An integrated corporate governance index for Spain: From construction to construct validity

ABSTRACT

This study, based on agency theory, focuses on the measurement of corporate governance in the Spanish corporate sector. Its aim is to develop, evaluate and validate a specific corporate governance index that overcomes the limitations of previous research, which relies on aggregated and unvalidated measures.

The research questions are: How can corporate governance in Spain be adequately measured? And how well does the proposed index represent the relevant aspects of corporate governance? These questions lead to the sub-question of the validity of the sub-indices that make up the index in relation to specific aspects of corporate governance.

The study analyses a sample of 130 Spanish listed companies with 1,039 observations corresponding to the period from 2007 to 2018. An aggregate corporate governance index is constructed, composed of four sub-indices: compliance with good governance codes, ownership characteristics, board characteristics and transparency of accounting information.

The results show that both the overall index and the sub-indices are positively related to firm value. Methods such as Cronbach's alpha coefficient for internal consistency and Principal Component Analysis (PCA) for index structure are used to validate the index. In addition, panel data analysis using the GMM method is employed, incorporating a novel measure of firm value that takes into account the replacement cost of assets.

This study fills a gap in the literature by constructing and validating a specific index for Spain, while addressing econometric issues such as endogeneity and unobservable heterogeneity. In practical terms, the index can support the implementation of the United Nations 2030 Sustainable Development Agenda, which promotes the adoption of good governance codes.

Finally, it is suggested that future research should focus on creating and validating robust indices to assess the quality of corporate governance in other contexts, thereby promoting best practices globally.

Keywords: Corporate governance index; Construct validity; Codes of good governance; Boards of directors; Ownership structure; Financial reporting; Firm value.

JEL classification: G18; G30; G34; G39; K22; K29.

Índice integrado de gobierno corporativo para el mercado español: desarrollo y validación

RESUMEN

Este estudio, basado en la teoría de la agencia, se centra en la medición del gobierno corporativo en el sector corporativo español. Su objetivo es desarrollar, evaluar y validar un índice específico de gobierno corporativo que supere las limitaciones de investigaciones previas, las cuales se basan en medidas agregadas y no validadas.

Las preguntas de investigación son: ?`cómo medir adecuadamente el gobierno corporativo en España?, y ?`cuán bien representa el índice propuesto los aspectos relevantes del gobierno corporativo? De estas preguntas se deriva una sub-pregunta sobre la validez de los subíndices que componen el índice en relación con los aspectos específicos del gobierno corporativo.

El estudio analiza una muestra de 130 empresas españolas cotizadas con 1.039 observaciones correspondientes al período 2007-2018. Se construye un índice agregado de gobierno corporativo, compuesto por cuatro subíndices: cumplimiento con códigos de buen gobierno, características de la propiedad, características de los consejos directivos y transparencia de la información contable.

Los resultados muestran que tanto el índice general como los subíndices están positivamente relacionados con el valor de la empresa. Para validar el índice, se utilizan métodos como el coeficiente de Cronbach $\alpha$ para la consistencia interna y el análisis de componentes principales (PCA) para la estructura del índice. También se emplea el análisis de datos de panel GMM, incorporando una medida novedosa del valor de la empresa que considera el coste de reposición de los activos.

Este estudio llena un vacío en la literatura al crear y validar un índice específico para España, abordando además problemas econométricos como la endogeneidad y la heterogeneidad inobservable. A nivel práctico, el índice puede apoyar la implementación de la Agenda de Desarrollo Sostenible 2030 de las Naciones Unidas, que promueve la adopción de códigos de buen gobierno.

Finalmente, se sugiere que futuras investigaciones se enfoquen en la creación y validación de índices robustos para evaluar la calidad del gobierno corporativo en otros contextos, promoviendo así las mejores prácticas a nivel global.

Palabras clave: Índice de gobierno corporativo; Validez del constructo; Códigos de buen gobierno; Consejo directivo; Estructura de propiedad; Informes financieros; Valor de la empresa.

Códigos JEL: G18; G30; G34; G39; K22; K29.

1. Introduction

It is now almost fifty years since the term corporate governance was first used. The growing interest in understanding how corporate governance works and how it is measured is reflected in the large number of studies published in recent decades (Chen et al., 2007; Nsour & Al-Rjoub, 2022). However, we still know little about corporate governance and even less about its relationship with other business areas such as gender diversity, corporate environmental impact, human rights and corporate social responsibility (Ahrens et al., 2011; Ouni et al., 2020; Zheng & Kouwenberg, 2019). And measures of corporate governance are not consistent across the world. Many academic works, such as Drobetz et al. (2004) and Black et al. (2006), have aimed to construct indices to measure corporate governance, but have not tested their validity. Nerantzidis (2016) sheds light on the need to construct an index that is valid and reliable. This need is also in line with the finding of Andreu-Pinillos et al. (2020), in the case of Spain, that not all items included in corporate governance and sustainability indices are homogeneous and interchangeable.

As noted, there are many shortcomings in the literature on the construction of a corporate governance index - including uncertainty about how to measure the construct of corporate governance, lack of comparability, lack of uniformity, lack of comprehensiveness and, most importantly, lack of construct validity - that cast doubt on the reliability of such indices and the findings derived from them (Bhagal et al., 2008). This lack of validity makes current indices highly imperfect instruments for deciding how to vote on corporate proxies and for assessing the relationship between such indices and company value. Therefore, any causal relationship between governance indices and firm value found in the literature may be highly biased because the proxy for the effectiveness of the governance system may not actually measure the underlying governance characteristics (Chen et al., 2007). Indeed, we argue that the literature has not properly assessed the relationship between governance and firm value because its construct of corporate governance lacks validity.

Hence, our main motivation is to rectify these weaknesses by using a proxy of corporate governance that measures the underlying concept of governance and not other corporate dynamics. Therefore, our aim is to construct a comprehensive index of corporate governance as a driver of firm value in the Spanish corporate sector and to test its validity. The main research questions are: How can we properly measure the construct of corporate governance for the Spanish corporate sector? How well does our suggested corporate governance index represent the reality of corporate governance in general? And how well do its subindices represent the specific aspects of governance? These last two questions are related to the construct-validity process.

Our study contributes to the literature in four ways. First, it offers a validated index of corporate governance for Spain. The literature uses proxies that do not necessarily measure attributes of corporate governance and their relation to firm value. For instance, Aggarwal et al. (2009) develop a firm-level corporate governance index that enables cross-country comparisons. However, since the authors remain silent regarding the validity of their index, it is hard to tell whether their metric of corporate governance actually measures firm-level corporate governance attributes, as pointed out by Bhagal et al. (2008).

Second, our study generates concerns about what existing measures of corporate governance really measure and how. For instance, Gompers et al. (2003) use twenty-four corporate governance provisions as proxies for the balance of power between shareholders and managers. The authors recognize that most of the provisions are proxies of corporate governance. However, they also argue that there are some ambiguous cases and suggest that there might be certain elements in their index that account for not governance but something else. Indeed, Bebchuk et al. (2008) assess the relative importance of Gompers et al. (2003)'s twenty-four provisions and find that eighteen of them are uncorrelated with firm valuation and abnormal returns. This suggests that Gompers et al. (2003) index is less a proxy of corporate governance than a proxy of other corporate aspects. Our study mitigates such flaws in the literature.

A third contribution is that our index, unlike classical corporate governance indices such as the G-index (Gompers et al., 2003), the E index (Bebchuk et al., 2008), and the O index (Straska & Waller, 2014), relies on an appropriate econometric approach to deal with endogeneity issues and heterogeneity problems that have not been properly treated in the empirical literature. Similarly, our study improves the existing estimations by using more suitable proxies of firm value that consider the replacement cost of assets vis-à-vis the traditional Tobin’s Q, and it uses various metrics of the components of our suggested index’s subindices. None of these studies properly address endogeneity issues caused by both the causality of the relationship and omitted variables, which might bias their findings (Karpoff et al., 2017), nor do they use the superior, replacement-cost-based proxy of firm value (Saona, 2014). Such problems might indicate that statistically significant relationships between their indices and firm value may be the result of correlation with an omitted variable that is the true predictor of firm value (Black et al., 2017).

Fourth, corporate governance has been on the political agenda of national and supranational institutions, such as the United Nations 2030 Agenda for Sustainable Development, which, among other things, establishes a framework for corporations seeking to implement good corporate governance practices, and our suggested index provides an appropriate measurement of the construct of governance. Consequently, this study helps the literature to advance this new agenda by legitimating future research on corporate governance using our validated Spanish corporate governance index.

Although there are multiple definitions of corporate governance (Claessens & Yurtoglu, 2013), all of them view it as the way in which suppliers of funds to corporations ensure they will get a return on their investment (Shleifer & Vishny, 1997). Corporate governance involves a set of conditions that support stakeholders’ interests, preventing the agency problems arising from the separation of ownership and control. Hence, corporate governance is seen as the system by which companies are efficiently managed and controlled. As stated by Jensen (1993), corporate governance concerns four areas: capital markets, the legal-political-regulatory system, product and factor markets, and internal systems.

Along the same lines, Ocasio & Joseph (2005) describe the evolution of the concept of corporate governance from the ’70s to the end of the twentieth century and explain how it has been associated with the preservation and promotion of shareholder value. They suggest that the term corporate governance has become popular in the corporate sector because of growing shareholder understanding of issues concerning institutional investors’ roles in takeover defenses, board structure, and executive compensation. Moreover, corporate governance has come to be widely recognized in the corporate conscience as the set of mechanisms designed to ensure that suppliers of financing receive a satisfactory risk-adjusted return on their investments as defined by Shleifer & Vishny (1997).

As observed above, corporate governance has gained momentum elsewhere in its association with different corporate dimensions, such as firm value and performance (Claessens & Yurtoglu, 2013; Denis & McConnell, 2003; Nasrallah & El Khoury, 2022; Shleifer & Vishny, 1997). But measures of corporate governance are still lacking. Stakeholders have started to demand governance ratings (Sherman, 2004) to avoid undesirable outcomes (Daines et al., 2010). This new trend has led to efforts at measuring governance quality (Aguilera Ruth & Desender Kurt, 2012), both by academics (Cheung et al., 2011; Cheung et al., 2007; La Porta et al., 1998; Tsipouri & Xanthakis, 2004) and by commercial agencies such as Governance Metrics International, Risk Metrics/Institutional Shareholder Service, Credit Lyonnais Securities, and Standard & Poor’s.

Since corporate governance, being unobservable and abstract, cannot be precisely measured (Black et al., 2017), the empirical literature commonly relies on indices of firm-level proxy variables (Sami et al., 2011). However, as stated by Nerantzidis (2016), the indices are imperfect and sometimes do not measure what they are supposed to measure. The reasons for such imperfection include spurious correlations, incomplete knowledge about the governance phenomenon under study, the subjectivity of researchers’ judgments as applied to the estimations, and the limitations of direct observation (Black et al., 2020).

The idea of measuring corporate governance quality through indices is relatively new, and several approaches have been developed thus far (Black et al., 2017; Daines et al., 2010; Kocmanová & Šimberová, 2014; Leech & Manjón, 2002; Renders et al., 2010). This study takes a comprehensive approach to it.

Using agency theory, our study follows the approach of Black et al. (2017) and applies a construct-validity process in the index construction. The data used for the construction of our index correspond to several years of microlevel data, which allows for the creation of panel structures. Hence, we use comparable constructs that proxy for similar underlying corporate governance attributes. We take a top-down approach in which we first identify several governance attributes, based mostly on (i) empirical evidence on the Spanish market and (ii) ad hoc variables suggested by corporate governance theories and our criteria (variables such as features of boards of directors, codes of good governance, financial transparency, and ownership structure). With these elements, we build proxies for general attributes of governance and then use them to create a governance index for Spanish capital markets, which we name the Spanish Corporate Governance Index (S-CGI).

We choose these ad hoc variables for the following reasons. First, codes of good governance are chosen because a company’s governance needs to be aligned with the external regulatory framework (Aguilera & Cuervo-Cazurra, 2009). Second, boards of directors are an essential aspect of internal corporate governance since their fiduciary role is to protect shareholders’ rights (Booth et al., 2002). Third, concerning ownership structure, we believe that one of the major governance characteristics of companies operating in civil-law countries, such as Spanish companies, is their concentrated and pyramidal ownership structure (de Miguel et al., 2004). This is a natural consequence of relatively weak external governance systems. Finally, we include financial transparency because the literature on Spanish firms has increasingly considered earnings management and the quality of the financial reporting in recent years (Prior et al., 2019). This growth is a symptom of concerns in academia regarding the need to consider financial transparency in corporate governance studies given the prevalence of corporate scandals and misreported financial information. Hence, we follow the recommendations of Black et al. (2020), who propose applying their approach to construct validity to country level governance indices, and we show that the Spanish corporate sector offers the characteristics needed to conduct the empirical analysis.

Following Black et al. (2017) road map for assessing validity, we apply Cronbach (1951) \(\alpha\), the most popular instrument for testing the reliability of measurement instruments (Ararat et al., 2017; Bozec & Bozec, 2012; Nerantzidis, 2016). If the elements used to construct a subindex collectively measure the same attribute of governance, then the elements will be positively correlated, yielding a relatively high Cronbach’s \(\alpha\). However, if the various elements measure different attributes, the estimated Cronbach’s \(\alpha\) for the subindex will not be high (Chen et al., 2007; Hoekstra et al., 2019).

The second approach used to test construct validity is principal component analysis (PCA). Since we account for many variables that measure the same corporate governance attribute, we create clusters. The major benefits of this technique are that, first, the factors created are not correlated and, second, the factors incorporate a large amount of the variability of the individual variables used to estimate the factors (Kim & Mueller, 1978). The methodology also incorporates the validation process of the created corporate governance index in which it is later used to explain firm value. Our study goes one step beyond other publications by testing firm value with a suitable measure for validation. The superior, novel firm-value variable we use is derived from Tobin’s Q but factored by the reposition cost of assets.

The study continues as follows. Section 2 reviews the literature on corporate governance indices. Section 3 describes our methodology. We validate our proposed corporate governance index in Section 4. Finally, we conclude in Section 5.

2. Literature review

Agency theory is the fundamental basis for many academic studies of corporate governance (Bathala et al., 1994; Berger & Bonaccorsi di Patti, 2006; Block, 2012; Cuevas-Rodríguez et al., 2012; Eisenhardt, 1989; Garbade & Silber, 1982; Jensen, 1994; Jiraporn et al., 2008). It concerns the conflicts of interest in companies due to disparities in parties’ incentives (Berle & Means, 1932; Jensen & Meckling, 1976; Vitolla et al., 2020). These conflicts of interest call for mechanisms to protect shareholders against managers, and these mechanisms give rise to corporate governance (Aguilera Ruth & Desender Kurt, 2012; Ararat et al., 2020; Filatotchev et al., 2013; Mayer, 1998).

As noted, there are multiple definitions of corporate governance, but in the classical definition (Brown et al., 2011; Kumari & Pattanayak, 2014; Mayer, 1998; Williamson, 1988) it is the set of systems that ensure companies are managed in the interest of all stakeholders.

Multiple approaches and measures have been used to construct governance indices. For instance, Gompers et al. (2003) develop a broad index (G-index) based on twenty-four variables tracked by the Investor Responsibility Research Center for approximately 1,500 US firms with equal weighting. The index is negatively correlated with firm value (measured using Tobin’s Q). Bebchuk & Cohen (2005) construct an entrenchment index based on six factors selected from twenty-three governance factors developed by the research center. Brown & Caylor (2009), using a broader index based on the governance provisions mandated by the three major US stock exchanges, find that corporate governance is positively correlated with operating performance, market valuation, and dividend payout for a large sample of US firms.

Black et al. (2006) construct a corporate governance index for 515 Korean companies using a survey conducted by the Korea Stock Exchange. They find a positive correlation between corporate governance practices and market valuation as measured by Tobin’s Q and market-to-book ratio. Similar results have been documented by Beiner et al. (2006) in Europe, Ahmadjian (2012) in Japan, and Klapper & Love (2004) in twenty-five emerging markets. Following Aman & Nguyen (2008), Brown & Caylor (2009) construct a governance index based on several attributes associated with good corporate governance such as board composition, ownership structure, and disclosure policy. Though all these works build corporate governance indices, none develop the construct-validity process, which is essential to ensure that the indices actually measure governance attributes and no other features correlated with governance.

Unlike Gompers et al. (2003) index, which measures firms’ resistance to external-control mechanisms (such as takeovers), our index emphasizes the quality of firms’ internal controls. In that sense, our index is closer to that of Aman & Nguyen (2008), Brown & Caylor (2009), Black et al. (2010), and Black et al. (2017). We consider a few internal, firm-level aspects of governance that have not been studied before. In the following sections, we review each variable and justify their inclusion in our index.

Despite a general consensus on the importance of corporate governance, the findings of the vast majority of existing governance studies are mixed, raising major concerns as to whether the governance constructs that are often employed are valid proxies for the complex and unobservable concept of governance that they intend to measure (Black et al., 2017). Indeed, Larcker et al., (2007, p. 964) argue that the measurement error that may be introduced from using a single governance mechanism (for example, board size) as a proxy “will almost certainly cause the regression coefficients to be inconsistent.” They suggest that using multiple indicators can avoid that measurement error.

Other researchers seek to address the measurement-error issue by constructing governance indices that contain multiple measures. According to Elmagrhi et al. (2020), there are three major problems with such indices. First, as there is no theoretical basis for selecting governance provisions, such indices are often naively constructed (Brown & Caylor, 2009), thereby resulting in similar measurement errors (Black et al., 2017; Larcker et al., 2007).

Second, it is not only practically impossible to include all relevant governance provisions but likely that not all included provisions will be relevant; therefore, measurement problems such as omitted-variable bias are likely to persist in such governance indices (Black et al., 2017; Denes et al., 2017; Larcker et al., 2007) 1. Consequently, a small but growing number of researchers have recently employed statistical approaches in developing more reliable governance indices, such as Black et al. (2017), Karpoff et al. (2017), and Larcker et al. (2007). Larcker et al. (2007), for example, employ PCA to develop an alternative disclosure index containing fourteen key components out of thirty-nine governance provisions for US firms, and they demonstrate that it is more reliable and better specified compared with previous ones, such as the G-disclosure index (Gompers et al., 2003). We also employ the PCA to develop an alternative corporate governance disclosure index for Spanish firms.

Third, despite increasing anecdotal evidence suggesting that corporate executives below the CEO level, such as CFOs, receive pay packages as large as those of CEOs, existing studies have mainly investigated the determinants of CEO pay (for example, Core et al. (1999); Dong & Ozkan (2008); Adams & Ferreira (2009); Fahlenbrach (2009); Guest (2009); Brick et al. (2006); so, relatively little is known about the impact of firm-level corporate governance on the pay packages of other executives. All these studies show that the construction of corporate governance indices is still being debated (see, for instance, Benvenuto et al. (2021), Mishra et al. (2021), López-Quesada et al. (2018), Nerantzidis (2016), Kocmanová & Šimberová (2014), Kaufmann et al. (2011), and Chen et al. (2007), among others).

Empirically, Benvenuto et al. (2021) investigate the impact of a corporate governance index on financial performance—more specifically, return on assets, general liquidity, capital adequacy, and size of company in the banking sector. Similarly, Mishra et al. (2021) study the empirical relationship between corporate governance, on one side, and market-based performance measures of firms (such as Tobin’s Q) and accounting-based performance measures (such as return on assets), on the other. López-Quesada et al. (2018), using a corporate governance index, find that good corporate governance increases a measure of firms’ financial performance—namely, comprehensive income. Table 1 summarizes the most important studies focused on corporate governance indices.

Table 1. Summary of literature on corporate governance indices

This table provides a summary description of the most remarkable studies on corporate governance indices.

| Author | Title | Country Data/Scope | Summary |

|---|---|---|---|

| Gompers et al. (2003) | Corporate Governance and Equity Prices | US firms | Develops a broad index of governance rules tracked by the Investor Responsibility Research Center (IRRC). Most of the governance features tracked by the IRRC are defensive tactics. The features consist of provisions in firms’ corporate documents and types of state takeover statutes, resulting in a total of distinct items included in the construction of the index. The index is negatively correlated with firm value, measured by Tobin’s Q. An investment strategy that bought firms in the lowest decile of the index (strongest rights) and sold firms in the highest decile of the index (weakest rights) would have earned abnormal returns of 8.5% per year during the sample period. Firms with stronger shareholder rights had higher firm value, profits, and sales growth but lower capital expenditures, and they made fewer corporate acquisitions. |

| Klapper & Love (2004) | Corporate Governance, Investor Protection, and Performance in Emerging Markets | Firms from twenty-five emerging markets | The empirical tests show that better corporate governance is highly correlated with better operating performance and market valuation. Although the study does not deal specifically with the design of a corporate governance index, it uses a ranking of corporate governance. This ranking, compiled by Credit Lyonnais Securities Asia, is a composite of fifty-seven qualitative, binary (yes/no) questions. The paper shows that firm-level governance and performance (market valuation measured by return on assets and Tobin’s Q) are lower in countries with weak legal environments, suggesting that improving the legal system should remain a priority for policy makers. |

| Bebchuk & Cohen (2005) | The Costs of Entrenched Boards | US firms | The study designs an index based on six factors selected from twenty-four governance factors developed by , whose index is built upon the information provided by the IRRC. index is accepted as the best explanation of result that corporate governance is positively associated with firm’s performance. Among the major findings, the authors highlight that the correlation with reduced firm value (measured by Tobin’s Q) is stronger for staggered boards that are established in the corporate charter (which shareholders cannot amend) than for staggered boards established in the company’s bylaws (which shareholders can amend). The authors conclude that their index outperforms that of , as it is more parsimonious and better motivated. |

| Black et al. (2006) | Predicting Firms’ Corporate Governance Choices: Evidence from Korea | Korean firms | The authors construct a corporate governance index for companies listed on the Korean Stock Exchange, composed of governance elements, divided into five equally weighted subindices that characterize shareholder rights, board structure, board procedures, disclosure, and ownership parity. The most important finding is that regulatory factors are highly important as determinants of firms’ corporate governance practices. Regarding the firm-level variables, the findings indicate that larger firms are better governed than smaller firms and that riskier companies are also better governed than conservative firms. Additionally, long-term averages of profitability and equity-finance need are significant drivers of governance, while short-term averages are not. This is consistent with sticky governance, in which firms alter their governance slowly in response to economic factors. |

| Beiner et al. (2006) | An Integrated Framework of Corporate Governance and Firm Valuation | Swiss firms | The study is focused on the relationship between the quality of firm-specific corporate governance and firm valuation. The most important variables included in the index are ownership structure, board characteristics, and leverage. The results support the widespread hypothesis of a positive relationship between corporate governance and firm valuation. |

| Brown & Caylor (2006) | Corporate Governance and Firm Valuation | US firms | The authors create a more comprehensive corporate governance index than and based on firm-level information obtained from Institutional Shareholder Services. The authors’ index is based on the sum of factors. They highlight that their index has the potential advantage of providing a superior measure of a firm’s governance quality because (i) it incorporates a set of components of governance defense not considered in previous studies, (ii) it is broader in scope of governance, (iii) it covers more firms, and (iv) it is more dynamic than previous governance indices. The results show that only a small subset of provisions marketed by corporate governance data providers are related to firm valuation and that both internal and external governance are linked to firm value. |

| Chen et al. (2007) | Building a Corporate Governance Index from the Perspectives of Ownership and Leadership for Firms in Taiwan | Taiwanese firms | The paper tests the relationship between ownership/leadership structures and stock returns for listed firms. A governance index is built based upon CEO duality, size of the board of directors, management’s holdings, and block shareholders’ holdings. The major findings imply that well-governed firms should outperform those with poor governance and that the index successfully evaluates the effectiveness of the governance mechanism of firms in Taiwan. |

| Cheung et al. (2007) | Do Investors Really Value Corporate Governance? Evidence from the Hong Kong Market | Hong Kong firms | The created corporate governance index reflects the presence of good corporate governance practices and variation in the quality of those practices. The study’s empirical evidence shows that a company’s market valuation is positively related to its overall corporate governance index score, a composite measure of a firm’s corporate governance practices. The authors also find that the transparency component of the index score drives the relation with market valuation. |

| Larcker et al. (2007) | Corporate Governance, Accounting Outcomes, and Organizational Performance | US firms | The study is based on thirty-nine structural measures of corporate governance (for example, board characteristics, stock ownership, institutional ownership, activist stock ownership, existence of debtholders, mix of executive compensation, and anti‐takeover variables). The study finds that its diverse corporate governance indices have a mixed association with abnormal accruals, little relation to accounting restatements, but some ability to explain future operating performance and future excess stock returns. |

| Aman & Nguyen (2008) | Do Stock Prices Reflect the Corporate Governance Quality of Japanese Firms? | Japanese firms | The authors use new corporate governance information from Nikkei CGES to identify attributes that impact agency problems and thus are associated with governance features. These attributes include board composition, ownership structure, and investor rights. The main finding is that after adjusting for firm size and book-to-market ratio, poorly governed firms significantly outperform better-governed firms. The authors show that neither the sample period nor the behavior of specific industries is responsible for this outcome. Consistent with market efficiency, stock prices appear to reflect the higher (lower) risk associated with poor (good) corporate governance. |

| Bhagal et al. (2008) | The Promise and Peril of Corporate Governance Indices | Critical discussion of previous literature on corporate governance indices | The study analyzes the effectiveness of corporate governance indices in predicting corporate performance and assesses the implications for policy makers. The most prominent contribution of this work is its identification of major methodological shortcomings of the studies that claim to have identified a causal relationship between governance measures and corporate performance. Indeed, the study concludes that there is no consistent relationship between governance and performance and that there is no single best measure of corporate governance. The authors claim that “the most effective governance system depends on context and on firms’ specific circumstances.” Their criticism of corporate governance indices concerns factors such as boards of directors, shareholder franchise and block ownership, and executive compensation. |

| Brown & Caylor (2009) | Corporate Governance and Firm Operating Performance | US firms | Based on the authors’ preliminary work but using a broader index based on the governance provisions mandated by the three major US stock exchanges, the study confirms that corporate governance is positively correlated with operating performance, market valuation, and dividend pay-out ratio for a large sample of US firms. Six corporate governance provisions are significantly and positively linked to return on assets, return on equity, or both. The results reveal that the governance provisions mandated in 2002 by the stock exchanges are less closely linked to firm operating performance than are those not mandated. |

| Black et al. (2010) | Corporate Governance in Brazil | Brazilian firms | The study’s governance metric is based on an extensive survey distributed to all firms listed on BOVESPA, Brazil’s principal stock exchange. The survey includes information on board composition, board procedures, oversight of financial reporting, shareholder meetings and shareholder rights, related-party transactions and executive compensation, disclosure, and control and shareholder agreements. Such detailed information allows the authors to identify areas in which Brazilian corporate governance is relatively strong or weak and areas in which regulation might usefully be weakened or strengthened. For instance, the authors highlight that board independence and financial disclosure are areas of notable weakness in corporate governance in Brazil. |

| Cheung et al. (2011) | Does Corporate Governance Predict Future Performance? | Hong Kong firms | The authors’ metric of governance is based on a scorecard built upon the five principles of corporate governance developed by the OECD. The scorecard items are modified to accommodate the codes of best practice applicable in Hong Kong. The criteria for the index are grouped in sections replicating the OECD principles. The empirical results show that firms that exhibit improvements in the quality of corporate governance see a subsequent increase in market valuation as measured by Tobin’s Q and market-to-book value. The authors state that firms whose quality of corporate governance practices deteriorates in one period tend to see a decline in market valuation in the next. The impact is stronger for firms that are included in the middle- and small-cap index and firms that are related to China. |

| Ammann et al. (2011) | Corporate Governance and Firm Value: International Evidence | Publicly listed firms from twenty-two developed countries | The authors are pioneers in using a large data set from Governance Metrics International to build two additive corporate governance indices with equal weights based upon firm-level governance attributes. They also create one index derived using principal component analysis. For all three indices the authors find a strong and direct relation between firm-level corporate governance and firm valuation, as observed in previous empirical studies. In addition, the authors study the value relevance of governance attributes that characterize companies’ social behavior (identified with corporate social responsibility). The study also expands the panel used in international studies. The findings indicate a positive and significant effect on firm value, even after controlling for individual and aggregated governance attributes. |

| Balasubramanian et al. (2010) | The Relation between Firm-Level Corporate Governance and Market Value: A Case Study of India | Indian firms | The study constructs a broad Indian Corporate Governance Index based on an extensive survey of publicly listed companies. The authors find a positive and statistically significant association between their suggested index and firms’ market value. The association is more significant for more profitable firms and firms with greater growth opportunities. A subindex for shareholder rights is statistically significant, but subindices for board structure, disclosure, board procedure, and related-party transactions are not. Contrary to some other works, the study does not find statistically significant results for board-structure features, suggesting that India’s legal requirements are sufficiently strict. This finding indicates that overcompliance with the legal framework does not imply higher firm valuation. |

| Kaufmann et al. (2011) | The Worldwide Governance Indicators: Methodology and Analytical Issues | Over countries | This paper summarizes the methodology of the Worldwide Governance Indicators project and related analytical issues undertaken by the World Bank, organizing the index in six aggregate governance indicators: (i) voice and accountability, (ii) political stability, (iii) government effectiveness, (iv) regulatory quality, (v) rule of law, and (vi) control of corruption. Multiple underlying variables from many data sources are used to build these indicators, allowing for meaningful cross-country and over-time comparisons. |

| Black et al. (2012) | What Matters and for Which Firms for Corporate Governance in Emerging Markets? | Brazilian firms | The study provides strong evidence that corporate governance quality depends on country- and firm-specific features in line with . The authors construct an index of governance for the Brazilian corporate sector. The metric is based on subindices for ownership structure, board structure, and minority shareholder rights. The authors extend prior studies conducted in emerging markets to compare those studies’ results with those for Brazil. The index and its subindices predict higher lagged values for Tobin’s Q as a measure of firms’ value. Unlike other studies, however, this one finds that greater board independence predicts lower Tobin’s Q. Firm characteristics also matter; for instance, governance predicts market value for nonmanufacturing (but not manufacturing) firms, small (but not large) firms, and high-growth (but not low-growth) firms. Regarding policy implications, the findings of the study are not consistent with some mandatory minimum rules on adding corporate value. |

| Ammann et al. (2013) | Product Market Competition, Corporate Governance, and Firm Value: Evidence from the EU Area | Companies from fourteen EU countries | The authors examine whether the valuation effect of corporate governance depends on the degree of competition in companies’ product market. They claim that previous studies are plagued with measurement problems regarding both corporate governance and market competition. The authors’ corporate governance index is based on sixty-four governance attributes obtained from Governance Metrics International, similarly to their own previous study . As a robustness test of their findings, the authors use an alternative version of this index that excludes attributes in place at more than or less than 10% of the sample firms. The degree of market competition is measured with a Herfindahl-Hirschman index. The major findings of the study indicate that the corporate governance is positively associated with firm value in noncompetitive markets only, which is consistent with the hypothesis that product-market competition acts as a substitute for governance. |

| Kocmanová & Šimberová (2014) | Determination of Environmental, Social and Corporate Governance Indicators | Czech firms | The article contributes to the effort to measure corporate sustainability and proposes a conceptual framework of ESG performance indicators for the Sustainability Reporting of Czech companies operating in the processing industry. The results of factor analysis indicate that the factors fall into three measurement categories: environmental, social, and corporate governance. |

| Nerantzidis (2016) | A Multi-methodology on Building a Corporate Governance Index from the Perspectives of Academics and Practitioners for Firms in Greece | Greek firms | The goal of the study is to shed light on how to construct an efficient, reliable, and valid index of corporate governance. The value of the study lies in an improved understanding of the methodological issues in constructing corporate governance indices. The authors discuss how to measure corporate governance, the main criteria used in index construction, and the previous literature on corporate governance indices. The study expands our theoretical understanding of corporate governance index development by using the Delphi method, classical test theory, and analytic hierarchy process. |

| Ararat et al. (2017) | The Effect of Corporate Governance on Firm Value and Profitability: Time-Series Evidence from Turkey | Turkish firms | A Turkey Corporate Governance Index (TCGI) is developed that is composed of subindices for board structure, board procedure, disclosure, ownership, and shareholder rights. The TCGI predicts higher market value with firm fixed effects and higher firm-level profitability with firm random effects. The principal subindex that predicts higher market value and profitability and drives the results for the TCGI as a whole is the disclosure subindex. |

| Black et al. (2017) | Corporate Governance Indices and Construct Validity | Firms from emerging markets (Brazil, India, Korea, and Turkey) | The authors exhaustively analyze how to test the validity of a firm-level corporate governance index. They argue that uncertain construct validity of most corporate governance indices suggests caution in relying on research using these indices as a basis for firm-level governance changes or country-level legal reforms. Hence, they build country-specific indices based on country-specific governance elements that reflect local norms, institutions, and data availability, and they show that these indices predict firm market value in each country after conducting the construct-validity process. |

| Karpoff et al. (2017) | Do Takeover Defense Indices Measure Takeover Deterrence? | US firms | The authors go beyond and indices of governance by supplying an instrument version of these indices that is significantly and inversely related to firms’ takeover likelihood. The authors highlight the flaws of previously constructed corporate governance indices in measuring a firm’s takeover defense and in handling the potential endogeneity problems in constructing the index. Using simple tests that account for endogeneity, the authors do not find significant evidence that previous corporate governance indices are able to measure takeover likelihood. However, once endogeneity is considered, the authors find that previous popular indices are negatively associated with takeover likelihood. Concerns about the endogeneity issues in previous indices calls for the use of coverage antitakeover laws to control for the lack of causality in the construction of governance indices. |

| López-Quesada et al. (2018) | Corporate Governance Practices and Comprehensive Income | US firms | This paper analyzes the effect of corporate governance practices on firms’ financial performance. High levels of corporate governance culture, measured with an index composed of inputs such as board size, outside directors, board duality, board meetings, and CEO compensation, has a positive impact on firms’ financial performance measures such as return on assets, return on equity, and return on investment and on an innovative measure named Comprehensive Income. The results indicate a positive correlation between the percentage of outside directors and financial performance and a negative one between the number of board meetings and financial performance. The main contribution is to show that good corporate governance strategies deliver superior financial performance for businesses in terms of Comprehensive Income. |

| Black et al. (2020) | Which Aspects of Corporate Governance Do and Do Not Matter in Emerging Markets | Firms from merging markets (Brazil, India, Korea, and Turkey) | This study builds country-specific governance indices comprising indices for disclosure, board structure, ownership structure, shareholder rights, board procedure, and control of related-party transactions. Disclosure (especially financial disclosure) predicts higher market value across all four studied countries. Board structure (principally board independence) has a positive coefficient in all countries and is significant in two countries. The other indices do not predict firm value. These results suggest that regulators and investors, in assessing governance, and firm managers, in responding to investor pressure for better governance, would do well to focus on disclosure and board structure. |

| Elmagrhi et al. (2020) | Corporate Governance Disclosure Index–Executive Pay Nexus: The Moderating Effect of Governance Mechanisms | UK firms | The study uses the PCA technique to construct an alternative UK corporate governance index that comprises 31 out of 120 comprehensive governance provisions included in the UK Combined Code. In this sense, this index differs substantially from US-centered ones. Unlike indexes in previous empirical studies, this index allows researchers to capture the qualitative differences in governance structures across firms. The study assesses whether governance systems moderate payment of those in senior positions of UK firms. The most important findings suggest that better-governed firms tend to pay their executives less compared with their poorly governed counterparts. Pay-for-performance sensitivity is generally positive but improves in firms that exhibit high internal corporate governance quality. |

| Mishra et al. (2021) | Does Corporate Governance Characteristics Influence Firm Performance in India? | Indian firms | The study examines the empirical relationship between a suggested corporate governance index (for example, characteristics of board structure, ownership structure, director participation and busyness, market for external control, and product-market competition) and firms’ financial performance. The authors use internal and external corporate governance data to construct their index. They use the generalized method of moments to overcome the endogeneity and simultaneity biases observed in the construction of other corporate governance indices. The result shows a significant positive impact of the suggested index on firms’ return on assets and return on net wealth, but such relations are negative with Tobin’s Q. |

| Benvenuto et al. (2021) | Assessing the Impact of Corporate Governance Index on Financial Performance in the Romanian and Italian Banking Systems | Romanian banks | The research question is how a modification in corporate governance legislation influences two different banking systems. Corporate governance has a significant, positive, and long-lasting effect on profitability and capital adequacy in both Romania and Italy. Taking the size of companies into consideration, the impact of the Index of Corporate Governance on a homogenous banking system is positive, while the impact on a heterogeneous banking system is negative. The corporate governance principles applied do not encourage the growth of large banks in heterogeneous banking sectors. |

| Nsour & Al-Rjoub (2022) | Building a Corporate Governance Index (JCGI) for an Emerging Market: Case of Jordan | Jordanian firms | The study develops the first Jordan Corporate Governance Index, comprising five subindices: board structure, board procedure, disclosure, ownership structure, and minority-shareholder rights. The results show that Jordanian companies did not progress in corporate governance during the study period. |

| Nasrallah & El Khoury (2022) | Is Corporate Governance a Good Predictor of SMEs’ Financial Performance? Evidence from Developing Countries (the Case of Lebanon) | Small and medium Lebanese enterprises | Using a questionnaire to collect data on corporate governance and applying the bundles approach, the authors construct a corporate governance score based on (i) the characteristics of an efficient management board, (ii) the credibility and accounting of internal control and external audit, and (iii) the features of sound operational practices. Unlike previous studies, the study applies two-stage least-squares regression estimates to deal with endogeneity concerns. The paper studies the impact of the suggested corporate governance score and each of its components on financial performance measured by return on assets and return on investment. The study finds a positive interdependency between the governance index and different metrics of financial performance. |

This study intends to overcome the major limitations of index construction highlighted above and conducts a subsequent test of validity by incorporating multidimensional internal characteristics of corporate governance in a single institutional context. Hence, the governance index developed in subsequent sections includes four dimensions corresponding to the degree to which a corporation complies with codes of good governance, features of boards of directors, ownership-structure features, and transparency in financial reporting. After constructing the corporate governance index, we validate the construct by applying multiple suitable measures of firm value.

The hypotheses we test are as follows:

H1: The components of the subindices of corporate governance considered in this study capture internal coherence as metric of corporate governance.

H2: The components of the comprehensive index of corporate governance considered in this study capture internal coherence as metrics of corporate governance.

H3: In the construction-validity process, the subindices of corporate governance explain firm value.

H4: In the construction-validity process, the comprehensive Spanish corporate governance index explains firm value.

3. Methodology

3.1. Comprehensive corporate governance index and its construct validity

3.1.1. Cronbach’s \(\mathbf{\alpha}\)

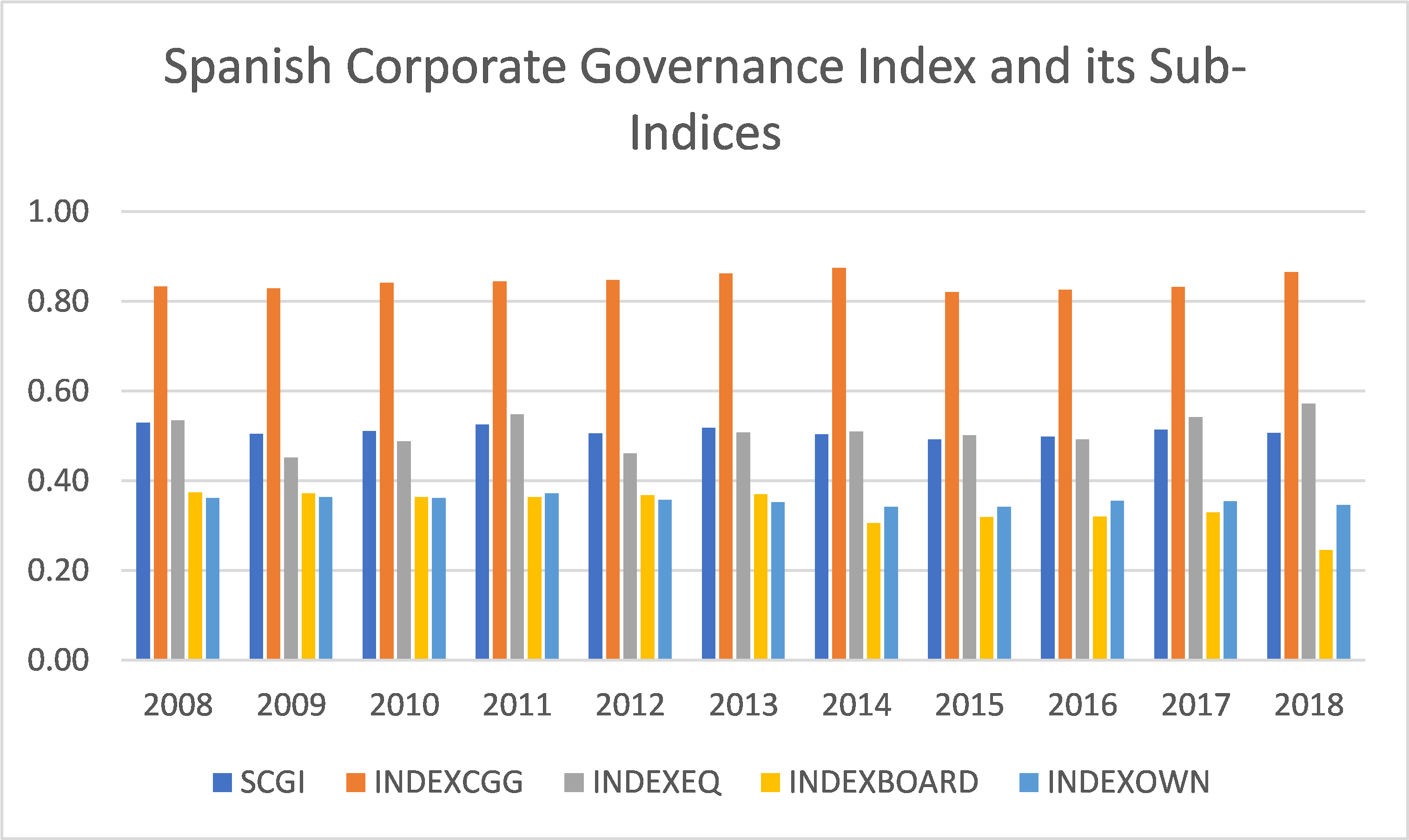

The subindices of our corporate governance index for Spanish firms (S-CGI) are degree of compliance with Spanish codes of good governance \(\left( IndexCGG \right)\), the features of boards of directors \(\left( IndexBOARD \right)\), ownership-structure features \(\left( IndexOWN \right)\), and transparency of financial reporting \(\left( IndexEQ \right)\)2. Every subindex is divided into several subcomponents. Since it is not easy to determine which components are relevant for each subindex, we use Cronbach (1951) \(\alpha\) to measure the scaled inter-subindex correlation—in other words, the internal consistency of the scale. The major advantages of \(\alpha\) are that it represents the average of all possible split halves for a set of items and that it can be used for dummies and, as in this study, for continuous scored variables3,4. The coefficient runs from 0 to 1—from no consistency in the measurement to perfect internal consistency. According to Black et al. (2017), if the components of every element of an index contribute to a measure of the same general aspect of governance, then \(\alpha\) is expected to be reasonably high, meaning that the components are highly correlated. Conversely, if the components capture distinct elements of corporate governance, \(\alpha\) should be moderate or low.

The rule of thumb in psychology is that a coefficient value above 0.7 is strong. A value above 0.6 is usually considered acceptable, and values below that threshold indicate relatively poor reliability in the measurement5. The coefficient is estimated as

\[\begin{equation} \label{eq1} \alpha = \frac{k\overline{r}}{\left( 1 + \left( k - 1 \right)\overline{r} \right)} \ \ \ \ \ (1) \end{equation}\]where \(k\) represents the number of components in each subindex of S-CGI and \(\overline{r}\) is the mean intercomponent correlation. The coefficient \(\alpha\) is highly sensitive to the number of components included in the corporate governance subindex, and there is a positive, nonlinear relationship between the number of components and the reliability. The important assumptions in calculating \(\alpha\) are, first, that it features intrinsic unidimensionality, meaning that the components of the subindices are single dimensions of corporate governance, and second, that the error terms of the components are uncorrelated.

3.1.2. Principal component analysis

In addition to Cronbach (1951) \(\alpha\), we also adopt PCA to validate the construct of the corporate governance index. PCA is a statistical technique aiming to create a condensed number of index variables from a larger set of measured variables (Aydin et al., 2019), which in our case are the components of the subindices in S-CGI. It does this using a weighted-average linear combination of the set of input variables. The created index variables are referred to as factors. The point of PCA is to determine the optimal number of components, the optimal choice of measured variables for each component, and the optimal weights of the measures (Khongmalai et al., 2010).

One of the major advantages of this technique is that the information in each data set corresponds to the data set’s total variation (Dray, 2008). The goal of PCA is to identify directions (or principal factors) in which the variation in the data is maximal (Florackis & Palotás, 2010). In other words, PCA reduces the dimensionality of a multivariate data set to two or three uncorrelated principal factors that can be identified with minimal loss of information.

3.1.3. Additive indices

We use additive indices to sum the normalized subindices. The general guidelines provided by Mazziotta & Pareto (2013) for constructing composite indices suggest using an additive index if the components of a composite index are substitutable—that is, if a deficit in one component may be compensated by a surplus in another. For instance, low gender diversity on a board of directors might be offset with a high proportion of independent, external board members, and vice versa. In such situations, a compensatory approach can be found that involves the use of additive methods, such as the arithmetic mean, as in this study, Ammann et al. (2011), and Ammann et al. (2013). This technique is common (see, for instance, Gompers et al. (2003), Bebchuk & Cohen (2005), Brown & Caylor (2006), and more recently Ararat et al. (2017) and Black et al. (2017)).

3.1.4. Panel-data approach for regression analysis

The last step in the construct-validation process is to assess the power of S-CGI as an input variable to explain firm value as an output variable. To do so, we use panel-data regression analysis. Given that the Spanish companies we study are observed during several years, we can form panel microstructures, or combinations of cross-sectional information (on individual firms) with time-series information. Panel-data analysis allows us to tackle the individual-heterogeneity issues typically observed in the corporate governance literature (Gormley & Matsa, 2014). Indeed, Gormley & Matsa (2014) state that controlling for unobserved heterogeneity is fundamental in empirical finance research because asset prices and most corporate policies depend on factors that are unobservable to the econometrician but must be considered in the analysis. Constant and unobservable heterogeneity refers to factors that are invariant over time (differences in firms’ economic environments, internal long-term corporate strategies, managerial styles, attitudes toward risk, and internal policies, to name a few). If these factors are correlated with the variables of interest, and if the individual and unobservable effect is not properly treated, the results can lead to biased estimations of parameters (Gormley & Matsa, 2014).

In addition to the unobservable-heterogeneity problem, there is the endogeneity (or simultaneity) problem, which is quite common in corporate governance, finance, and accounting studies (Gippel et al., 2015; Roberts & Whited, 2013; Wintoki et al., 2012). This problem occurs when the direction of causality is unclear between internal corporate governance systems and proxies for firm value (Wintoki et al., 2012). In other words, simultaneity bias occurs when the dependent variable and one or more of the independent variables are determined in equilibrium so that it can plausibly be argued either that the independent variables cause the dependent one or that the dependent variable causes the independent variables. Consequently, when the endogeneity issue is ignored, the results are at the very least incomplete.

We follow Saona et al. (2020) in applying the two-stage generalized-method-of-moments system estimator (GMM-SE), which overcomes both the unobservable-heterogeneity and endogeneity problems by using as instruments lagged right-hand-side variables (Alonso-Borrego & Arellano, 1999). We also employ the unobservable fixed-effects (FE) method as a robustness check of the major findings.

3.2. Construction of variables

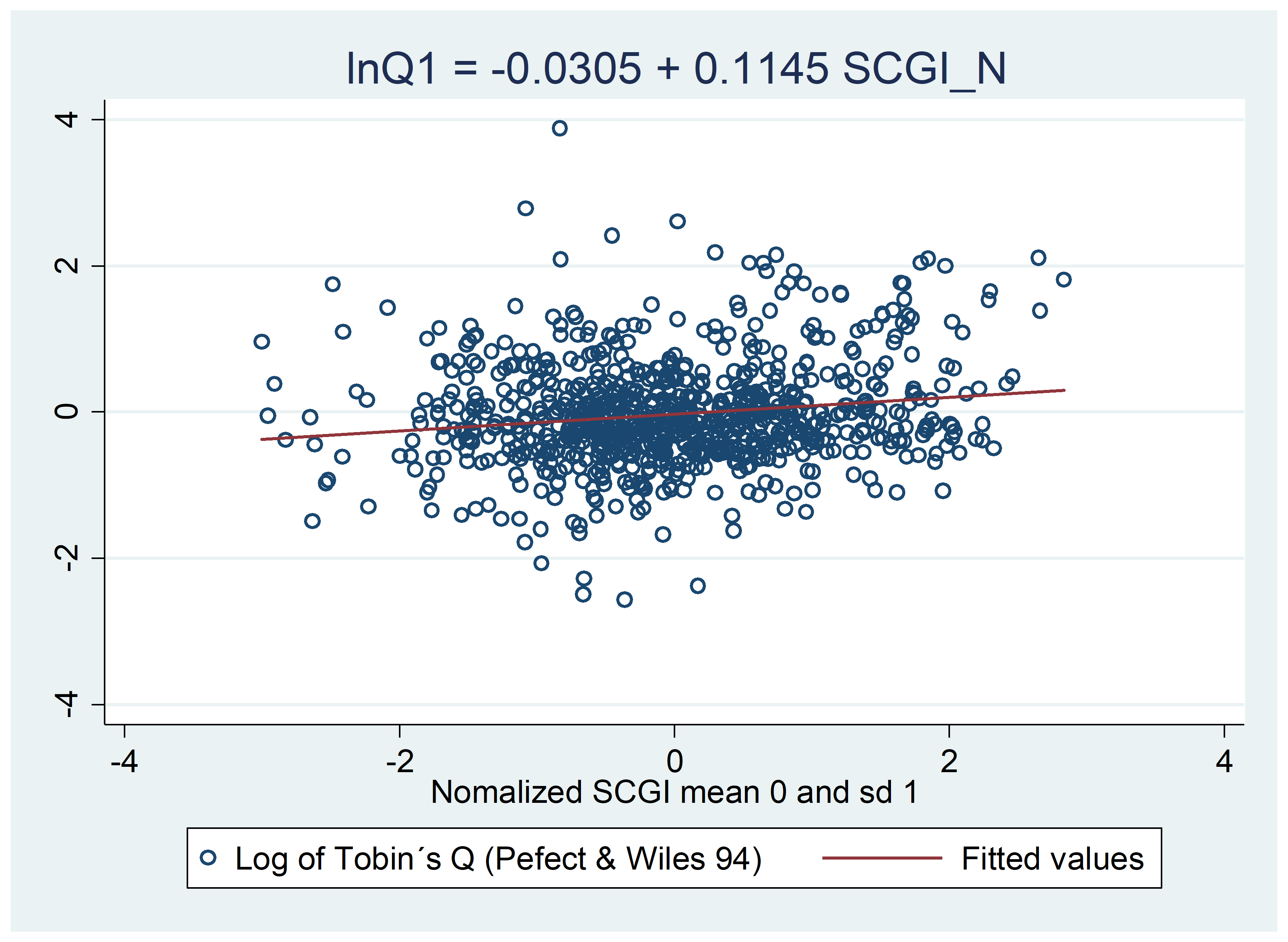

We use firm value as the dependent variable for checking construct validity. In most of the empirical literature, Tobin’s Q is used as a proxy for firm value, which is a common outcome variable in governance studies (Chung & Pruitt, 1994; Lindenberg & Ross, 1981; Lozano et al., 2016; Setia-Atmaja, 2009; Smirlock et al., 1984). Tobin’s Q can be used to measure the value added to a firm by corporate governance because investors ascribe higher value to assets as corporate governance practices improve (Black et al., 2017).

The theoretical definition of Tobin’s Q is the ratio of the market value of a firm to the replacement cost of its assets. Although often criticized, its simplified version—the ratio of the market value to the book value of total assets—is widely accepted in the literature (Adam & Goyal, 2008; Smirlock et al., 1984) 6. One of the firm-value literature’s major flaws regarding validity is that measuring firm value with Tobin’s Q produces inaccuracy, bias, and variability. Thus, although the measure boasts simplicity of computation, it has major disadvantages. As recently suggested by Barlett & Partnoy (2020), Tobin’s Q has been one of the most important concepts for examining how various regulatory and corporate governance provisions affect firm value and therefore economic welfare. As originally conceived, Tobin’s Q, named for the economist James Tobin, was an important variable in macroeconomic theory; it was defined as the market value of a firm’s assets divided by their replacement value. Within macroeconomics, it was originally viewed as a means to understand corporate investment policy. To mitigate the risk of misspecification of such a critical variable in the model specification of the construct-validity process, we follow an approach based on Perfect & Wiles (1994), Pindado et al., (2010), and Saona (2014) in which the Tobin’s Q proxy is computed based on the reposition cost of total assets in addition to the popular market-to-book-based ratios.

Hence, our first measure of firm value \(\left( Q1 \right)\) is defined as \(Q1 = \left( MkCptz_{it} + TD_{it} \right)/K_{it}\), where \(MkCptz_{it}\) is a firm’s market capitalization (computed as the product of the year-end closing price per share and the number of shares outstanding for firm \(i\)). \(TD_{it}\) is total liabilities in year \(t\). \(K_{it}\) is the replacement value of the firm’s assets, which is estimated in Perfect & Wiles (1994) as \(K_{it} = RNP_{it} + RINV_{it} + (TA_{it} - BNP_{it} - BINV_{it})\), where \(RNP_{it}\) is the replacement cost of net property, plant, and equipment (net fixed assets); \(RINV_{it}\) is the replacement value of inventory; \(TA_{it}\) is total assets; \(BNP_{it}\) is the book value of net property, plant, and equipment; and \(BINV_{it}\) is the book value of inventory.

\(RNP_{it} = RNP_{it - 1}\left\lbrack \frac{1 + \phi_{t}}{1 + \delta_{it}} \right\rbrack\)+\(I_{it}\) for \(t > t_{0}\), where \(t_{0}\) is the first year of observations for a given company in this study, while \(RNP_{it_{0}} = BNP_{it_{0}}\). Meanwhile, \(\phi_{t}\) is the growth of capital-goods prices in year \(t\) as defined by the gross domestic product (GDP) deflator. In other words, \(\phi_{t} = \frac{NomGDP_{t}}{RealGDP_{t}}100\), where \(NomGDP_{t}\) is nominal GDP and \(RealGDP_{t}\) is real GDP, both reported by the National Institute of Statistics of Spain. \(\delta_{it}\) is the real depreciation rate, defined as \(\delta_{it} = \frac{Dep_{it}}{BNP_{it}}\) , where \(Dep_{it}\) is annual book depreciation.

\(I_{it}\) is new investment in property, plant, and equipment and is defined as \(I_{it} = BNP_{it} - BNP_{it - 1} + Dep_{it}\).

\(RINV_{it} = BINV_{it}\left\lbrack \frac{{2WPI}_{t}}{WPI_{t} + WPI_{t - 1}} \right\rbrack\), where \(WPI_{t}\) is the wholesale price index reported by the National Institute of Statistics of Spain. This estimation for the replacement value of inventory assumes that the inventory-accounting method is average cost. In this method, the value of inventory reported at time \(t\) is approximately equal to the average of the prices at \(t - 1\) and \(t\).

The second measure of firm value \(\left( Q2 \right)\) is based on enterprise value \((EV_{it})\) according to Łudzińska (2017), which is the sum of market capitalization \(\left( MkCptz_{it} \right)\), total debt \(\left( TD_{it} \right)\), preferred stock \(\left( PrefStock_{it} \right)\), and minority interest \(\left( MinInt_{it} \right)\) minus cash and short-term investments \(\left( CashEquiv_{it} \right)\). Enterprise value is scaled by the replacement value of the firm’s assets \(\left( K_{it} \right)\), following Perfect & Wiles (1994). Therefore, \(Q2 = EV_{it}/K_{it}\). The third measure of firm value \((Q3)\) is market capitalization \(\left( MkCptz_{it} \right)\) plus total debt \(\left( TD_{it} \right)\), all over the book value of total assets, based upon Goyal et al. (2002), Maury & Pajuste (2005), and Saona & San Martín (2018): \(Q3 = \left( MkCptz_{it} + TD_{it} \right)/TA_{it}\). The fourth measure of firm value \((Q4)\) is the quotient between enterprise value and book value of total assets (Łudzińska, 2017): \(Q4 = EV_{it}/TA_{it}\).

Hence, the econometric model takes the following form:

\[\begin{equation} \label{eq2} Q_{it} = \beta_{0} + \beta_{1}SCGI_{it - 1} + \beta_{2}X_{it}^{'} + \mu_{i} + \epsilon_{t} + \varepsilon_{it} \ \ \ \ \ (2) \end{equation}\]The output variable \(Q_{it}\) is any of the alternative measures of firm value defined above. In constructing the dependent variable, market capitalization is in the nominator, which might lead to large variation of the variable. Hence, to minimize the impact of outliers and to normalize the distribution of the covariates, we also use as a dependent variable in model (2) the natural logarithmic transformation of the various metrics of firm value defined above. Consequently, in these cases, \(\beta_{1}\) and \(\beta_{2}\) must be interpreted as partial elasticities: the percentage change in firm value caused by a unit change in any of the right-hand-side variables included in equation (2). Additionally, \(SCGI_{it}\) corresponds to either S-CGI or any of its subindices (namely, features of the board of directors, ownership-structure features, degree of compliance with codes of good governance, and transparency in financial reporting).

Additionally, to prevent misspecification problems, we enter in the model the vector \(X_{it}^{'}\), which incorporates exogenous firm-level control covariates typically used in the literature (Kocmanová & Šimberová, 2014). This vector includes \(ROA_{it}\), a measure of profitability computed as net income over total assets (Singh & Gaur, 2009); leverage \(\left( Lev_{it} \right)\), defined as total debt as a share of total assets (Harris & Raviv, 1990; Saona & Vallelado, 2012); and the firm’s capital expenditure \(\left( CAPEX_{it} \right)\), which represents the sum of purchases of fixed assets, acquisitions of intangible assets, and software-development costs (Rosenblatt & Jucker, 1979) 7. Firm size \(\left( Size_{it} \right)\) is also used as a control variable and is defined as the logarithmic transformation of the firm’s total assets (Beck et al., 2008; Dennis & Sharpe, 2005). Additionally, dummy variables that identify the industry sector are introduced in the analysis. Finally, \(\mu_{i}\), \(\epsilon_{t}\), and \(\varepsilon_{it}\) represent the individual fixed effect, the time-series fixed effect, and the stochastic error, respectively.

To mitigate potential biases resulting from outliers, variables are winsorized at the 1% level in the lower and upper tails when appropriate as in previous studies (Jara et al., 2019; Mellado & Saona, 2020).

The subindices of S-CGI are defined based on the following covariates.

Degree of compliance with codes of good governance (IndexCGG): As we explained earlier, codes of good governance play an essential role in aligning a company’s governance with the external regulatory framework (Aguilera & Cuervo-Cazurra, 2009). Following the main arguments of Aguilera & Cuervo-Cazurra (2004), the degree of compliance with these codes is measured by answers to thirty-one questions regarding Spanish firms’ compliance with codes of good governance. The answers are provided in four points on a Likert scale. The questions are listed in the appendix. We use PCA and the additive-indices technique as alternative approaches to create a subindex from these thirty-one components. Afterward, the subindex is normalized to have a mean of 0 and a standard deviation equal to 1.

Assidi (2020), Renders & Gaeremynck (2012), and Outa & Waweru (2016), among other authors, have found a positive relationship between corporate governance compliance and firm value in institutional contexts such as France, Indonesia, and Kenya. Consequently, we expect that Spanish companies with high compliance with the Spanish \(SCGI_{it}\) will experience greater firm value.

Features of board of directors (IndexBOARD): We consider it fundamental to include board-of-directors characteristics because of their importance in control and supervision (Saona et al., 2020). These characteristics play a key role in reducing agency costs and in improving the effectiveness of corporate governance (Frias-Aceituno et al., 2013). According to the empirical literature—see, for instance, Baysinger & Butler (1985), Forbes & Milliken (1999), Klein (2002), de Cabo et al., (2012), Kumar & Zattoni (2014), Fernández-Gago et al., (2016), Birindelli et al., (2018), Arzubiaga et al., (2018), and Lidia & Patricia (2018)—the most influential board variables are percentage of the firm’s capital represented by directors’ stock options, percentage of directors on the boards of other companies, percentage of independent directors on the audit committee, percentage of independent directors on the executive committee, percentage of independent directors on the nomination committee, whether the board secretary monitors the good-governance recommendations, whether an executive committee exists, whether directors receive external advice, percentage of the firm’s owners (weighted by capital) attending the firm’s general meetings, percentage of independent directors, percentage of total directors on the audit committee, percentage of total directors on the executive committee, percentage of total directors on the nomination committee, restrictions on the exercise of voting rights, whether the secretary is a board member, whether there is separation of powers between the board chair and the chief executive, whether there are specific requirements for being board chair, whether there is a supermajority voting rule, whether there is a policy of tenure for independent directors, whether there is a policy regarding time to prepare a board meeting, and number of female board members.

Researchers have found various relationships between these features and firm value. For instance, Pucheta-Martínez et al., (2018) report that female institutional directors increase firm value, with an inverse-U-shaped relationship at the threshold of 11.72% of female members in the board of Spanish companies. Vitolla et al. (2020) find a positive relationship between the size, independence, diversity, and activity of a board with integrated reporting quality. Fernández-Gago et al. (2016) find positive relationships between, on the one side, small boards, boards with many women, and boards with more independent members and, on the other side, firm value. Kao et al., (2019) show an increase in the value of Taiwanese firms with a high proportion of independent directors, a smaller board size, a two-tier board system, and no CEO duality. Fich & Shivdasani (2005) find a positive relationship between stock-option plans and firm value.

From our analysis we can see that the characteristics of the board play a fundamental role as a corporate governance mechanism; consequently, improvements in them will increase the value of firms.

Ownership-structure features (IndexOWN): Spain belongs to the group of civil-law countries which are characterized by concentrated ownership structures in its companies. Different ownership-structure attributes provide different incentives to control a firm’s management (Ang et al., 2000; Jensen & Meckling, 1976; Morck et al., 1988; Shleifer & Vishny, 1986), and consequently affect the corporate governance of the firm. Firms’ ownership structure, viewed as a governance device, is also measured by several variables. We measure the institutional nature of the majority shareholder with a dummy variable (Azofra et al., 2003). Additionally, following the existing literature (Bozec & Bozec, 2007; Lefort & Urzúa, 2008; Saona & San Martín, 2016; Saona et al., 2018; Setia-Atmaja, 2009), we use ownership concentration, measured alternatively as the percentage of capital held by the majority shareholder, the ownership held by the ten largest shareholders, the ownership held in accordance with Article 4 of the Spanish Securities Market Law, and the percentage of capital owned by other significant shareholders8. All these variables are normalized to have a mean of 0 and a standard deviation of 1.

Ruiz-Mallorquí & Santana-Martín (2011) find that when the dominant institutional investor is a banking institution, this increases the value of unlisted Spanish firms. Comparable findings are reached by de Miguel et al. (2004). Saona et al., (2019) find that more concentrated ownership structures, as found in Spain, and the presence of institutional investors act as corporate governance drivers that prevent earnings mismanagement.

Transparency in financial reporting (IndexEQ): We include the quality of financial information in our corporate governance index because, first, corporate governance and readability reports are highly correlated as recently reported by Melon-Izco et al. (2021) and Arcas-Pellicer et al. (2022) for Spanish companies and government agencies and, second, earnings management is a critical issue for Spanish firms (Saona et al., 2020). This metric is an already-defined, scaled variable that tracks earnings quality as developed by StarMine. This metric is comparable to those described in previous empirical studies such as Obeng et al. (2020), Beyer et al. (2019), and Gaio & Raposo (2011). Earnings quality is based on a percentile ranking from 0 to 100 of stocks based on sustainability of earnings, with 100 representing the most sustainable. StarMine defines earnings quality as the degree to which past earnings are reliable and likely to persist. High-quality earnings accurately reflect a company’s current and past operating performance, indicate future operating performance, and reliably measure company value, regardless of the level of earnings. Meanwhile, according to StarMine, companies with poor earnings quality are not necessarily engaging in earnings manipulation; in most cases, low earnings quality reflects a likelihood of deteriorating fundamentals and reflects low reporting transparency because of weak internal-governance tools. Furthermore, earnings quality can be measurably high. This is the case for companies that have very persistent earnings and strengthening fundamentals and are likely to outperform their benchmarks in the future, assuming earnings faithfully represent the effect of good corporate governance on the firm’s economic performance. This also is the case for companies whose earnings have high informational content or high transparency.

Gaio & Raposo (2011) find a positive and significant relationship between earnings quality and firm value across firms in thirty-eight countries. This relationship is stronger in countries with big investment opportunities and low investor protection. More recently, Pavlopoulos et al. (2019) and Obeng et al. (2020) confirm the relationship.

The earnings-quality algorithm developed by StarMine is broken down into accruals, cash flow, and operating efficiency. Accordingly, earnings can be broken down into accruals and cash flow. Accruals are measured as changes in operating assets and liabilities from four quarters ago to the most recent quarter. The measure includes changes in both current and noncurrent operating assets and liabilities. Finally, accruals are scaled by average assets. The operating-cash-flow component of earnings is defined as the sum of net cash flow from operations and cash flow from investment. Cash flow is relatively free of estimation error and therefore is more reliable than accruals. It is measured as annualized free cash flow scaled by average assets. StarMine computes free cash flow as the cash generated (used) by operations after subtracting capital expenditures, which are investments made in the business to support operations. Finally, the operating-efficiency measure of earnings quality is based on return on assets. Return on assets is decomposed into a profit-margin subcomponent and an asset-turnover subcomponent, similarly to a DuPont analysis. StarMine evaluates asset turnover and profit margin against sector benchmarks because of the structurally different ways in which companies in various industries produce similar levels of return on assets. Profit margin is measured using the annualized operating profit margin as a percentage of annualized sales while total-asset-turnover ratio is calculated as annualized sales over average net operating assets. Change in asset turnover measures the annualized asset turnover for the most recent quarter minus the annualized asset turnover from four quarters ago. Based on these three measures, StarMine creates a ranking of all stocks in the country. This ranking, an overall measure of earnings quality, corresponds to our first metric of earnings quality \(\left( EQ1 \right)\). Our alternative metrics of earnings quality correspond to accruals \(\left( EQ2 \right)\), cash flow \(\left( EQ3 \right)\), and operating efficiency \(\left( EQ4 \right)\) as defined above. This composite index is normalized to have a mean of 0 and a standard deviation of 1.

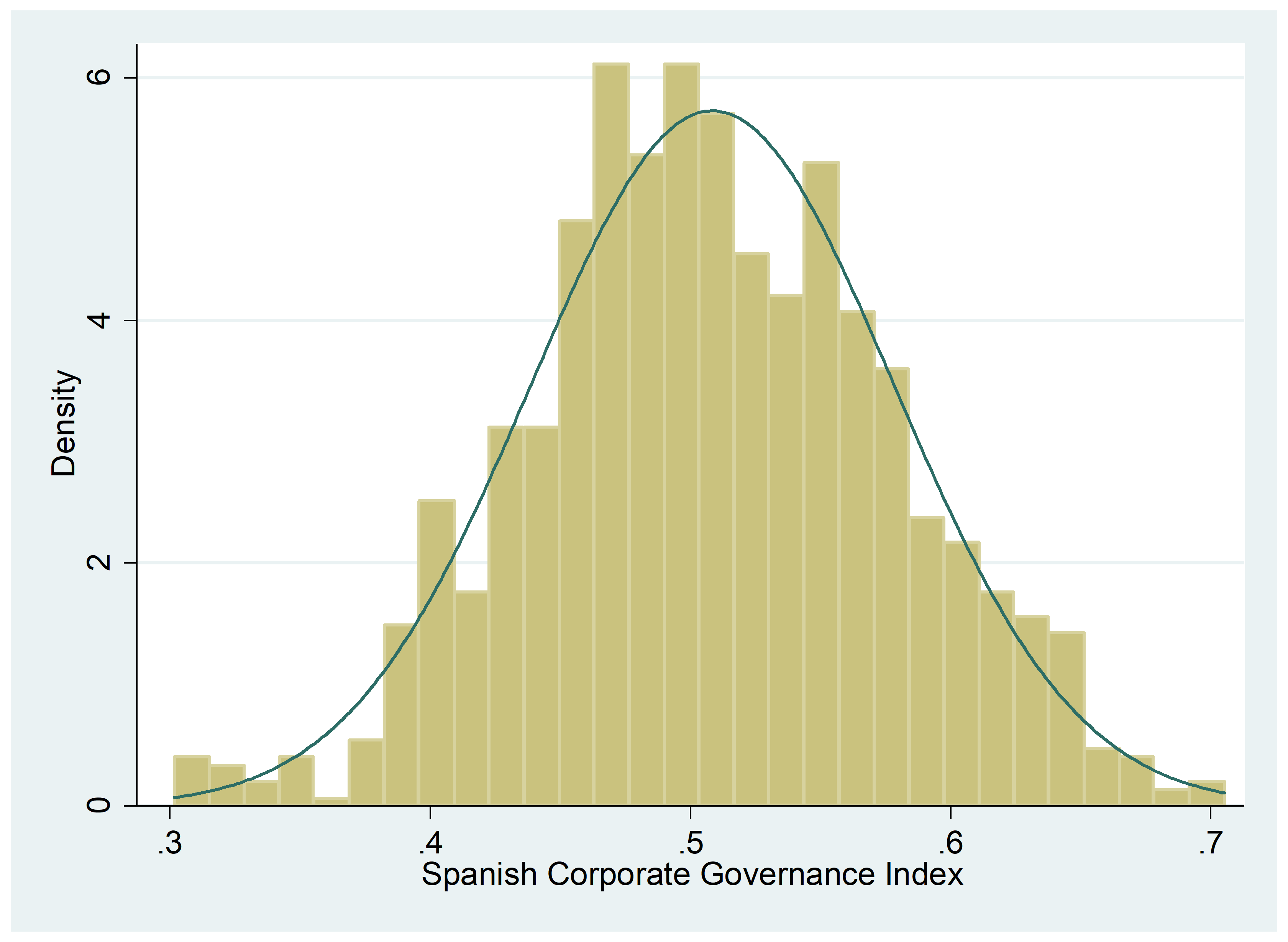

Finally, these four subindices are equally weighted to generate S-CGI.9 Subsequently, S-CGI is normalized to have a mean of 0 and standard deviation of 1.

3.3. Source of information

Our study is conducted with information on a sample of 130 listed Spanish companies with a total of 1,039 firm-year observations. This gives us an average of almost 8 continuous observations per company in our micropanel data. According to Baltagi (2013), a minimum of 4 continuous observations per individual (for example, a company) is a sine qua non condition to run an efficient panel-data estimation, even if it is unbalanced as in this study. The financial information, the information concerning the ownership-structure features, and the data regarding the quality of financial reporting were obtained from Thomson Reuters REFINITIV EIKON from 2007 to 2018. Given their regulated status and different financial reporting system, financial institutions were excluded from the sample. The advantage of Thomson Reuters REFINITIV EIKON is that it contains homogenized data and enables comparison and analysis of data on companies in different industrial sectors. Board-feature variables and the degree of compliance with codes of good governance were obtained from the Annual Report on Corporate Governance published by the Spanish Stock Exchange Commission (Comisión Nacional del Mercado de Valores). Table 2 describes how the variables were constructed.

Table 2. Variables’ construction

This table provides information about the construction of the variables used in this study. The dependent variable is firm value. The independent variables are SCGI, which is the corporate governance index for Spanish firms, and SCGI_N, the index’s normalized value. IndexCGG represents the subindex of SCGI concerning the degree of compliance with codes of good governance, IndexBOARD represents the subindex of features of boards of directors, IndexOWN is the subindex component that represents firm’s ownership-structure features, and Index EQ represents the subindex that measures transparency in financial reporting. Beneath these variables, their normalized versions are reported. Control variables include Size, ROA, Lev, and CAPEX.