic of study, based on a fairly novel methodology, framed in a triplet of theories, and that goes beyond the academy itself, giving value to external collaborations.

This research has several limitations. First, having chosen a single database reduces the number of articles that make up the study sample. Although Scopus has been chosen for its greater number of references compared to Web of Science, using this second database would have increased the sample size and, with it, the depth of the analysis. A second limitation is that of the language in which the articles that make up the sample are written since, by selecting only articles in English and not including other languages, the productivity of both Spanish and Latin American universities has been affected.

The study leaves several possible lines of research open, such as carrying out this same study, but with articles from the Web of Science platform, as well as articles written in a second language, such as Spanish. A second line of research that remains open is to carry out bibliometric reviews of CE practices carried out in specific industrial sectors, as well as segmented analyses according to the size of the companies.