Forty years of publications on strategic management accounting: Exploring the conceptual structure through co-word analysis

ABSTRACT

The main purpose of this paper is to explore the conceptual structure of strategic management accounting (SMA) research over the past 40 years to reveal and synthesize research trends in the field. To achieve this goal, we applied a bibliometric approach to analyze 326 peer-reviewed articles retrieved from Scopus and Web of Science databases. We conducted a co-word analysis using the VOSviewer software. The bibliometric analysis reveals the main outlets that published articles on SMA, and the most prolific authors and cited articles. Our findings reveal four main research streams in this field as follows: (i) SMA as a source of competitive advantage, (ii) strategic performance measurement systems, (iii) the SMA adoption and context of use, and (iv) the role of SMA in the strategic management process. For each research stream, we systematize some research themes. Additionally, our findings highlight potential emerging topics, such as the role of SMA in the integration of sustainability within companies’ strategy; and new settings of study, which represent opportunities for further research. Thus, this paper intends to support researchers in positioning their future research efforts.

Keywords: Strategic management accounting; Bibliometric analysis; Science mapping; Conceptual structure; Co-word analysis; VOSviewer.

JEL classification: M41.

Cuarenta años de publicaciones en contabilidad de gestión estratégica: Explorando la estructura conceptual a través del análisis de co-palabras

RESUMEN

El propósito de este artículo es explorar la estructura conceptual de la investigación sobre contabilidad de gestión estratégica (CGE) realizada en los últimos 40 años para revelar y sintetizar las tendencias de investigación. Para lograr este objetivo realizamos un estudio bibliométrico basado en 326 artículos revisados por pares obtenidos en las bases de datos Scopus y Web of Science que fueron analizados empleando el análisis de co-palabras y la herramienta VOSviewer. El análisis bibliométrico revela las principales revistas que han publicado artículos sobre CGE, así como los autores más prolíficos y artículos más citados. Nuestros resultados revelan cuatro líneas de investigación principales sobre CGE: (i) CGE como fuente de ventaja competitiva, (ii) sistemas de medición del desempeño estratégico, (iii) la adopción y el contexto de uso de la CGE, y (iv) el papel de la CGE en el proceso de gestión estratégica. Para cada línea de investigación sistematizamos algunos temas de investigación. Además, nuestros resultados destacan posibles temas emergentes, como el papel de la CGE en la integración de la sostenibilidad en la estrategia de las empresas, y nuevos escenarios de estudio, que representan oportunidades para futuras investigaciones. Por lo tanto, este artículo pretende ayudar los investigadores a posicionar sus futuros esfuerzos de investigación.

Palabras clave: Contabilidad de gestión estratégica; Análisis bibliométrico; Cartografía científica; Estructura conceptual; Análisis de co-palabras; VOSviewer.

Códigos JEL: M41.

1. Introduction

SMA emerged about 40 years ago to restore management accounting relevance (Roslender, 1995). Simmonds (1981) was the first author to use the term SMA and define it. Since then, several authors have contributed to its development (Bromwich, 1990; Roslender & Hart, 2002, 2003, 2010; Shank, 1996; Shank & Govindarajan, 1992; Simmonds, 1982) and research (Cadez & Guilding, 2008; Carlsson-Wall et al., 2015; Cescon et al., 2019; Guilding et al., 2000; Hadid & Al-Sayed, 2021; Henri et al., 2016; Höglund et al., 2021; Hutaibat, 2019; Lapsley & Rekers, 2017; Pavlatos & Kostakis, 2018). Some of them have presented messages of hope and confidence concerning the SMA’s role and relevance in the organizations (Cadez & Guilding, 2008; Carlsson-Wall et al., 2015; Langfield‐Smith, 2008). Others have doubts regarding its development and implementation (Dixon, 1998; Lord, 1996; Seal, 2010).

Although literature reviews on the SMA field exist (Abdullah et al., 2022; Langfield‐Smith, 2008; Nixon & Burns, 2012; Ojra et al., 2021; Rashid et al., 2020a, 2020b; Roslender & Hart, 2003; Tayles, 2011), no prior evidence of a literature review using bibliometric methods was found. Most of these literature reviews adopt a traditional approach to review different facets of the SMA literature. Roslender & Hart (2003) review the origins of SMA, stressing the attribute costing, and redefine SMA by incorporating insights from the marketing management. Langfield‐Smith (2008) examines the origins of SMA and analyses the extent of the adoption of SMA practices, particularly activity-based costing (ABC). Tayles (2011) discusses the concept of SMA and presents a set of SMA practices. He also highlights the management accountant’s role. Nixon & Burns (2012) discuss the evolution of the SMA research in the context of strategic management evolution. Recently, Rashid et al. (2020a) review 19 empirical studies focused on the adoption, benefits, and contingencies of SMA practices and the influence of their adoption on performance. Rashid et al. (2020b) adopt a systematic approach to extend the study of Langfield‐Smith (2008). They review articles on SMA published in 23 leading accounting journals between 2008 and 2019. Ojra et al. (2021) also perform a systematic review focused on SMA foundation, three contingencies of SMA practices usage (i.e., perceived environmental uncertainty, organizational structure, and organizational strategy), and the influence of SMA on performance. Similarly, Abdullah et al. (2022) carry out a systematic literature review based on 174 articles on SMA retrieved from Scopus and Web of Science databases. Their analysis focuses on the factors that motivate the adoption of SMA practices, the use of SMA practices for decision-making, and the influence of SMA on business performance.

Therefore, the central purpose of this paper is to explore the conceptual structure of the SMA research to reveal and synthesize research trends in the field over the past 40 years. The conceptual structure of a research field emerges from the terms (or words) used by researchers and highlights how these terms are related which allows identifying the main research streams (Castriotta et al., 2019; Cobo et al., 2011a; Zupic & Čater, 2015). Additionally, we aim to: (i) analyze the volume and trend of the publications, (ii) reveal the main outlets and the most influential authors and articles, and (iii) identify opportunities for further research.

To achieve the goals of this paper we rely on bibliometric analysis, a popular and rigorous approach (Donthu et al., 2021) which improves the quality of reviews (Zupic & Čater, 2015) and has been employed in business, management, and accounting research in the last years (Balstad & Berg, 2020; Castriotta et al., 2019; Fernandes & Pires, 2021; Mugwira, 2022; Uyar et al., 2020). Through co-author, co-citation and/or bibliographic coupling, and co-word analyzes, bibliometric studies reveal, respectively, the social, intellectual, and conceptual structures of a given research field (Gutiérrez-Salcedo et al., 2018; Zupic & Čater, 2015). In particular, co-word analysis allows (Cobo et al., 2011a; Donthu et al., 2021; Feng et al., 2017): (i) to discover the main concepts and topics addressed in a given research field, (ii) to explore the conceptual structure and its dynamics, and (iii) to identify research trends and opportunities for further research. Thus, co-word analysis is the most suitable bibliometric method to achieve the main goal of this study.

This paper makes two contributions to the current literature. Firstly, by adopting a quantitative approach, this study complements the most subjective and qualitative literature reviews on SMA performed so far. Secondly, to the best of our knowledge, no study has explored the conceptual structure of the SMA research. This paper aims to fill this gap using a co-word analysis. Therefore, our study aids in identifying not only what the previous literature says on SMA, but also prepares the ground for a new wave of research on this field, identifying the key shortcomings in knowledge and setting out opportunities for future studies.

The remainder of this paper is structured as follows. The second section presents an overview of bibliometric analysis and SMA. The third section describes the methodological procedures followed, including the compilation of bibliometric data, selection of the unit of analysis, and methods of data analysis. The fourth section describes the results of the bibliometric analysis performed. The fifth section discusses the research findings and provides some opportunities for further research. The final section provides the main conclusions and limitations.

2. Literature review

This section contains two parts. It aims to provide an overview of bibliometric analysis and the definition and dimensions of the SMA.

2.1. Bibliometric analysis

Bibliometric analysis is defined by Broadus (1987, p. 376) as “the quantitative study of physical published units, or of bibliographic units, or of the surrogates for either.” In turn, Gutiérrez-Salcedo et al. (2018, p. 1275) define it as “a set of methods used to study or measure the research through the scientific publications stored or indexed in big bibliographic databases.” The bibliometric analysis examines bibliographic data quantitatively, organizing available knowledge and revealing research trends over time of a given research field (Donthu et al., 2021). So, bibliometric analysis complements traditional literature review, adopting a systematic, transparent, and reproducible review process and introducing quantitative rigor to promote the quality of reviews (Zupic & Čater, 2015).

According to Cobo et al. (2011a) and Gutiérrez-Salcedo et al. (2018), there are two main bibliometric procedures to explore a research field: performance analysis and science mapping. Performance analysis assesses the productivity and activity’s impact of individuals and groups of scientific authors, such as researchers, universities, countries, and regions (Gutiérrez-Salcedo et al., 2018). To achieve these aims, performance analysis uses several bibliometric indicators, including (Gutiérrez-Salcedo et al., 2018): (i) production indicators (e.g., the total number of published articles and number of articles published in a period), (ii) impact indicators based on received citations (e.g., the total number of citations per published article), and (iii) indicators based on the impact of the journal (e.g., CiteScore and Impact Factor).

Science mapping reveals social, intellectual, and conceptual structures of a given research field through bibliographic networks, that is, collaboration networks, publication citation networks, and conceptual networks (Gutiérrez-Salcedo et al., 2018; Zupic & Čater, 2015). Science mapping uses a range of bibliometric methods, including co-author, co-citation, bibliographic coupling, and co-word analyzes (Cobo et al., 2011b; Gutiérrez-Salcedo et al., 2018; Zupic & Čater, 2015).

Co-word analysis is a content analysis method that explores the relationship of words (Callon et al., 1983) through the analysis of their co-occurrence in the documents’ keyword list, title, and abstract, or full text (Cobo et al., 2011b; Feng et al., 2017; Zupic & Čater, 2015). The co-occurrence of two words in the same document indicates that they are related to each other and the frequency of these co-occurrences measures the strength of the relationship between words and the similarity within documents (Feng et al., 2017). Co-word analysis is used to reveal conceptual networks (Gutiérrez-Salcedo et al., 2018), which are interpreted as the conceptual structure of a given research field (Zupic & Čater, 2015). This bibliometric method, as referred above, is the most appropriate to reach the purpose of this study regarding the conceptual structure of the SMA research.

2.2. Strategic management accounting

There is no agreement on a definition of SMA (Langfield‐Smith, 2008; Nixon & Burns, 2012). Terms such as accounting for strategic positioning (Roslender, 1995), accounting for strategic management (Dixon, 1998; Hutaibat, 2019), and strategic accounting (Bhimani & Langfield‐Smith, 2007; Brouthers & Roozen, 1999) are often used as synonymous, which makes difficult a broadly agreed definition of SMA. The term strategic cost management (SCM) is also used as synonymous with SMA (Cadez & Guilding, 2007; Tayles, 2011). However, some authors consider SCM different from SMA (Roslender & Hart, 2002) and others see SCM as a part (or a practice) of SMA (Cadez & Guilding, 2008; Phornlaphatrachakorn, 2018; Tillmann & Goddard, 2008). In other words, some authors view SMA as broader than SCM.

Nevertheless, it is generally accepted that the first author to use the term strategic management accounting was Kenneth Simmonds (1981), who defined it as the analysis of management accounting information concerning a business and its competitors to develop and monitor business strategy. However, other definitions presented chronologically in Table 1 reveal some variations. For instance, Bromwich (1990) focuses, similarly to Dixon & Smith (1993), not only on competitors but also on the market. Roslender & Hart (2003) stress the orientation of SMA to marketing management. Some recent studies (Cescon et al., 2019; Ma & Tayles, 2009) describe SMA as the body of management accounting which provides strategic information to support strategic decision-making and control. Thus, SMA encompasses the provision, analysis, and use of strategically orientated management accounting information.

Table 1. Some definitions of SMA

| Source | Definition |

|---|---|

| Simmonds (1981, p. 26) | “The provision and analysis of management accounting data about a business and its competitors, for use in developing and monitoring business strategy.” |

| Bromwich (1990, p. 28) | “The provision and analysis of financial information on the firm’s product markets and competitors’ costs and cost structures and the monitoring of the enterprise’s strategies and those of its competitors in these markets over a number of periods.” |

| Dixon & Smith (1993, p. 605) | “The provision and analysis of information relating to a firm’s internal activities, those of its competitors and current and future market trends, in order to assist in the strategy evaluation process.” |

| Roslender & Hart (2003, p. 255) | “SMA is identified as a generic approach to accounting for strategic positioning, defined by an attempt to integrate insights from management accounting and marketing management within a strategic management framework.” |

| Ma & Tayles (2009, p. 474) | “The body of management accounting concerned with strategically orientated information for decision making and control.” |

| Cescon et al. (2019, p. 606) | “SMA, as a type of organizational system, provides information that aids strategic decision-making processes.” |

Despite the lack of agreement concerning the definition of SMA, there is some consensus on the existence of at least two dimensions of SMA (Arunruangsirilert & Chonglerttham, 2017; Cadez & Guilding, 2008): (i) the management accountant’s involvement in strategic decision-making process, and (ii) the strategically oriented management accounting practices or SMA practices. The first dimension considers the critical role that management accountant plays in strategic decision-making process, providing relevant strategic information, participating, and supporting managers in this process (Alamri, 2019; Brouthers & Roozen, 1999; Tayles, 2011). The management accountant is seen as a strategic information provider and an active actor in the strategic decision-making. He provides strategic information to managers to make informed and timely decisions (Brouthers & Roozen, 1999) and assists other organizational actors in making sense of strategic decisions (Tillmann & Goddard, 2008).That is, management accountant participates as integral member of the strategic decision-making team (Abdullah et al., 2022). Therefore, SMA requires a strategic management accountant (Abdullah et al., 2022; Cadez & Guilding, 2008; Coad, 1996; Tillmann & Goddard, 2008) who assumes a business orientation and a proactive role acting as a business/strategic partner (Alamri, 2019; Wolf et al., 2015).

The second dimension comprises the SMA practices, which provide useful information for strategic decision-making. A given management accounting practice is considered an example of an SMA practice when it possesses at least one of the following features (Cadez & Guilding, 2008; Guilding et al., 2000; Hadid & Al-Sayed, 2021; Ma & Tayles, 2009): (i) environmental/external orientation (outward-looking), and (ii) long term orientation (forward-looking).

SMA practices also exhibit multidimensionality (objects such as competitors, customers, and products) and financial and non-financial measurement typologies (Cinquini & Tenucci, 2010; Tayles, 2011). Accordingly, the SMA literature provides some lists of SMA practices (Cadez & Guilding, 2008; Cescon et al., 2019; Cinquini & Tenucci, 2010; Hadid & Al-Sayed, 2021). They consider practices such as attribute costing, target costing, value chain costing, integrated or strategic performance measurement system (SPMS) (e.g., balanced scorecard), brand valuation, strategic pricing, competitor cost assessment, and customer profitability analysis. Some studies classify these practices into four (Cescon et al., 2019; Cinquini & Tenucci, 2010) or five broad categories (i.e., costing; planning, control, and performance measurement; strategic decision-making; competitor accounting; and customer accounting) (Arunruangsirilert & Chonglerttham, 2017; Cadez & Guilding, 2008; Tayles, 2011).

Some studies conceptualize and operationalize SMA based on additional dimensions (Alamri, 2019; Phornlaphatrachakorn, 2019). For instance, Alamri (2019) refines the two SMA dimensions analyzed above by expanding the concept into four dimensions. However, most of the studies have conceptualized and operationalized SMA using only one dimension corresponding to the SMA practices (Kalkhouran et al., 2017; Lachmann et al., 2013; Pasch, 2019; Pavlatos & Kostakis, 2018; Petera et al., 2020; Turner et al., 2017).

3. Methodological procedures

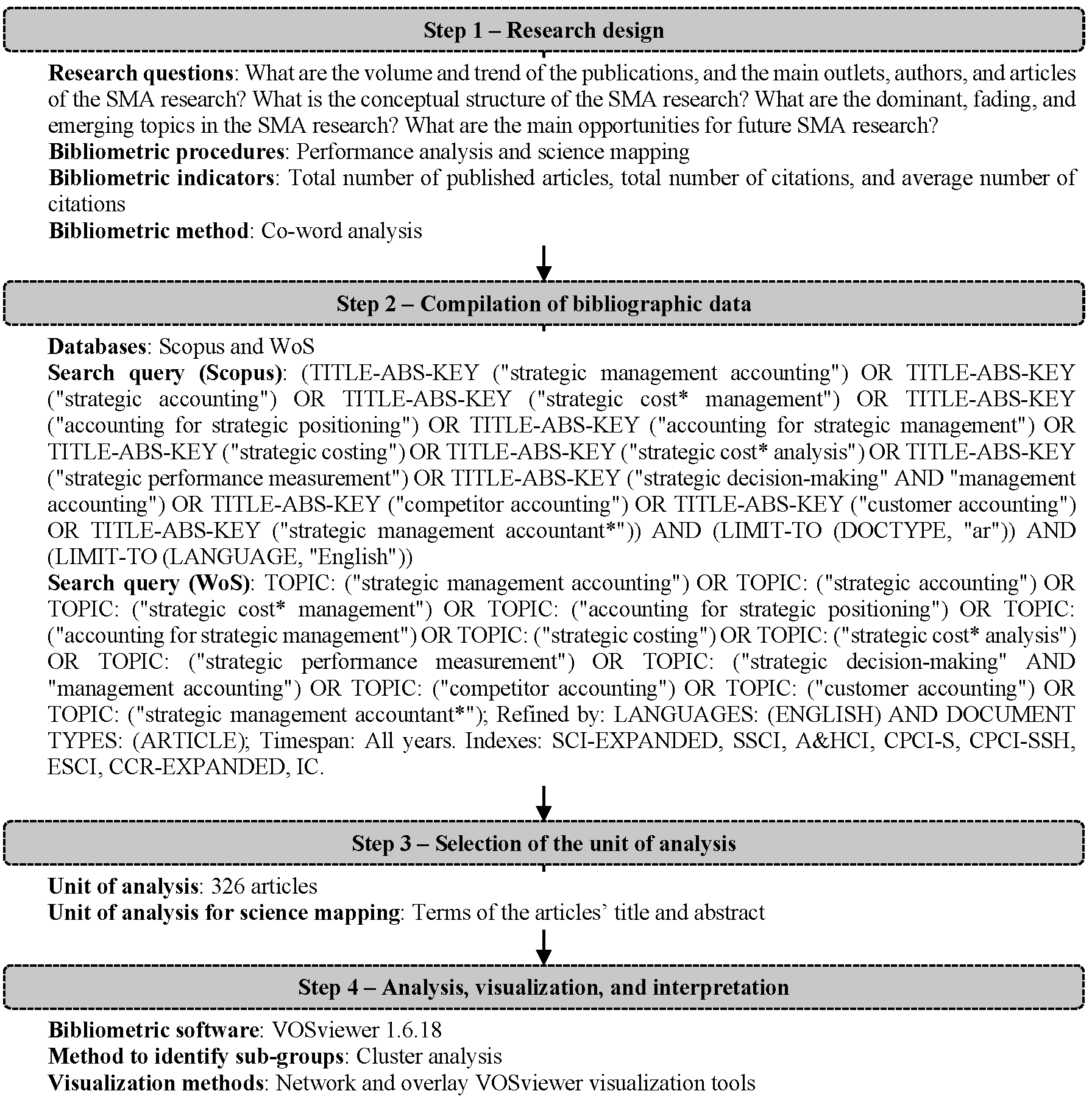

In this paper, we adopted a bibliometric approach to explore the conceptual structure of the SMA research and identify research trends in the field. Although various workflows are recommended in the literature (Donthu et al., 2021; Gutiérrez-Salcedo et al., 2018; Zupic & Čater, 2015), as Castriotta et al. (2019), we adopted a four-step procedure based on the workflow delineated by Zupic & Čater (2015). Figure 1 describes these four steps.

To answer the research questions addressed in this paper, we carried out two bibliometric procedures: performance analysis and science mapping. We undertook performance analysis to answer the first research question: What are the volume and trend of the publications, and the main outlets, authors, and articles of the SMA research? We examined production and impact indicators. In addition, we performed science mapping to answer the second and third research questions: What is the conceptual structure of the SMA research? What are the dominant, fading, and emerging topics in the SMA research? In this bibliometric procedure, we used co-word analysis. This bibliometric method has been employed to investigate the conceptual structure of several other research fields and to answer similar research questions (Castriotta et al., 2019; Fernandes & Pires, 2021; Uyar et al., 2020).

Figure 1. Workflow protocol for conducting performance analysis and science mapping with bibliometric methods (Zupic & Čater, 2015)

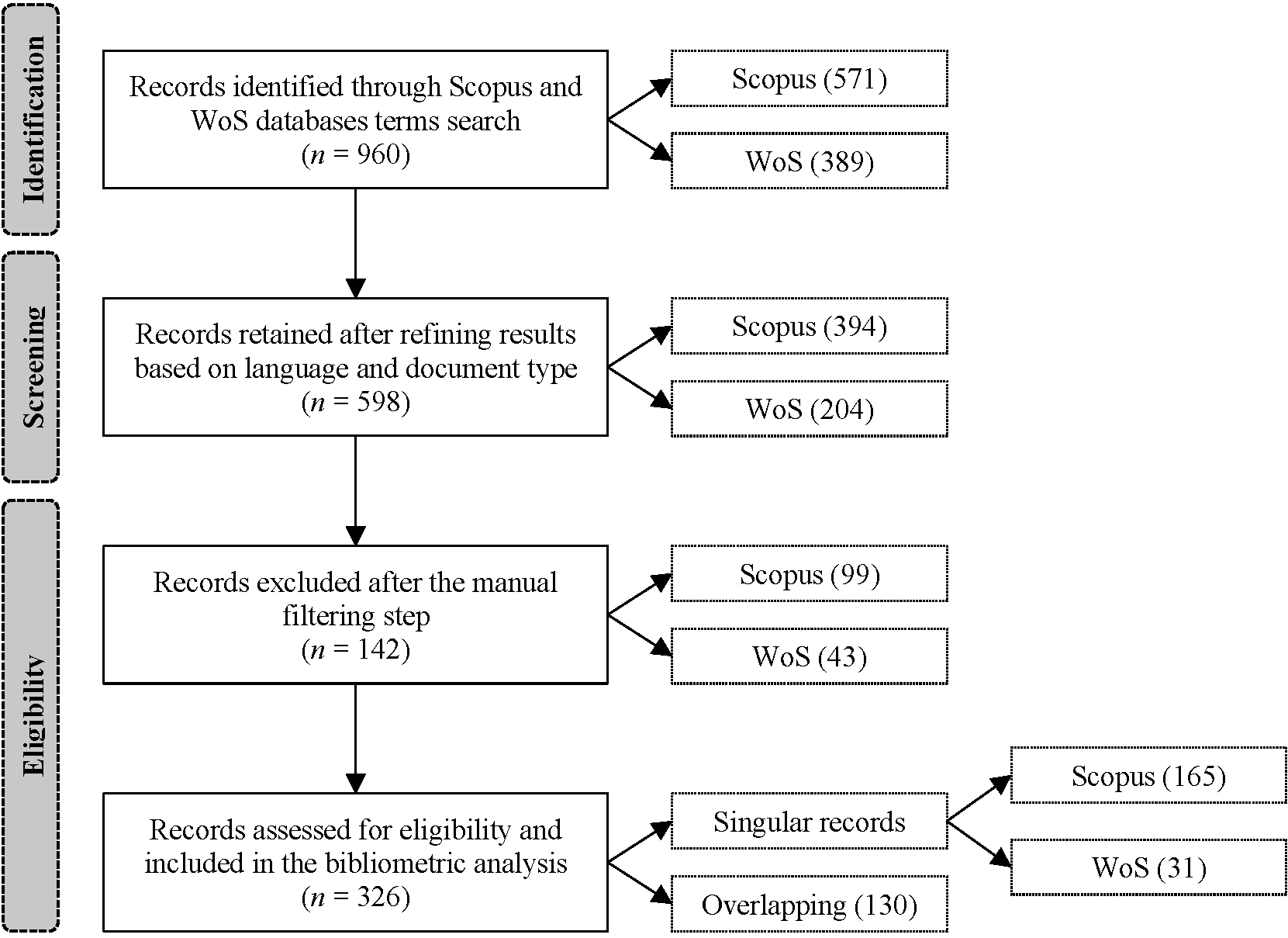

To obtain bibliographic data, some authors limit their analysis to major research journals in the field (Uyar et al., 2020). We collect data from Elsevier’s Scopus and Clarivate Analytics’ WoS,1 which are two essential sources of bibliographic data in the business, management, and accounting research (Donthu et al., 2021; Mongeon & Paul-Hus, 2016). We searched in the title, abstract, and keywords fields. No chronological filters were used. However, we restricted the searches to articles written in English and published in international journals. Other publications such as conference proceedings and book chapters were excluded to ensure the homogeneity of the sample and to ensure the reliability of the study’s findings based on peer reviewed articles only. The search was made on 02 January 2022 and returned 598 articles, 394 articles indexed in Scopus and 204 articles indexed in WoS. Figure 2 shows the process of bibliographic data collection.

Figure 2. Process of bibliographic data collection

Bibliographic data from Scopus and WoS was further analyzed in a spreadsheet and, also, using Mendeley Desktop 1.19.8. We examined the title, abstract, and keywords of all articles to determine their coherence with the scope of this study. When necessary, we analyzed the articles’ full text. Consequently, we excluded 142 articles from the initial sample either because they were out of the scope of this study or because they were not written in English. In addition, we detected 130 overlapping articles (i.e., common to both databases). Since Scopus has a higher coverage than WoS, we considered the overlapping articles as collected from Scopus. Therefore, the final sample includes a total of 326 articles.

To construct and visualize the conceptual networks, we employed the VOSviewer, version 1.6.18. This combines clustering and mapping techniques (van Eck & Waltman, 2010). Other software, such as Bibexcel and SciMAT, could be used in this process (Cobo et al., 2011b; Gutiérrez-Salcedo et al., 2018). However, VOSviewer allows to explore and interpret bibliometric maps easily (Cobo et al., 2011b; van Eck & Waltman, 2010). Moreover, VOSviewer has been used in several bibliometric analyses on business, management, and accounting research (Balstad & Berg, 2020; Castriotta et al., 2019; Fernandes & Pires, 2021; Uyar et al., 2020).

Finally, to construct the conceptual networks, we employed the text-mining resource available in VOSviewer, which extracts the terms from titles and abstracts. We could not use keywords because some articles did not contain them. In this context, and as recommended by van Eck & Waltman (2022), we used a VOSviewer thesaurus file to reduce noise into data, excluding and merging some terms.2

To visualize the terms and clusters, we used network visualization. Furthermore, we performed a temporal co-word analysis, using the overlay visualization analysis available in VOSviewer (van Eck & Waltman, 2022), to identify the fading and the emerging topics. This analysis has been used in recent studies (e.g., Castriotta et al., 2019; Fernandes & Pires, 2021). It considers the average publication year as a type of overlay to reveal the period when a particular term was most used (Castriotta et al., 2019).

4. Results

This section encompasses two parts. The first one comprises a performance analysis and sample description, exploring the publications’ evolution, journals, and authors. Additionally, it presents the most cited articles and the terms most used in the articles’ title and abstract. The second part analyzes the conceptual structure of the SMA research using co-word analysis.

4.1. Performance analysis

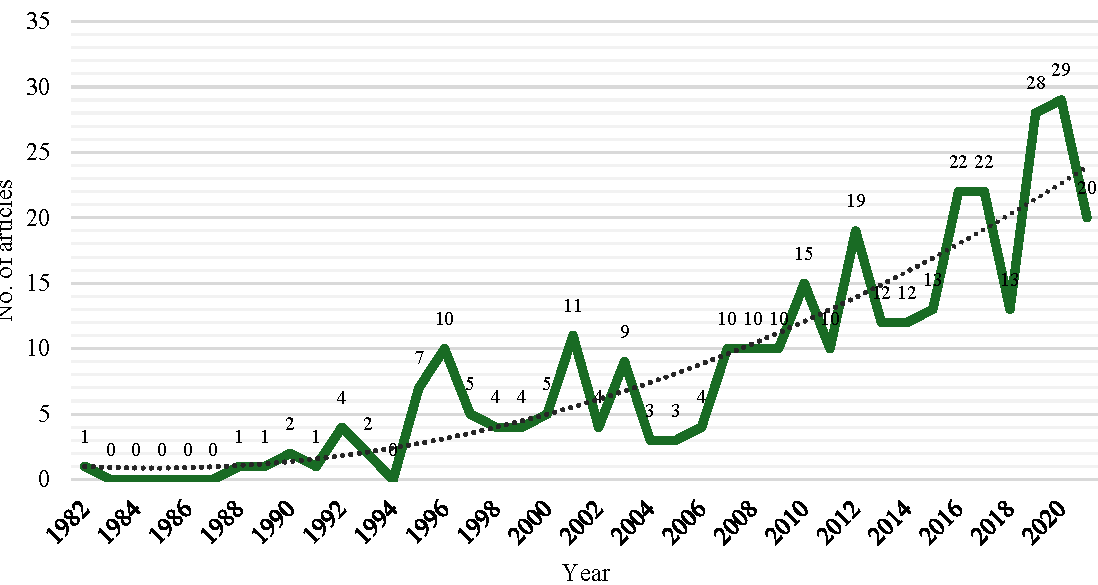

Figure 3 shows the publications’ evolution on SMA from 1982 to 2021. The first publication using the term strategic management accounting appeared in 1981 (Simmonds, 1981), but the journal was not indexed in Scopus or WoS. As can be seen, in the first decade, only six articles were published on SMA in journals indexed in Scopus and/or WoS. However, this trend has changed, particularly in the last decade and a half. Although fluctuations were observable in some years, there was a significant increase in the publications. This reveals a growing interest of the scientific community on the topic. Figure 3 highlights some peaks corresponding to two special issues of Management Accounting Research journal focused on SMA (1996 and 2012) and one special issue of Long Range Planning journal focused on SPM (2010). 2020 was the most productive year with 29 articles.

Figure 3. Evolution of publications from 1982 to 2021

The analysis of scientific journals reveals that most articles were published in accounting and management journals, but some were in different fields, such as engineering, technologies, and tourism. This gives us a sense of the transversal nature of the research on SMA. Nevertheless, it should be noted that some of these journals have published a smaller number of articles dealing with SMA. In total, 180 journals published articles on the topic. Only 55 journals published two or more articles, while the other 125 published only one article each, which shows that the distribution of research on SMA is quite extensive. This may be due to the wide range of journals that publish management accounting research (Balstad & Berg, 2020) and, consequently, can also publish SMA research.

Table 2 lists thirteen journals with the highest number of published articles (four or more). The journals with the most publications are Management Accounting Research (MAR) (33 articles), Journal of Accounting & Organizational Change (JAOC) (13 articles), and Accounting, Organizations and Society (AOS) (11 articles). These journals are the major outlets to publish articles on SMA and should be considered by researchers when choosing where to publish studies on this topic.

Table 2. Journals with four or more publications

| Source title | fi | TC | C/P |

|---|---|---|---|

| Management Accounting Research | 33 | 2,632 | 79.76 |

| Journal of Accounting & Organizational Change | 13 | 177 | 13.62 |

| Accounting, Organizations and Society | 11 | 1,996 | 181.45 |

| Long Range Planning | 7 | 321 | 45.86 |

| Measuring Business Excellence | 6 | 151 | 25.17 |

| Academy of Accounting and Financial Studies Journal | 5 | 3 | 0.60 |

| European Accounting Review | 5 | 223 | 44.60 |

| Pacific Accounting Review | 5 | 31 | 6.20 |

| Actual Problems of Economics | 4 | 0 | 0.00 |

| International Journal of Productivity and Performance Management | 4 | 91 | 22.75 |

| Journal of Asian Finance, Economics and Business | 4 | 15 | 3.75 |

| The British Accounting Review | 4 | 94 | 23.50 |

| The Journal of Corporate Accounting & Finance | 4 | 6 | 1.50 |

fi – absolute frequency (total number of published articles); TC – total number of citations received by the published articles; C/P – average number of citations per published article.

To achieve a more complete overview of this research field, we also analyzed the authors with the greatest research output, similarly to previous bibliometric studies (e.g., Rojas-Lamorena et al., 2022; Zhai et al., 2023). According to Furrer et al. (2008), the analysis of the most productive authors is critical to understand the past evolution of the topic and directions of further developments. Therefore, as Rojas-Lamorena et al. (2022) and Zhai et al. (2023), we measure the author’s productivity by the number of articles published on the topic and selected to the study, and the author’s impact by the number of citations received by these articles. This analysis does not intent to assess the articles’ quality or the quality of the research performed by the authors.

The total number of authors who have published on this topic during the period under analysis is 622 (531 authors only have written one article and 67 have written two articles). In Table 3, we highlight the authors with three or more publications (that is, with the highest number of articles published on the topic, indexed in Scopus and WoS databases, and included in the sample of this study) and the total number of citations received by these publications. Chris Guilding leads the ranking of the most productive authors with seven articles. Mike Bourne stands out with the greatest number of citations received (795 citations).

Guilding and his colleagues make relevant contributions to the field. They provide the first list of SMA practices and examine their incidence and perceived merit in New Zealand, United Kingdom, and United States (Guilding et al., 2000). Other Guilding’s studies focus on customer accounting, one of the categories of SMA practices (Guilding & McManus, 2002; McManus & Guilding, 2008), and on the use and context of use of SMA practices (Cadez & Guilding, 2007, 2008).

Bourne also makes relevant contributions in the topic of SPMSs, which have been cited by many researchers. Bourne’s studies analyze the appropriateness of SPMSs development processes for small- and medium-sized enterprises (Hudson et al., 2001) and the factors that influence the effective use of SPMSs by organizations (Franco-Santos & Bourne, 2003). Bourne and his colleagues also develop a framework that helps to understand the consequences of SPMSs (Franco-Santos et al., 2012).

Table 3. Authors with three or more publications

| Authors | fi | TC | C/P |

|---|---|---|---|

| Guilding, C. | 7 | 658 | 94.00 |

| Yuliansyah, Y. | 6 | 54 | 9.00 |

| Phornlaphatrachakorn, K. | 5 | 17 | 3.40 |

| Roslender, R. | 5 | 256 | 51.20 |

| Cadez, S. | 4 | 352 | 88.00 |

| McManus, L. | 4 | 194 | 48.50 |

| Oyewo, B. | 4 | 2 | 0.50 |

| Bates, K. | 3 | 55 | 18.33 |

| Bourne, M. | 3 | 795 | 265.00 |

| Hart, S. | 3 | 185 | 61.67 |

| Hutaibat, K. | 3 | 20 | 6.67 |

| Khan, A. | 3 | 19 | 6.33 |

| Kryshtopa, I. | 3 | 0 | 0.00 |

| Lesníková, P. | 3 | 87 | 29.00 |

| Maelah, R. | 3 | 7 | 2.33 |

| Pavlatos, O. | 3 | 36 | 12.00 |

| Rahman, I. | 3 | 13 | 4.33 |

| Rahmawati, R. | 3 | 14 | 4.67 |

| Rajnoha, R. | 3 | 87 | 29.00 |

| Rasid, S. | 3 | 16 | 5.33 |

| Shank, J. | 3 | 81 | 27.00 |

| Silvi, R. | 3 | 127 | 42.33 |

| Šiška, L. | 3 | 17 | 5.67 |

| Tayler, W. | 3 | 164 | 54.67 |

fi – absolute frequency (total number of published articles); TC – total number of citations received by the published articles; C/P – average number of citations per published article.

Some publications have seminal roles in the evolution of the knowledge field (Furrer et al., 2008). Table 4 shows the ten articles which achieved the highest impact in terms of number of citations. Ittner et al. (2003) ranks first with 593 citations. This study examines the influence of two approaches to SPM (i.e., greater measurement diversity and alignment with firm strategy and value drivers) on performance of US financial services firms. As we can see, the first seven of the ten most-cited articles focus on SPMSs, which reveals the high interest in this research theme. The remaining three theorize on the role of accountants in the strategic decision-making process (Bromwich, 1990) and the integration of sustainability within the organizational strategy (Gond et al., 2012), and investigate the contingency context of SMA (Cadez & Guilding, 2008). Among the ten most-cited articles, four were published in AOS, three in MAR, one in IJOPM, one in SMR, and one in NML. In particular, AOS and MAR are the most-cited journals that publish management accounting research in Scopus and WoS databases (Balstad & Berg, 2020).

Table 4. The 10 most-cited articles

| Authors (year) | Title | Journal | TC | C/Y |

|---|---|---|---|---|

| Ittner et al. (2003) | Performance implications of strategic performance measurement in financial service firms | AOS | 593 | 31.94 |

| Chenhall (2005) | Integrative strategic performance measurement systems, strategic alignment of manufacturing, learning and strategic outcomes: An exploratory study | AOS | 491 | 30.69 |

| Kaplan (2001) | Strategic performance measurement and management in nonprofit organizations | NML | 436 | 21.80 |

| Hudson et al. (2001) | Theory and practice in SME performance measurement systems | IJOPM | 372 | 18.60 |

| Atkinson et al. (1997) | A stakeholder approach to strategic performance measurement | SMR | 342 | 14.25 |

| Franco-Santos et al. (2012) | Contemporary performance measurement systems: A review of their consequences and a framework for research | MAR | 331 | 36.78 |

| Speckbacher et al. (2003) | A descriptive analysis on the implementation of balanced scorecards in German-speaking countries | MAR | 313 | 17.39 |

| Cadez & Guilding (2008) | An exploratory investigation of an integrated contingency model of strategic management accounting | AOS | 251 | 19.31 |

| Gond et al. (2012) | Configuring management control systems: Theorizing the integration of strategy and sustainability | MAR | 228 | 25.33 |

| Bromwich (1990) | The case for strategic management accounting: The role of accounting information for strategy in competitive markets | AOS | 214 | 6.90 |

TC – total number of citations; C/Y – average number of citations per year; IJOPM – International Journal of Operations and Production Management; SMR – Sloan Management Review; NML – Nonprofit Management and Leadership.

Finally, we used the VOSviewer to identify the terms most quoted in the articles’ titles and abstracts, and the Wordclouds software to create a words (or terms) cloud. Figure 4 represents the 112 terms quoted more than fourteen times in the articles’ title and abstract, out of a total of 6,092 terms identified. As we can see, the terms that most stand out are SMA, performance, company, effect, relationship, management, and SPMS. These terms appear interrelated with other terms, such as strategy, system, use, manager, balanced scorecard, cost, and information. Figure 4 also reveals other terms related to the concept (e.g., management accounting, SCM, customer, SPM, customer accounting, competitive advantage, strategic decision-making, and management accountant) the research (e.g., model, framework, survey, case study, sample, questionnaire, and interview), and the use of SMA (e.g., development, implementation, factor, context, and adoption).

Figure 4. Representation of the 112 terms with more than fourteen occurrences in the titles and abstracts

In short, the sample comprises articles published in scientific journals from 1982 to 2021. Despite some fluctuations, there is an increasing trend of the publications. 2020 was the most productive year. However, there is an extensive dispersion of the journals and authors that publish articles on SMA. Only MAR stands out with 33 publications and some of the most cited articles. Regarding the occurrence of terms, Figure 4 reveals the terms most quoted. It suggests that research has been done on (i) the development, adoption, and use of SMA, (ii) the context of adoption and use of SMA and its influence on performance, (iii) the role of management accountant, (iv) the importance of SMA for strategic decision-making, (v) the role of SMA in the strategic management process, and (vi) the features, implementation, and role of SPMSs (e.g., BSC).

4.2. Science mapping: Conceptual structure using co-word analysis

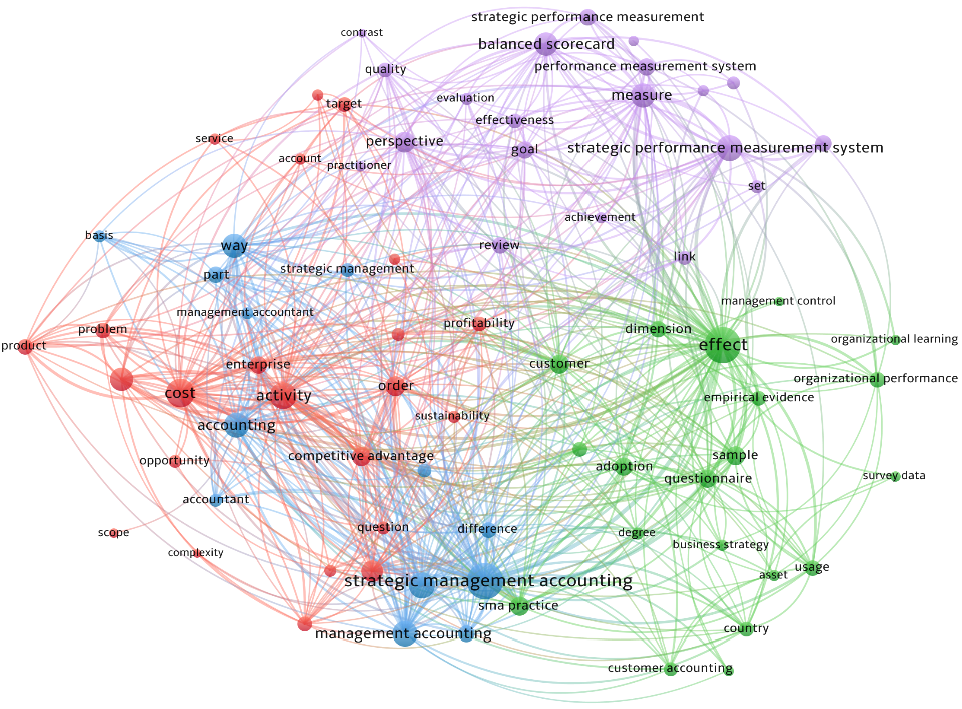

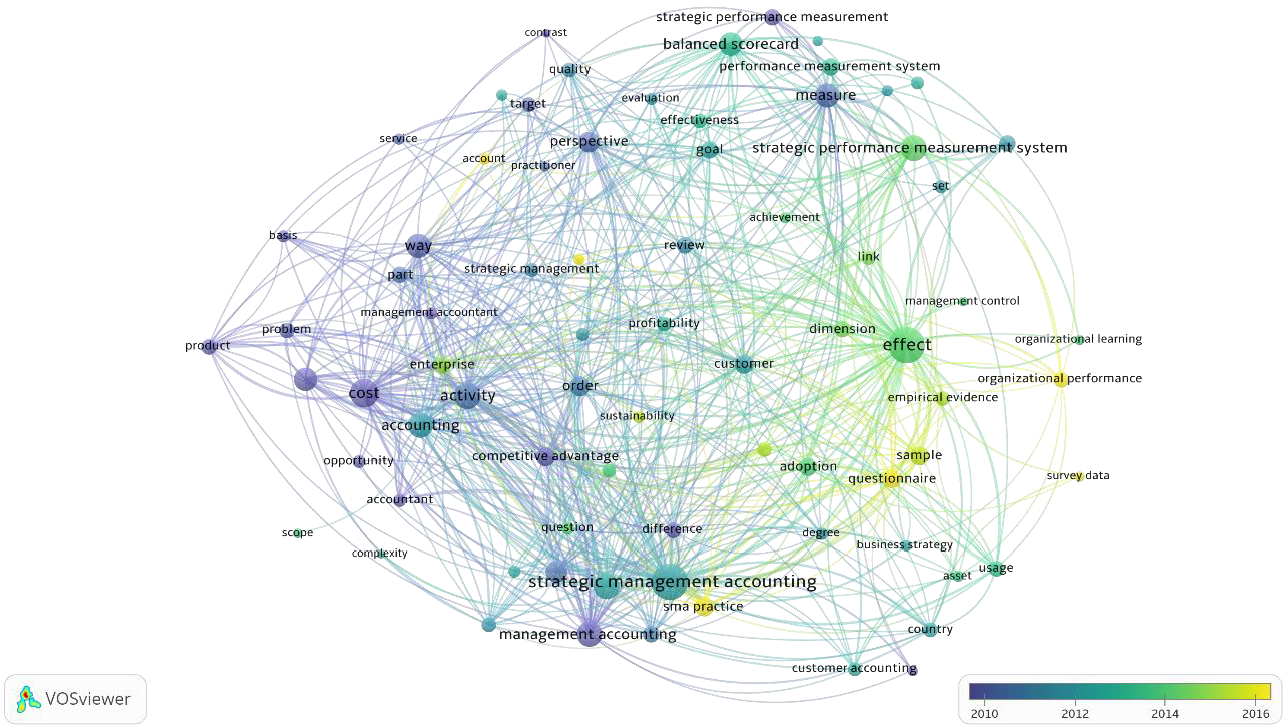

To explore the conceptual structure of the SMA research over the past 40 years, we generated a terms co-occurrence map based on titles and abstracts (see Figure 5). Colors indicate the cluster to which a term was assigned (van Eck & Waltman, 2010) and each cluster of terms represents a research stream. The map displays 76 terms that had met a threshold of at least ten co-occurrences. It reveals four clusters (four main research streams, not mutually exclusive): (i) Cluster 1 (red) - SMA as a source of competitive advantage, (ii) Cluster 2 (purple) - strategic performance measurement systems, (iii) Cluster 3 (green) - the SMA adoption and context of use, and (iv) Cluster 4 (blue) - the role of SMA in the strategic management process. Table 5 presents the terms that compose each one of the clusters and some associated references. Below we provide a brief overview of each of them.

Figure 5. Terms co-occurrence map based on articles’ title and abstract (threshold n = 10; display 76 terms; network visualization)

Table 5. Research streams on SMA and some associated references

| Cluster: Research stream | Terms | Some references |

|---|---|---|

| Cluster 1 (red): SMA as a source of competitive advantage. | Ability, account, activity, application, choice, competitive advantage, competitiveness, complexity, cost, enterprise, market, opportunity, order, problem, product, profitability, question, recommendation, scope, service, strategic cost management, sustainability, target. | Bjørnenak (2000), Cugini et al. (2007), Ellram & Stanley (2008), Ewert & Ernst (1999), Fayard et al. (2012), Henri et al. (2016), Marlina et al. (2020), McNair et al. (2001), Roslender & Hart (2002, 2003, 2010), Sedevich-Fons (2018), Shank (1996), Tanc & Gokoglan (2015), Trussel & Bitner (1998), and Woods et al. (2012). |

| Cluster 2 (purple): Strategic performance measurement systems. | Achievement, balanced scorecard, contrast, effectiveness, evaluation, goal, hypothesis, link, measure, performance measure, performance measurement, performance measurement system, perspective, practitioner, quality, review, set, strategic performance measurement, strategic performance measurement system, top management. | Appuhami (2019), Aranda & Arellano (2010), Atkinson (1998), Atkinson et al. (1997), Baird (2017), Bisbe & Malagueño (2012), Chenhall (2005), Franco-Santos & Bourne (2003), Gimbert et al. (2010), Hudson et al. (2001), Ittner et al. (2003), Kaplan (2001), Knox (2021), Parisi (2013), Silvi et al. (2015), Speckbacher et al. (2003), Srimai et al. (2011), Webb (2004), Yuliansyah & Jermias (2018), and Yuliansyah et al. (2019). |

| Cluster 3 (green): The SMA adoption and context of use. | Adoption, asset, business strategy, competitor, country, customer, customer accounting, degree, dimension, effect, empirical evidence, management control, organizational learning, organizational performance, questionnaire, resource, sample, SMA practice, survey data, usage. | Alamri (2019), Arunruangsirilert & Chonglerttham (2017), Cadez & Guilding (2007, 2008), Cescon et al. (2019), Cinquini & Tenucci (2010), Coad (1996), Gonçalves et al. (2018), Guilding et al. (2000), Hadid & Al-Sayed (2021), Kalkhouran, et al. (2017), Lachmann et al. (2013), McManus (2013), Pasch (2019), Pavlatos (2015), Pavlatos & Kostakis (2018), Phornlaphatrachakorn (2019), Turner et al. (2017), and Wolf et al. (2015). |

| Cluster 4 (blue): The role of SMA in the strategic management process. | Accountant, accounting, basis, consideration, difference, management accountant, management accounting, part, strategic decision-making, strategic management, strategic management accounting, technique, way. | Bhimani & Langfield‐Smith (2007), Carlsson-Wall et al. (2015), Cuganesan et al. (2012), Höglund et al. (2021), Hutaibat (2019), Hutaibat et al. (2011), Lapsley & Rekers (2017), Ma & Tayles (2009), McLean & McGovern (2017), Tillmann & Goddard (2008), and Vedd & Kouhy (2001). |

Cluster 1 (red): SMA as a source of competitive advantage

This cluster encompasses articles that investigate SMA as a source of competitive advantage and value creation using several approaches. Although case studies prevail (Cugini et al., 2007; Ellram & Stanley, 2008; McNair et al., 2001; Shank, 1996; Trussel & Bitner, 1998; Woods et al., 2012), some studies use survey approaches (Fayard et al., 2012; Henri et al., 2016); others provide theoretical discussions (Ewert & Ernst, 1999; Roslender & Hart, 2010) or develop frameworks, which are not tested empirically (Marlina et al., 2020; Sedevich-Fons, 2018). Thus, future research should collect empirical evidence to validate these frameworks.

A subset of articles examines the features of some SCM practices. Ewert & Ernst (1999) analyze the target costing’s strategic characteristics. Others stress the potential of SCM to explain cost causality (Bjørnenak, 2000) and support strategic investment decisions (Carr & Tomkins, 1996; Shank, 1996; Shank & Govindarajan, 1992), as well as to enhance performance (Henri et al., 2016; Phornlaphatrachakorn, 2018). In the context of environmental costs, Henri et al. (2016) show that both components of SCM (executional cost management - the tracking of environmental costs, and structural cost management - the development of environmental initiatives) positively influence financial performance independently and together. Therefore, SCM helps companies to obtain sustainable competitive advantage and reach superior performance. Moreover, inter-organizational cost management, regarded as an SCM resource, extends the application of internal cost management activities to include managing costs in purchasing and supply chains (Fayard et al., 2012; Zsidisin et al., 2003). SCM can benefit not only a firm but also all supply chain partners.

The second subset of articles focuses on customers’ interests. These studies examine the link between a firm’s costs and the value a firm provides to its customers (McNair et al., 2001) or customer satisfaction (Cugini et al., 2007). Also, they promote “customer self-accounting as a new development within SMA” (Roslender & Hart, 2010, p. 750). In particular, McNair et al. (2001) and Cugini et al. (2007) show how the balance between firms’ costs and the product/service attributes leads to superior customer’s satisfaction and higher financial performance in the market. Accordingly, these studies evidence the potential to integrate management accounting and marketing into SMA to achieve and sustain competitive advantage (Roslender & Hart, 2002, 2003). This approach requires greater cooperation between management accountants and marketing managers (Roslender & Hart, 2002, 2003), focusing on customers’ interests (Roslender & Hart, 2010). However, it appears that there is still a weak interaction between management accounting and marketing regarding customer accounting (Matsuoka, 2020; McManus & Guilding, 2008). Thereby, future research should explore the factors that hinder and promote this interaction.

Finally, the third subset of articles explores potential competitive advantage resulting from the combination of SMA practices (Marlina et al., 2020) and/or the integration of SMA with other approaches, such as the three-dimensional concurrent engineering (i.e., the simultaneous design of products, processes, and supply chains) (Ellram & Stanley, 2008) and the quality management approach (Sedevich-Fons, 2018). SMA practices and quality management systems can complement each other, promoting the spread of SMA practices and the full exploitation of quality management systems (Sedevich-Fons, 2018). Additionally, the integration of SCM with three-dimensional concurrent engineering provides several benefits, namely the incorporation of both suppliers and customers in the supply chain, boosting operational and competitive advantage (Ellram & Stanley, 2008). Woods et al. (2012) investigate, in particular, the integration of economic value added into the target costing system, concluding that target costing allows aligning customers’ and shareholders’ interests. It can be combined with other SMA practices, such as life cycle costing, to improve the product profitability management. Accordingly, it seems that the combination of SMA practices and their integration with different approaches may provide additional benefits, enhancing competitiveness and performance. Nevertheless, empirical evidence is still scant, which represents an opportunity to further research.

Cluster 2 (purple): Strategic performance measurement systems

This cluster contains articles that investigate the design, implementation, use, antecedents and consequences of SPMSs, one of the SMA practices related with the planning, control, and performance measurement (Cadez & Guilding, 2008; Hadid & Al-Sayed, 2021; Tayles, 2011). Most of them focuses on the BSC, developed by Kaplan & Norton (1992), which has been gaining widespread attention (Endrikat et al., 2020). To accomplish their goals, these studies use various qualitative and quantitative methodological approaches, such as case studies (Akhtar & Sushil, 2018; Aranda & Arellano, 2010; Kaplan, 2001), experiments (Knox, 2021; Webb, 2004), and survey questionnaires (Appuhami, 2019; Baird, 2017; Chenhall, 2005; Gimbert et al., 2010; Oyewo et al., 2022; Parisi, 2013; Yuliansyah et al., 2019). Furthermore, they also use several theoretical perspectives, sometimes in combination, such as contingency theory (Bisbe & Malagueño, 2012; Ittner et al., 2003; Oyewo et al., 2022; Speckbacher et al., 2003), psychological theories (Appuhami, 2019; Knox, 2021; Webb, 2004), and resource-based theory (Yuliansyah et al., 2019).

Some studies describe the design, implementation, and benefits of different types of SPMSs (Akhtar & Sushil, 2018; Silvi et al., 2015; Speckbacher et al., 2003), their defining characteristics (Baird, 2017; Knox, 2021), and also the adaptation of these systems to small-and-medium enterprises (Hudson et al., 2001) and to the nonprofit sector (Kaplan, 2001). They highlight that the use of multidimensional performance measures provided by SMPSs, namely for various strategic control and governance purposes (Cheng & Humphreys, 2016), enhances their effectiveness (Baird, 2017). Also, the inclusion of cause-and-effect relationships, another central feature of SPMSs, improves managers’ information relevance judgments and strategy appropriateness judgments (Knox, 2021). However, an effective SPMS that ensures organizations’ capability to be as flexible as circumstances require should be also sufficiently flexible (Akhtar & Sushil, 2018). Others studies report how organizations use information provided by these systems for strategic decision-making (Franco-Santos & Bourne, 2003; Gimbert et al., 2010). For instance, Gimbert et al. (2010) find that organizations that use SPMSs engage in a greater number and wider variety of strategic decisions in each strategy (re)formulation process, which generates more comprehensive strategic agendas. Nevertheless, most of the studies focus on the use of SPMSs for strategy implementation and monitoring, which represents an opportunity for additional research regarding de role of SPMSs for strategy (re)formulation.

Research that addresses the antecedents of SPMSs reveals that several external and organizational factors, such as strategic uncertainty, affiliation to a foreign entity, top management’s commitment, availability of specialist skills, organizational alignment, and business strategy, influence the adoption and use of SPMSs (Cheng & Humphreys, 2016; Oyewo et al., 2022; Parisi, 2013; Silvi et al., 2015). In turn, studies on the consequences of SPMSs show that this SMA practice affects people’s behavior, organizational capabilities, and performance (Endrikat et al., 2020; Franco-Santos et al., 2012). SPMSs influence managers’ goal commitment (Webb, 2004), managers’ creativity (Appuhami, 2019), strategic outcomes (Chenhall, 2005; Yuliansyah et al., 2019; Yuliansyah & Jermias, 2018), team performance (Yuliansyah et al., 2021), and organizational performance (Bisbe & Malagueño, 2012; Parisi, 2013), directly and/or indirectly through organizational learning, market orientation, psychological empowerment, and strategic alignment. Bisbe & Malagueño (2012), for instance, also stress the moderator role of environmental dynamism on the positive effect of SPMSs on organizational performance through the (re)formulation of intended strategies. However, literature on the consequences of SPMSs adoption and use on people’s behavior and on organizational capabilities seems to be scarce, as reported also previously (Endrikat et al., 2020; Franco-Santos et al., 2012), which calls for future studies. Additionally, it should be noted that most of the studies only investigate the relationships between the antecedents, SPMSs, and their consequences without examine causal mechanisms. This gap in the literature represents an opportunity for further research.

Cluster 3 (green): The SMA adoption and context of use

This cluster comprises articles that investigate the SMA adoption and context of use. It represents one of the research streams that has attracted more attention from researchers, especially in recent years.

Some studies focus on the SMA adoption and extent of SMA practices usage in Germany (Lachmann et al., 2013), Nigeria (Oboh & Ajibolade, 2017), Australia and Slovenia (Cadez & Guilding, 2007), and New Zealand, United Kingdom, and United States (Guilding et al., 2000), using questionnaire data. They show that SMA practices are not extensively adopted. The exception is competitor focused SMA practices which are the most widely used (Cadez & Guilding, 2007; Guilding et al., 2000). Nevertheless, they report higher perceived benefits than usage rates (Guilding et al., 2000). This suggests their potential and likely future adoption and usage. The limited understanding of the meaning of the SMA term and its negligible impact on managerial discourse (Guilding et al., 2000; Seal, 2010) may justify these findings. Furthermore, the higher usage of competitor focused SMA practices may result from the fact that SMA pioneers had focused SMA in the provision of information on competitors (Bromwich, 1990; Simmonds, 1981, 1982).

Most of the articles use contingency theory to investigate the context of the use of SMA and its practices (Cadez & Guilding, 2008; Cinquini & Tenucci, 2010; Gonçalves et al., 2018; Hadid & Al-Sayed, 2021; McManus, 2013; Pasch, 2019; Pavlatos, 2015; Turner et al., 2017). Some studies use contingency theory in conjunction with upper echelons theory (Kalkhouran et al., 2017; Pavlatos & Kostakis, 2018), resource-based theory (Phornlaphatrachakorn, 2019), and role theory (Pavlatos & Kostakis, 2018). Other theories (e.g., agency theory, stewardship theory, and resource dependence theory) are also used (Arunruangsirilert & Chonglerttham, 2017).

The articles under analysis examine the influence of external contextual factors (e.g., competitive forces, competition intensity, and environmental uncertainty), internal contextual factors (e.g., business strategy, innovation, market orientation, organizational learning, organizational life cycle stage, organizational structure, and size), and individual characteristics (e.g., CEO and top management team characteristics, such as age, tenure, educational background, and creativity) on both SMA dimensions (Arunruangsirilert & Chonglerttham, 2017; Cadez & Guilding, 2008) or only on SMA practices usage (Cescon et al., 2019; Cinquini & Tenucci, 2010; Kalkhouran et al., 2017; Pasch, 2019; Pavlatos, 2015; Pavlatos & Kostakis, 2018; Turner et al., 2017). Furthermore, some of them analyze the influence of SMA usage on performance (Cadez & Guilding, 2008; Kalkhouran et al., 2017; McManus, 2013; Pasch, 2019; Phornlaphatrachakorn, 2019). The studies of Pavlatos (2015) and Pavlatos & Kostakis (2018) are two exceptions that explore the influence of historical performance on SMA usage.

They reveal that contextual factors and individual characteristics influence management accountants’ involvement in strategic decision-making and SMA practices usage. This affects organizational performance. Competition intensity, prospector and deliberate strategies, decentralized structures, quality of information systems, organizational life cycle stage, and organizational size positively influence SMA usage (Cadez & Guilding, 2008; Hadid & Al-Sayed, 2021; McManus, 2013; Pasch, 2019; Pavlatos, 2015). Moreover, separation of CEO’s role and chairmanship, independent board size, and frequency of audit committee meetings (Arunruangsirilert & Chonglerttham, 2017), CEO education (level of qualifications), involvement in networks (Kalkhouran et al., 2017), and managers with business-oriented educational background, lower tenure, and highly creative (Pavlatos & Kostakis, 2018) also have a positive influence on SMA adoption and usage. On the other hand, independent chairman, board size (Arunruangsirilert & Chonglerttham, 2017), and historical performance (Pavlatos, 2015; Pavlatos & Kostakis, 2018) negatively influence SMA. SMA adoption and usage, in turn, enhances organizational performance (Alamri, 2019; Cadez & Guilding, 2008; Kalkhouran et al., 2017; Phornlaphatrachakorn, 2019). However, we can find mixed results between some contextual factors (e.g., perceived environmental uncertainty, competition intensity, business strategy, and market orientation), and SMA usage; and the relationship between SMA usage and performance. Additionally, the evidence regarding the influence of some contextual factors (e.g., organizational culture) and individual characteristics on both SMA dimensions is scarce. Thus, further research is needed to shed light on these relationships.

Cluster 4 (blue): The role of SMA in the strategic management process

This cluster includes articles that explore the role of SMA in the strategic management process using, mainly, qualitative and case study approaches (Cuganesan et al., 2012; Höglund et al., 2021; Hutaibat, 2019; Lapsley & Rekers, 2017; Ma & Tayles, 2009). Only a few articles use quantitative and survey approaches (Bhimani & Langfield‐Smith, 2007). Furthermore, they use several theoretical perspectives, such as grounded theory (Hutaibat et al., 2011; Tillmann & Goddard, 2008), institutional theory (Agasisti et al., 2008; Ma & Tayles, 2009), self-referential theory (Agasisti et al., 2008), and the strategy-as-practice perspective (Cuganesan et al., 2012; Lapsley & Rekers, 2017).

Some studies adopt a rational perspective, assuming that strategic management processes are formal, structured, sequential, and linear (Bhimani & Langfield‐Smith, 2007; Ma & Tayles, 2009). This perspective “is based on two classical perspective assumptions, namely that the environment is relatively stable and predictable and that the overarching objective of the organisation is maximising shareholder wealth” (Nixon & Burns, 2012, p. 236). Other studies address emergent strategies instead of deliberate strategies (Cuganesan et al., 2012; Hutaibat, 2019; Hutaibat et al., 2011; Lapsley & Rekers, 2017). That is, they focus, specifically, on the SMA’s role in strategic action on a day-to-day basis (Carlsson-Wall et al., 2015; Cuganesan et al., 2012).

Ma & Tayles (2009) and Tillmann & Gooddard (2008) see SMA as more than a set of particular management accounting practices. As other authors, taking a more holistic approach to SMA, they stress that any practice and accounting information can be strategic depending on their use (Carlsson-Wall et al., 2015) or on the mindset adopted (Hutaibat, 2019; Hutaibat et al., 2011). According to Hutaibat et al. (2011), the strategizing mindset is twofold: bureaucratic (i.e., more operational focus) or entrepreneurial (i.e., more strategic focus). In turn, Hutaibat (2019) identifies two dimensions (a deliberate and an unconscious dimension), which are influenced by the power structures. Thus, power structures also influence how strategizing, accounting, and decision-making occur.

Moreover, the SMA’s role in strategizing can also go beyond the decision-facilitation and decision-influencing functions, acting within organizational practices related to planning and direction setting, resource allocation, and monitoring and control through which strategizing occurs (Cuganesan et al., 2012). Accordingly, Agasisti et al. (2008) and Hutaibat et al. (2011) document the usefulness of SMA to planning and resource allocation within the particular setting of higher education. These studies reveal that SMA not only provides to strategic management processes the strategic information needed but also has an active role in “reconstitute strategic practices and engender new forms of management accounting, creating both change and continuity for strategizing” (Cuganesan et al., 2012, p. 257). For instance, in cultural industries, to act strategically, management accountants “need to connect with the wider social and institutional setting” (Lapsley & Rekers, 2017, p. 53). Nevertheless, SMA practices can function as instruments that make or break strategies because of the influence from the environment’s constituents (e.g., media and public), namely in the public sector (Höglund et al., 2021). The analysis of these mechanisms and influences should be object of further research, not only in the public sector but also in the private sector.

Finally, Figure 6 reveals a temporal overlay to the co-occurrence map shown in Figure 5, linking terms to the average date of publication (Castriotta et al., 2019; Fernandes & Pires, 2021). The temporal co-word analysis allows us to identify the fading and the emerging topics through the color/shade of each term plotted in the map (Figure 6). This is representative of their average usage over time. Darker terms are older than lighter ones. This means that darker terms were used on average around 2010 while lighter terms on average around 2016. Therefore, the temporal co-word map suggests that the research stream “SMA as a source of competitive advantage” comprises most of the oldest terms. Strategic cost management stands out as the oldest term (average year of publication = 2005.98). Since some recent studies consider SCM as a part (or practice) of SMA (Arunruangsirilert & Chonglerttham, 2017; Phornlaphatrachakorn, 2018), the use of the term SMA prevails. However, the oldest term plotted in the map is management accountant (average year of publication = 2005.88). Thus, it seems that more recent studies have not investigated the role of management accountants in the strategic management process, revealing an opportunity for future research in this area.

In turn, the research stream “the SMA adoption and context of use” contains the most recent terms: organizational performance and SMA practice (average year of publication = 2016.00 and 2016.04, respectively), and questionnaire (average year of publication = 2018.44). In fact, recent studies have addressed the adoption and use of SMA practices, as well as the influence of SMA on organizational performance, using questionnaires (Alamri, 2019; Hadid & Al-Sayed, 2021; Kalkhouran et al., 2017; Pasch, 2019; Pavlatos & Kostakis, 2018).

Figure 6. Terms co-occurrence map based on articles’ title and abstract (threshold n = 10; display 76 terms; overlay visualization)

5. Discussion and opportunities for further research

The main purpose of this study was to reveal the conceptual structure of the SMA research analyzing the terms in the articles’ title and abstract on the field over the past 40 years. Accordingly, we performed a co-word analysis to examine the relationships among words/terms based on their co-occurrence (Callon et al., 1983; Cobo et al., 2011b). We used network and overlay visualization tools available in VOSviewer. Hence, we were able to reveal the terms that SMA researchers most use. Moreover, we synthesize research trends in the field. We also anchor the use of the terms over time.

A significant result of this study, per the results of the cluster analysis, indicates the existence of four different, albeit complementary, main research streams on SMA. Only research on the adoption, context of use, and practices of SMA has been widely addressed in previous general literature reviews on SMA (Abdullah et al., 2022; Langfield‐Smith, 2008; Ojra et al., 2021; Rashid et al., 2020a, 2020b; Tayles, 2011). Other literature reviews focus exclusively on research on SPMSs (e.g., Endrikat et al., 2020; Franco-Santos et al., 2012; Hoque, 2014; Mio et al., 2022). Therefore, this study reveals and synthesizes two additional and relevant main research streams: “SMA as a source of competitive advantage” and “the role of SMA in the strategic management process”. Although they are not properly emergent research streams, to the best of our knowledge, previous literature reviews do not address them in depth. Furthermore, this study also reveals that only one category of SMA practices, regarding the SPMSs, has been extensively studied. That is, none of the other SMA practices categories has been widely investigated to emerge as a main research stream in the conceptual structure based on articles’ title and abstract. Thus, much more research is needed on these SMA practices.

Several opportunities for further research emerge in consideration of the analysis performed. For instance, SMA research has used qualitative and quantitative methodologies, case study and survey methods. However, qualitative and case study approaches is prevalent in two research streams: “SMA as a source of competitive advantage” and “the role of SMA in the strategic management process”. The use of quantitative and survey approaches is prevalent in “the SMA adoption and context of use” research stream. Only the research stream “strategic performance measurement systems” has used a greater variety of methods, including case study and survey approaches, and experiments. Additionally, only a few studies use longitudinal approaches (Aranda & Arellano, 2010; Cuganesan et al., 2012; Hutaibat, 2019; Woods et al., 2012). Thus, future research can be enriched by complementing quantitative and qualitative approaches and using longitudinal approaches.

Furthermore, previous research was more focused on large companies (Bhimani & Langfield‐Smith, 2007; Carlsson-Wall et al., 2015; Chenhall, 2005; Gonçalves et al., 2018; Parisi, 2013; Tillmann & Goddard, 2008; Woods et al., 2012) rather than small and medium-sized enterprises (Kalkhouran et al., 2017; McNair et al., 2001), as well as more focused on manufacturing industry (Appuhami, 2019; Cescon et al., 2019; Cinquini & Tenucci, 2010; Henri et al., 2016; Oyewo et al., 2022; Pavlatos & Kostakis, 2018; Shank, 1996) rather than service industries, such as financial industry (Oboh & Ajibolade, 2017; Phornlaphatrachakorn, 2019; Yuliansyah et al., 2019), hotel industry (McManus, 2013; Pavlatos, 2015; Turner et al., 2017), higher education industry (Agasisti et al., 2008; Hutaibat, 2019; Hutaibat et al., 2011), and hospital industry (Lachmann et al., 2013). Empirical evidence on the public sector is also scarce, a few exceptions being the studies of Bjørnenak (2000), Cuganesan et al. (2012), and Höglund et al. (2021), which represents an opportunity for further research. The same is true for other nonprofit organizations. Future research should also address new business models and emerging businesses such as platform companies (e.g., Amazon, Airbnb, and Uber). These platforms are different from traditional value chain business models (Dávila, 2019), which challenges the role of SMA in supporting their activities.

Additional and more specific opportunities for further research are addressed below following their relatedness to the four research streams identified through co-word analysis.

Cluster 1 (red): SMA as a source of competitive advantage

This research stream offers at least two potential opportunities for future development. First, the unprecedented situation of the COVID-19 pandemic crisis, and the recent war in Ukraine, have challenged companies to search for recovery solutions related to, for instance, reducing costs and developing innovative (or redesigning) business models (Bhattacharyya & Thakre, 2021). Companies have formulated strategies to survive and accelerate recovery to ensure long-term growth (Bhattacharyya & Thakre, 2021). SMA can support this recovery process. The literature stresses that SMA helps align companies’ resources with short-term tactics and long-term strategies (Henri et al., 2016). This enhances cost efficiency and, consequently, competitiveness and performance (Henri et al., 2016; Phornlaphatrachakorn, 2018). Moreover, it seems that companies most affected by the economic crisis tend to use SMA to improve their performance (Pavlatos & Kostakis, 2018). Therefore, future research should provide answers for the following questions: What is the role of SMA in the development of recovery solutions during higher uncertainty situations such as the pandemic crisis and the war in Ukraine? How can SMA support companies in adapting business models to promote collaborative inter-organizational practices that can build sustainable competitive advantage for long-term growth?

Second, the role of SMA in the development of organizational resources and (dynamic) capabilities has been neglected in the literature (Nixon & Burns, 2012). Only a few articles address this issue (Fayard et al., 2012; Phornlaphatrachakorn, 2018, 2019; Zsidisin et al., 2003). They examine the influence of resources and capabilities on SMA; and how SMA is seen as a resource (Fayard et al., 2012; Phornlaphatrachakorn, 2019) or a dynamic capability (Phornlaphatrachakorn, 2018). Thus, there seems to be a bi-directional relationship between management accounting and intellectual capital, which comprises knowledge-based resources and capabilities (Novas et al., 2017). Future research should improve the integration of the SMA and intellectual capital approaches, that was developed in previous studies (e.g., Tayles et al., 2002), to explore empirically the bi-directional relationship between them. Additionally, future studies should analyze the role of SMA in the acquisition, share, and use of knowledge in contexts of inter-organizational collaboration. Moreover, the influence of SMA on exploitative and explorative innovation (i.e., ambidexterity innovation) should be investigated. Given the external orientation of the SMA, it is expected that its influence on explorative innovation is higher than on exploitative innovation. Innovation is a critical activity, which promotes performance, namely in crisis periods (Somohano-Rodríguez et al., 2018).

Cluster 2 (purple): Strategic performance measurement systems

Concerning this research stream, we highlight three avenues for further research. First, some studies have investigated and reported the influence of SMPSs on people’s behavior (e.g., Appuhami, 2019; Knox, 2021; Webb, 2004). However, this issue seems to be under researched (Endrikat et al., 2020; Franco-Santos et al., 2012). For instance, little is known on how SPMSs influence employees’ innovative behavior. According to Appuhami (2019), SPMSs influence, through organizational learning and psychological empowerment, managers’ creativity, an antecedent of innovative behavior. Thus, future research should explore the (potential) effects of SPSMs on employees’ innovative behavior considering, also, the mediating and moderating role of variables such as commitment and empowerment.

Second, although some studies have addressed the influence of sustainability initiatives on the design, implementation, use, and effectiveness of SPMSs (Mio et al., 2022; Parisi, 2013), additional research is needed regarding the role of SPMSs for integrating sustainability within business strategies and achieving sustainability goals. Hence, future research should provide answers for the following questions: How SPMSs can support organizations in strategy (re)formulation for integrating environmental and social issues within organizational strategies? What is the relevance of top management´s and employees’ commitment to sustainability in this process? How environment’s constituents influence the integration of environmental and social issues within organizational strategies through SMPS?

Third, the influence of digital innovation on SPMSs and the role of SPMSs in digital transformation have been neglected in the existing literature, which requires future scholarly attention. The study of Reinking et al. (2020) is an exception. It stresses the importance of digital dashboards, which synthesize enterprise data, in assisting SPMSs and aligning organizational efforts to enhance managerial and organizational performance. In fact, digital technologies can be used to enhance business and transform business processes (Kraus et al., 2022), such as accounting and auditing (Mugwira, 2022). Thus, what are the effects of digital innovation on the design, implementation, and use of SPMSs? What is the (potential) role of digital innovation in SPMSs evolution? On the other hand, digital transformation requires strategic responses for improving the success of the change processes in companies (Kraus et al., 2022). Future research should explore the role of SMPSs (and SMA in general) in the (re)formulation, implementation, and monitoring of these strategic responses.

Cluster 3 (green): The SMA adoption and context of use

The findings also reveal some gaps in this research stream. First, no recent study examined the extension of SMA practices usage and its evolution over time (Tayles, 2011). This analysis should be performed in developed and developing countries. Cross-country studies should be also undertaken to investigate and compare the adoption and extension of usage in different countries (Cescon et al., 2019). These studies should consider the (potential) influence of national culture and other factors to understand possible differences in the adoption and usage of the SMA practices.

Second, the empirical literature reports mixed results on the influence of some contextual factors (e.g., perceived environmental uncertainty, competition intensity, business strategy, and market orientation) on SMA; and the influence of SMA on performance. Moreover, there seems to be a bidirectional relationship between SMA and performance. Pavlatos (2015) and Pavlatos & Kostakis (2018) document that organizations with lower historical performance use SMA more extensively to enhance future performance. Cadez & Guilding (2008) and Turner et al. (2017) show that SMA usage positively influences performance. Thus, these relationships should be investigated further.

Third, many determinants of SMA adoption have been explored in previous research. Nonetheless, more research is needed to investigate the influence of additional contextual factors (e.g., leadership style, organizational culture, and horizontal structures) and individual characteristics (e.g., management accountants and managers’ skills such as communication and interpersonal skills) on both SMA dimensions. Recently, Phornlaphatrachakorn (2019) and Hadid & Al-Sayed (2021) addressed, respectively, the role of transformational leadership and organizational culture (i.e., innovation-oriented culture and outcome-oriented culture) in promoting SMA usage. These studies highlight the need for more research on the influence of leadership styles and organizational culture types on SMA usage as well as on the management accountant’s involvement in strategic decision-making. Additionally, some authors stress the influence of CEO and top management team characteristics on SMA practices usage (Kalkhouran et al., 2017; Pavlatos & Kostakis, 2018). This represents an opportunity to explore the influence of board characteristics and other management accountants and manager’s skills not only on SMA practices usage but also on the management accountant’s involvement in strategic decision-making. Some of these issues can be investigated using the lens of the role theory (Pavlatos & Kostakis, 2018).

Cluster 4 (blue): The role of SMA in the strategic management process

Regarding this research stream, we highlight three interesting lines of research. First, the reviewed articles explore the use of some SMA practices in the strategic decision-making process. Little is known on the simultaneous use of several SMA practices, which can be integrated to enhance the strategic management process. In fact, “concentrating on one or two specific accounting techniques to assist strategic decision-making may reduce the relevant information available and result in less effective decision-making” (Tillmann & Goddard, 2008, p. 81). Nevertheless, according to Höglund et al. (2021), the use of multiple SMA practices may potentially obscure strategy. Future studies should address this issue to investigate how SMA practices can be used simultaneously to improve the efficiency of strategic decision-making; and to examine whether/how the use of multiple SMA practices obscure strategy.

Second, companies are currently challenged to integrate sustainability issues within their strategies (Gond et al., 2012). Some studies highlight that SMA can (and should) incorporate environmental issues enhancing sustainable competitive advantage and performance (Henri et al., 2016; Tanc & Gokoglan, 2015). Therefore, some questions need to be addressed in future research: How can SMA facilitate the integration of sustainability and strategy? What is the role of the different SMA practices? What is the role of different organizational actors in this process?

Third, although some studies have addressed the management accountant’s role in the strategic management process (Ma & Tayles, 2009; Tillmann & Goddard, 2008), future research should investigate in more depth the management accountant’s interventions in the strategy (re)formulation and its implementation and monitoring. Moreover, further research should also examine the management accountant’s interactions with other organizational actors in the strategic management process. The literature reports some cooperation between management accountants and marketing managers (Ma & Tayles, 2009; Roslender & Hart, 2003). However, empirical evidence is still scarce. Additionally, little is known about the management accountant’s interactions with other organizational actors, such as purchasing and supply chain managers, production managers, human resources managers, and strategists.

6. Conclusion

This paper aimed to explore the conceptual structure of the SMA research to reveal and synthesize research trends in the field over the past 40 years. Furthermore, it sought to assess the volume and direction of the publications, and the main outlets, authors, and articles. We achieved these goals through a combination of two bibliometric procedures: performance analysis and science mapping.

Performance analysis results showed that SMA research, despite some fluctuations, attracted growing attention between 1982 and 2021. However, the total number of articles published and indexed to the Scopus and WoS databases within the last 40 years (326) is not high. One hundred eighty journals have published articles on the topic, which shows an extensive dispersion of the research on SMA. Nevertheless, the top five journals that publish articles on SMA encompasses some of the most cited journals that publish management accounting research: MAR, the main outlet of SMA research, and AOS. Concerning articles’ authorship, none of the authors stands out as particularly prolific.

Based on the co-word analysis, science mapping results revealed four clusters of terms, corresponding to four main research streams (not mutually exclusive): (i) SMA as a source of competitive advantage, (ii) strategic performance measurement systems, (iii) the SMA adoption and context of use, and (iv) the role of SMA in the strategic management process. “The SMA adoption and context of use” and “strategic performance measurement systems” research streams are the most researched. “The SMA adoption and context of use” and “the role of SMA in the strategic management process” research streams have attracted researchers’ attention in recent years. Only one SMA practice has been consistently and extensively investigated, emerging as main research stream on SMA.

The systematization of these research streams allowed us to identify several gaps in the literature that represent opportunities for further research. Table 6 summarizes some suggestions for future research on SMA. The list is not exhaustive. However, it seems clear that we need a significantly more scholarly effort to enhance our knowledge on SMA.

Table 6. Future research on SMA

| Cluster: Research stream | Suggestions for future research |

|---|---|

| Cluster 1: SMA as a source of competitive advantage. | - Investigate how SMA supports organizations to obtain and sustain competitive advantage during higher uncertainty situations (e.g., during the Covid-19 pandemic crisis and war in Ukraine and, particularly, in the post-pandemic and post-war recovery). - Explore the role of SMA to manage and mobilize knowledge-based resources and dynamic capabilities that improve organizations’ sustainable competitive advantage. |

| Cluster 2: Strategic performance measurement systems. | - Examine the influence of SPMSs on employees’ innovative behavior. - Investigate how SPMSs can assist organizations in strategy (re)formulation for integrating environmental and social considerations within organizational strategies. - Explore the influence of digital innovation on the design, implementation, and use of SPMSs and, also, the role of SPMSs (and other SMA practices) in digital transformation. |

| Cluster 3: The SMA adoption and context of use. | - Examine the influence of organizational culture and leadership style on both SMA dimensions. - Study the influence of corporate governance (e.g., board diversity characteristics and board power) on SMA adoption and usage. - Analyze the influence of management accountant’s skills on its involvement in strategic decision-making process and, also, on SMA practices. |

| Cluster 4: The role of SMA in the strategic management process. | - Investigate how the integration and simultaneous use of some SMA practices enhance the strategic management process; and examine whether/how the use of multiple SMA practices obscure strategy. - Explore the role of SMA in the integration of sustainability in the business strategy. - Study the management accountant’s role in the strategic management process, not only as a strategic information provider but also as an active actor in the strategic decision-making (i.e., as a strategic management accountant). |