Reporting measurements or measuring for reporting? Internal measurement of the Circular Economy from an environmental accounting approach and its relationship

ABSTRACT

This paper aims to provide a model to measure the circular economy in businesses from an environmental accounting approach. The range of circular activities and the intensity with which companies implement them are analysed to increase the understanding of the relationship between the implementation of circular economy in firms and their different environmental management accounting and reporting practices.

The study is developed through an empirical analysis based on a survey addressed to a sample of Spanish companies and designed to analyse different environmental accounting practices and measure the circular economy-related activities introduced by companies to close the material loops in processes. Main results indicate that circular economy activities are generally introduced by companies progressively, without clearly responding to common patterns for the introduction of the different circular principles and activities. A moderate correlation is observed between companies' level of circular economy and their environmental management accounting practices, with a more significant correlation for a higher number of circular activities, particularly for firms that implement environmental management systems and have higher levels of transparency and sustainability information policies.

Although companies are progressively adopting circular activities, the lack of specific indicators limits their internal measurement. Consequently, the information provided by organisations about the closing of material loops remains sporadic. The results highlight the need for built-in specific metrics to deploy environmental accounting practices in circular economy models.

Keywords: Circular economy; Environmental Accounting; Sustainability report; Reporting.

JEL classification: M41; M14; Q56.

¿Reportar mediciones o midiendo para reportar? Medición interna de la Economía Circular desde una perspectiva de la contabilidad medioambiental y su interrelación

RESUMEN

Este trabajo presenta un modelo para medir la economía circular en las empresas desde un enfoque de contabilidad medioambiental. Se analizan tanto el rango de actividades circulares como la intensidad con la que son implementadas para contribuir al conocimiento de la relación entre la introducción de la economía circular en las empresas y sus prácticas de contabilidad e información de gestión medioambiental.

El estudio se desarrolla a través de un análisis empírico llevado a cabo a través de una encuesta dirigida a una muestra de empresas españolas diseñada para analizar las prácticas de contabilidad e información medioambiental y de medición de las actividades relacionadas con la economía circular introducidas por las empresas en sus procesos de cierre de círculos de materiales. Los principales resultados obtenidos indican que las actividades de economía circular son generalmente introducidas por las empresas progesivamente, sin responder de forma clara a paulas relacionadas con los distintos principios y actividades circulares. Se observa una correlación moderada entre el nivel de circularidad de las empresas y sus prácticas de contabilidad de gestión medioambiental, siendo la correlación mayor a mayor número de actividades, especialmente en lo que concierne a la implementación de sistemas de gestión ambiental o el desarrollo de políticas de transparencia y de información de sostenibilidad.

A pesar de que las empresas estén adoptando progresivamente actividades circulares, la falta de indicadores específicos limita la medición interna de la economía circular por parte de las empresas. Por consiguiente, la información proporcionada por las organizaciones acerca del cierre de círculos sigue siendo esporádica. Los resultados ponen de manifiesto la necesidad de métricas integradas específicas para el despliegue de prácticas de contabildiad medioambiental para modelos de economía circular.

Palabras clave: Economía circular; Contabilidad medioambiental; Memoria de sostenibilidad; Elaboración de informes.

Códigos JEL: M41; M14; Q56.

1. Introduction

There is an urgent need to reduce the climate and environmental impact of both production and consumption, with the ultimate aim of reaching carbon neutrality and a fully circular economy (CE). Businesses introduce climate-friendly and sustainable products and processes in various sectors, including different activities related to the CE. In this scenario, different perspectives recognise the value of the CE as an alternative model to the linear one and as a path towards a low-carbon emission and zero-waste economy based on the convergence of economic and environmental principles (Ellen MacArthur Foundation, 2015a, 2015b; European Commission, 2015, 2020).

In summary, the CE seeks an efficient flow of resources -materials, energy, water, information- that conserves them in the productive cycle for as long as possible, creating circular loops in which resources are used repeatedly (Aranda-Usón et al., 2018; Yuan et al., 2006). A CE model applies principles like reduce, reuse, recycle (3R), allowing for added value and utility of products and materials to be maintained as long as possible, favouring waste minimisation (Aranda-Usón et al., 2018; Ellen MacArthur Foundation, 2015a; Scarpellini et al., 2019).

From a micro-level perspective, the adoption of the CE involves changes in environmental management and that it needs the progressive introduction of specific indicators and measurement practices that reflect circularity for reporting and corporate social responsibility (CSR). In a circular model, commercial links with local companies become closer, stable relationships with suppliers and customers are encouraged, and by-products and waste that turn into resources for other firms (in a sort of symbiotic relationship) need to be priced (Daddi et al., 2017).

In this context, the interest of scholars in the CE models at a micro-level has increased in recent years (Katz Gerro & López Sintas, 2019; Khan et al., 2020; Lieder & Rashid, 2016; Stewart & Niero, 2018). Some authors have analysed the adoption of CE-related activities by firms (Aranda-Usón et al., 2019; Aranda-Usón et al., 2020; Khan et al., 2020; Pauliuk, 2018), the introduction of circular business models (Bocken et al., 2017; Linder & Williander, 2017; Witjes & Lozano, 2016) and the measurement of the CE in specific products and processes (Elia et al., 2017; Niero & Kalbar, 2019; Ormazabal et al., 2016). However, the study of the CE's accounting implications for businesses is still in an incipient stage of development, and the measurement of the scope of the CE from an environmental accounting perspective is understudied (Rossi et al., 2020; Scarpellini et al., 2020).

Among the studies carried out from an accounting perspective in this field, Aranda-Usón et al. (2020) identify a set of activities that companies are implementing to close the materials loops, to increase the use of recycled materials avoiding the consumption of raw materials, or decrease the consumption of carbon-based energy by using renewable energy. Impacts of a business's CE from an environmental management accounting and reporting (EMAR) perspective have been analysed by Scarpellini et al. (2019), who define and measure the internal capabilities of firms related to the introduction of the CE in organisations. However, despite the interesting contribution of these authors, previous studies do not address how firms' accounting practices are related to introducing a circular model.

Other studies have approached this issue from another nearby related field, such as the eco-innovation (Ferreira et al., 2010; Lopez-Valeiras et al., 2015; Marco et al., 2019; Scarpellini et al., 2020); the cleaner production (Schaltegger et al., 2008); or from the climate change perspective or the carbon accounting (Marco-Fondevila et al., 2020; Qian et al., 2018; Schaltegger et al., 2016). However, to the best of our knowledge, previous studies are not focused on EMAR applied by firms to introduce the CE's principles, and this study attempts to fill this gap in the literature.

Therefore, the main goal of this study is to know the level of implementation of CE in businesses and analyse the influence of the related EMAR practices. To this end, we define and measure CE-related activities' adoption to deepen the analysis of the relationship between the introduction of CE in firms and their primary environmental accounting practices. To achieve the objectives of our study, we explore CE-related activities and their EMAR practices in a sample of Spanish companies from a double theoretical perspective: the Institutional theory and the resource-based view framework.

In summary, this manuscript is organised as follows: after this introduction and the background of the study, the third section describes the sample and the methodology; the fourth section shows and discusses results, and the final section summarises the main conclusions.

2. Background

2.1. The CE in businesses and the internal measurement

The internal measurement of sustainability from a CE perspective is an underdeveloped field of study. Therefore, at the first stage, this section analyses the previous literature focused on the internal management of the CE-related activities adopted by firms within the environmental accounting framework to contribute to an understudied topic at a micro-level.

In recent years, some authors have analysed and classified different CE measurement systems and indicators in organisations. Urbinati et al. (2017) use the adoption of CE principles by business models as a unit of analysis and propose a systematic approach to measuring since the number of contributions to the field is still small. Linder et al. (2017) analyse the incentives that can lead organisations to strive for high circularity values. Rigamonti et al. (2017) argue for applying LCA methodology, which must be interpreted from a CE perspective to guarantee the consistency and robustness of results; other authors use this methodology to measure circular and symbiotic processes (Daddi et al., 2017).

Nevertheless, a CE is a complex model related to economic, environmental and social development issues (Geng et al., 2012), and its complexity implies using multidimensional indicators that can express the principles of CE and sustainability (Rossi et al., 2020). It has been argued that the relationship between an organisation's field of activity and the measurement of CE plays a crucial role in this issue because CE is a precondition for good performance (Aranda-Usón et al., 2018, 2019, 2020; Franco, 2017; Lieder & Rashid, 2016). In this sense, each organisation needs to adapt CE indicators to its specifications and standards, making it challenging to compare CE measurements from different organisations, processes and sectors (Su et al., 2013).

Su et al. (2013) and Huysman et al. (2017) apply a circular performance indicator to different approaches to waste management, and Franklin-Johnson et al. (2016) apply a 'longevity indicator' to measure the length of time during which a material or production system is retained. Lieder & Rashid (2016) present a general framework for CE from a threefold perspective -- environmental impact, economic profit and social benefit -- in combination with the organisations' business models. Linder & Williander (2017) assess empirically the influence of a series of factors that hamper the implementation of CE business models and establish a typology of customers and customer needs; Ormazabal et al. (2018) evaluate the introduction of EC in Spanish SMEs.

In this framework, Elia et al. (2017) also present a taxonomy of existing indicators to measure CE at the micro-level in the industrial and service sectors. Based on the idea of adapting existing indicators and characterising loop-closing activities, Aranda-Usón et al. (2020) propose the integrated measurement of CE from different perspectives, suggesting that this will contribute to a better understanding of the progressive adoption of CE at the micro-level. These authors define specific interdependent CE actions according to how difficult they are to implement, thus increasing the likelihood that they will adopt SMEs (Katz Gerro & López Sintas, 2019). They also analyse the conceptualisation of CE activities as in line with other authors (Lerner et al., 2013; Zamfir et al., 2017).

However, the literature review reveals that internal processes leading to adopting the CE principles are underexplored. The indicators proposed to date are not providing specific information for the environmental accounting or the actual cost of the material loop-closing, especially if we consider that some CE principles are not exclusively related to profitability criteria, as Azevedo et al. (2017) argued. Thus, it seems relevant to introduce CE-specific accounting criteria based on these arguments, as an under-explored research topic, following an approach that has already been applied to material flow and efficiency (Haupt et al., 2017). In fact, material flow cost accounting (MFCA) methodologies have been adapted to the CE (Zhou et al., 2017), and the integrated systems are applied to evaluate CE based on material flow or to assess life-cycles in sectorial studies (Pauliuk, 2018).

Kristensen & Mosgaard (2020) propose different indicators to measure recycling, remanufacture, disassembly, the extension of life-cycle, or integral waste management and process efficiency. Rossi et al. (2020) analyse accounting-related practices connected with their proposed indicators to measure the three dimensions of sustainability (environmental, economic and social) concerning CE business models. The social value of the CE is another impact analysed through employment (Scarpellini, 2021; Zhao et al., 2017), with an emphasis on the introduction of CE principles and internal accounting. In addition, the measurement of the CE has to include the social dimension because to achieve an environment free of pollution, and the whole community has to be involved in the circular values (Kornberger & Carter, 2010).

Seminal contributions in this area include the approach proposed by Stewart and Niero (2018) to the CE accounting practices by analysing CSR reports qualitatively and addressing a wide range of circular activities undertaken by firms. However, their study does not present activity-specific indicators to measure the scope of CE adopted by businesses. In contrast, Scarpellini et al. (2019) propose an advanced accounting capabilities-measuring model for introducing the CE principles. In summary, these authors analyse the different environmental capabilities that organisations apply to resources to introduce CE, including environmental management systems, corporate social responsibility, sustainability reports, and accountability and other environmental accounting practices. Despite these interesting contributions, to the best of our knowledge, no previous study has addressed the relationship between environmental accounting practices and the CE practices adopted by organisations.

Based on the literature review and these considerations, this study aims to increase our understanding of CE's introduction and examine its relationship with environmental accounting practices introduced in the following subsection.

2.2. Environmental accounting and the CE

In the last decades, the EMAR has become an essential instrument for correctly implementing environmental management policies and has ultimately led to more socially responsible behaviours, and several authors have been paid substantial research attention to CSR (Deegan, 2017; Gray et al., 2018; Gray et al., 2009; Schaltegger & Burritt, 2017). The literature has pointed out existing EMAR practices as a critical factor for firm sustainability (Deegan, 2014; Patten & Shin, 2019; Unerman et al., 2010), and, recently, some authors have approached this topic from a CE perspective (Aranda-Usón et al., 2020).

In recent years, increasing environmental awareness has led organisations to adopt EMAR demonstrating that it is a valuable tool to help implement CE changes. Implementing a CE in firms requires significant managerial and operational changes, leading to new expenses and investments. Thus, activities should be adequately accounted for redesigning products and processes that make more efficient use of resources, recycling or reusing materials and products. Notably, the EMAR allows firms to identify, classify and assign environmental-related costs, which turns it into an important decision-making tool (Adams, 2002; Burritt & Saka, 2006; Contrafatto & Burns, 2013; Cullen & Whelan, 2006; Ferreira et al., 2010; Schaltegger & Csutora, 2012). These practices improve both firms and products (Gibson & Martin, 2004). In contrast to EMAR, conventional management accounting and management control methods incorporate environmental costs to indirect manufacturing costs (Burritt, Hahn, & Schaltegger, 2002), which blurs the firms' environmental practices decision-makers (Burritt, 2004).

The analysis of the EMAR in a CE context is of great interest to introduce new topics of research related to the identification and quantification of costs (Birkin, 2001); life-cycle management and its costs (Bennett & James, 1998; Bierer et al., 2015; Qian & Burritt, 2011; Schaltegger & Burritt, 2010), and the adoption of environmental accounting processes in a circular business model (Marco-Fondevila et al., 2020; Scarpellini et al., 2020).

Similarly, reporting the CE-related activities is essential to maintain the necessary transparency for all policies that purport to be sustainable and socially responsible. Thus, it can b expected that environmental accounting techniques, including management-related ones, will play a relevant role in implementing CE practices in organisations in the short term. Previous studies related to sustainability performance and financial performance indicators (Moneva & Ortas, 2010; Orlitzky et al., 2003) demonstrated the link between environmental reporting techniques and the implementation of sustainable management systems (Adams, 2004; Clarkson et al., 2008). A study developed before the CE was widely introduced. Christ & Burritt (2015) analysed the value of MFCA in terms of flows and costs and concluded that there is no theoretical basis for using this tool, and they argue that its value is limited to large manufacturing firms.

Our research is not specifically theory-driven. However, we approach the relationship between the businesses' circular scope and their EMAR practices as a first theoretical attempt at this topic that is still under development.

Recent studies analyse aspects of accounting in the introduction of CE in organisations from perspectives inspired by resource-based view theory (RBV) and by the evolution of dynamic capabilities (Latan et al., 2018; Scarpellini et al., 2020). Based on this theoretical framework, Aranda-Usón et al. (2019) define and measure different financial resources applied to circular activities and study how they can help firms achieve higher circularity levels. These authors analyse a sample of Spanish companies and find that the availability of funds, the quality of the firms' financial resources and public subsidies encourage CE practices. Portillo-Tarragona et al. (2018) and Scarpellini et al. (2020) analyse environmental management systems, including some variables of EMAR used in eco-innovation and CE, applying the dynamic capabilities theoretical framework. Based on this analysis, they define and measure environmental management systems (EMS) and other management and accounting techniques to implement CE in businesses.

The theoretical approach proposed by the RBV can be considered the most appropriate for the internal measurement of resources and capabilities applied by companies to the adoption of different CE-related activities. Using this theoretical approach, Aranda-Usón et al. (2020) divide the main CE activities into four levels and argue that circular economy-related activities are being introduced progressively. However, few studies have analysed the introduction of CE from the point of view of internal accounting and reporting using the RBV theoretical framework, and this study aims to close this gap.

From another perspective, the institutional theory could explain the organisations' behaviour in a CE context and the related application of different environmental accounting tools (Acerete et al., 2019; Campbell, 2007). In this theoretical framework, DiMaggio & Powell (1983) and Acerete et al. (2019) claim that coercive and normative mechanisms cannot be avoided due to the organisation's authority that promotes them. These mechanisms include legal regulations, technical requirements and behaviour codes promoted by educational bodies (universities), professional bodies, or society (Scott, 1995, 2014). Similarly, cultural-mimetic mechanisms can be argued to shape the behaviour of an organisation through common beliefs, isomorphism, a shared operational logic, and national or sector-specific cultures (Scott, 2014).

Notably, some authors, such as Acerete et al. (2019, 2011), argue that EMAR is determined by institutional mechanisms, such as environmental regulation or pro-environmental policies can lead to different behaviours towards environmental disclosure (Acerete et al., 2011, 2019; Archel, 2003; Criado-Jiménez et al., 2008; Llena et al., 2007). Thus, if we consider that these mechanisms could apply to the recent proposals, regulations and operations developed in a circular model, the institutional theory could partially explain the implementation of EMAR practices to measure the environmental performance (Christ & Burritt, 2013; Ferreira et al., 2010; Latan et al., 2018; Zhou et al., 2017) and the reporting in a circular scenario (Marco-Fondevila et al., 2020). An excellent environmental performance achieved through the implementation of environmental management systems favours applying the principles of circularity in business activities (Kristensen & Mosgaard, 2020; Marrucci, 2019; Scarpellini et al., 2020). In addition, the indicators presented emphasise the role to be played by environmental management accounting in terms of both management and reporting to stakeholders.

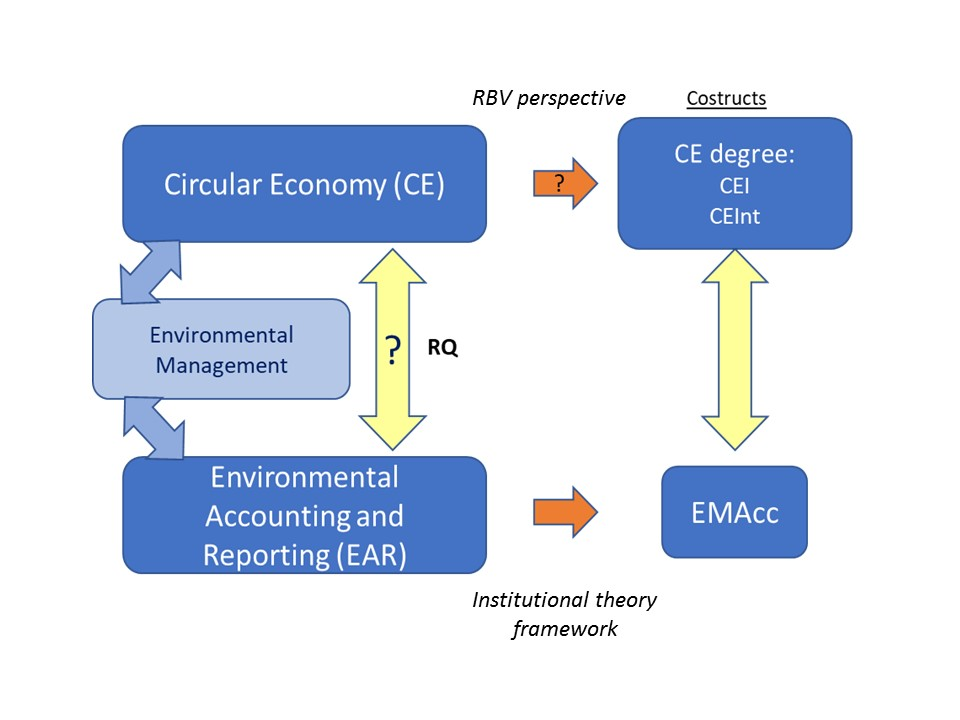

Considering these premises, we study in detail the implementation of EMAR practices from the Institutional theory perspective and the progressive introduction of circular activities in firms using the RBV. Figure 1 explains the model that is developed in the following sections.

Figure 1. Empirical model: CE-related activities and EMAR practices relationship

In summary, our research question is aimed at covering the existing gap regarding the interrelation between EMAR practices and the implementation of CE in company operations:

RQ-: To what extent is there a relationship between the scope of a firm's CE practices and its environmental accounting and reporting?

The following section addresses the empirical methodology proposed to answer the main research question.

3. Methodology

The empirical analysis is based on a survey undertaken with a sample of firms interested in eco-innovation, eco-design and the CE, which took part in a collaborative research project in northeast Spain. The underlying idea was that disseminating environmental information among agents can help promote products, processes, and new management practices and the use of more environmentally-friendly resources and energy (Scarpellini & Romeo, 1999).

Firms that integrate the sample were selected using the SABI database1 with 50 employees or more, considering that size increases the likelihood of adopting cleaner production technologies (Rehfeld et al., 2007; Triguero et al., 2014; Wagner, 2007). These firms were selected because they operate in the sectors defined in the so-called 'BREFs' ("Best Available Techniques")2. Specifically, selected sectors include the industrial, transport and logistics, and waste sectors, whose NACE 09 codes correspond to those of the extractive industry (05-09), the manufacturing industry (10-33), electricity, gas, steam, and air-conditioning supply (35), water supply, sewerage, waste management, and remediation activities (36-39), and transportation and storage (49-53). Although some companies potentially interested in CE-related activities could be excluded from this selection, the sample is considered as representative in line with previous studies ( Rivera-Torres et al., 2015; Scarpellini et al., 2017). Firms that operate in these sectors are under more significant pressure than others to act pro-environmentally and are therefore especially keen to improve their environmental performance and introduce eco-design and CE practices (Ogunmakinde, 2019).

Approximately 1,000 firms met the criteria. They were contacted by email to be informed of the purpose of the study, and they received a survey. A total of 110 responses were forthcoming, 89 of which were regarded as valid for the study. The distribution of these firms by sector is presented in Table 1.

Table 1. Sample distribution by sector

| Sample distribution by economic sector | (no. companies) |

|---|---|

| Food industry | 10 |

| Energy | 4 |

| Waste | 3 |

| Manufacturing | 40 |

| Industrial sector (chemistry, paper, etc.) | 10 |

| Transport/Logistics | 11 |

| Service Sector | 11 |

| 89 |

Although the number of observations is limited, it is worth noting that the survey was not anonymous, and its Tax Code identified each firm. This data was intended to ensure the firms' commitment to the quality of the answers and make it possible to cross the survey results with the firms' characteristics and economic and financial information. The survey was divided into three sections, and the main one dealt with activities directly or indirectly related to closing material loops from a CE perspective. The questions were designed to gather information about implementing specific actions related to the CE (Table 2).

Table 2. Main CE-related activities and the selected variables to measure the intensity of their introduction in businesses

| Activities | Description | Likert | Intensity scale |

|---|---|---|---|

| 01. Energy efficiency | % of equipment or facilities replaced and/or improved for energy efficiency | 0-5 | 0%; From 1 to 10 %; From 11 to 20 %; From 21 to 30; %; From 31 to 40 %; More than 40 %; NA |

| 02. Internal recycling | % of recycling waste within the company itself | 0-5 | |

| 03. Renewable energy | % of processes/equipment replaced and/or improved to exploit renewables | 0-5 | |

| 04. Design for resource efficiency | % of the products’ design or services modified to reduce resource intensity (dematerialisation) | 0-5 | 0%, From 1 to 5 %, From 6 to 10 %, From 11 to 20 %, From 21 to 30 %, More than 30 %, NA |

| 05. Design for resource recovery | % of the products’ design or services modified to increase their recyclability (waste prevention) | 0-5 | |

| 06. “Secondary raw materials” (recycled) | % of resources replaced by other fully recycled materials | 0-5 | |

| 07. Product-life extension | % of the products’ design or services modified to extend their durability and reparability | 0-5 | |

| 08. Design for upgradability and multifunctionality | % of the products’ design or services modified to increase their functions and upgradability | 0-5 | |

| 09. Eco-innovation | % of the company’s total revenue invested in eco-innovation (other activities) | 0-5 | |

| 10. Energy waste recovery | % of total revenue invested in energy valorisation of waste | 0-5 | 0%; From 1 to 10 %; From 11 to 20 %; From 21 to 30; %; From 31 to 40 %; More than 40 %; NA |

| 11. Industrial symbiosis and sharing (or similar) | % of recycling waste in shared facilities with other companies and industrial symbiosis. | 0-5 |

Three constructs have been designed to measure both the level of circularity (CEI and CEInt) and the EMAR practices (EMAcc) and their relationship (Figure 1) to answer the research question,

The eleven CE-related activities selected to address the RQ are used to calculate the 'Index of CE-related activities' (CEI), which specifies the activities introduced by each firm in terms of CE. In addition, the percentage is used to measure the activities' intensity (Table 2) to build the 'Index of CE-related activities intensity' (CEInt), transforming the percentage intervals into a Likert scale as follows:

Index of CE-related activities": \(\textbf{CEI =} \sum_{\mathbf{i = 1}}^{\mathbf{n}} \boldsymbol{Xi}\)

Xi is activity i of CE; values (0,1)

Index of CE-related activities intensity: \(\textbf{CEInt =} \sum_{\mathbf{i = 1}}^{\mathbf{n}}\boldsymbol{Xi \ pi}\)

pi is the weight of each activity measured by the intensity scale.

For EMAR practices, previous studies have shown that the level of environmental or sustainability practices and environmental and sustainability accounting are often related (Llena Macarulla, 2008; Maas et al., 2016; ). Thus, in this study, transparency practices and environmental management, accounting and reporting are measured using the EMAR-related variables listed in Table 3 and based on the literature (Acerete et al., 2011, 2019; Llena et al., 2007; Schaltegger et al., 2008).

Table 3. Environmental and management accounting and reporting practices

| Cod | Practices | Description | Type | Values |

|---|---|---|---|---|

| ENV_TRANSP | Transparency Policy | The company as specific and public transparency/accountability practices | Dichotomic | Yes/No |

| ENV_MEM | CSR Report | Sustainability reports on environmental impact are presented to stakeholders | Dichotomic | Yes/No |

| ENV_ACC | Environmental accounts | Environmental concepts are accounted explicitly for (expenses, provisions, contingencies, assets…) | Dichotomic | Yes/No |

| ENV_EnvINV | Valuation of cash-flows from environmental investments | The company quantifies cash flows concerning environmental investment | Dichotomic | Yes/No |

| ENV_NOTES | Environmental information in the notes to accounts | Environmental entries (costs, provisions…) are detailed in the notes to accounts | Dichotomic | Yes/No |

| ENV_EMS | Environmental Management System | The company follows certified environmental norms or implements certified EMAS | Dichotomic | Yes/No |

| ENV_EMT | Environmental Management Tools | The form uses environmental management techniques (energy, eco-design, LCA, e-footprint) | Dichotomic | Yes/No |

The variables defined in Table 3 integrate the construct 'EMAcc' to measuring the level of implementation of EMAR practices in companies as follows:

\(\textbf{EMAcc} = \sum_{\mathbf{i}\mathbf{=}\mathbf{1}}^{\mathbf{n}}\boldsymbol{EMARi}\)

EMARi Environmental Management Accounting and Reporting activity i; values (0,1)

The measurement, evaluation, analysis and relationship between the constructs are evaluated in the following section. The data was subject to qualitative statistic-descriptive analysis. First, a descriptive analysis of the constructs is carried out independently, and then the statistical and graphic test is carried out to analyse their possible relationships.

The SPSS statistical package has been used to perform the different quantitative analyses. In addition, we use the tools of spreadsheet of Microsoft Excel to elaborate the different figures and descriptive analyses.

4. Main results and discussion

The preliminary descriptive results indicate that all firms, except seven, have undertaken at least one of the eleven CE-related activities (Table 5), albeit without following a precise pattern to adopt CE principles. More than half the firms in the sample have undertaken some of the activities, such as energy efficiency (77.5 %) and eco-innovation (60.7 %). In contrast, the energy valorisation of waste, internal recycling, the exploitation of renewable energy sources or the industrial symbiosis has been undertaken by less than 25 % of the sample (Table 4).

Table 4. CE-related activities rank and intensity introduced by companies

| Activity | n | % | Intensity Average (max 5) |

|---|---|---|---|

| 01. Energy efficiency | 69 | 77.5 | 1.59 |

| 02. Internal recycling | 21 | 19.4 | 0.29 |

| 03. Renewable energy | 18 | 16.7 | 0.25 |

| 04. Design for resource efficiency | 43 | 48.3 | 0.96 |

| 05. Design for resource recovery | 43 | 48,3 | 1.15 |

| 06. “Secondary raw materials” (recycled) | 43 | 48.3 | 0.87 |

| 07. Product-life extension | 41 | 46.1 | 0.91 |

| 08. Design for upgradability and multifunctionality | 35 | 39.3 | 0.99 |

| 09. Eco-innovation | 54 | 60.7 | 0.84 |

| 10. Energy waste recovery | 23 | 25.8 | 0.29 |

| 11. Industrial symbiosis and sharing (or similar) | 22 | 24.7 | |

| CEI (max. 11) | 4.62 (42.0%) | ||

| CEInt (max. 55) | 8.42 (16.5%) |

Eco-design-related actions (activities 4-8) have been implemented by between 40 and 50% of the sample, over 60% of firms undertake four or more activities, and nearly 50% five or more (Table 5). In contrast, 25% of the firms in the sample implement three or fewer CE activities. In addition, although none of the firms in the sample undertakes all listed actions, around 30% undertake seven or more.

Table 5. Number of activities undertaken by companies

| no. of different CE Activities | no. companies | % | ≥ than “n” activities | % |

|---|---|---|---|---|

| 0 | 7 | 7.9 | ||

| 1 | 7 | 7.9 | 1 | 92.1 |

| 2 | 8 | 9.0 | 2 | 84.3 |

| 3 | 12 | 13.5 | 3 | 75.3 |

| 4 | 11 | 12.4 | 4 | 61.8 |

| 5 | 8 | 9.0 | 5 | 49.4 |

| 6 | 10 | 11.2 | 6 | 40.4 |

| 7 | 10 | 11.2 | 7 | 29.2 |

| 8 | 8 | 9.0 | 8 | 18.0 |

| 9 | 5 | 5.6 | 9 | 9.0 |

| 10 | 3 | 3.4 | 10 | 3.4 |

| 11 | 0 | 0.0 | 11 | 0.0 |

| 89 |

The results indicate that firms adopt a fair number of activities without a typical pattern, in line with previous outcomes achieved by Aranda-Usón et al. (2020). This result confirms that the adoption of CE-related principles is still in an incipient stage in businesses, despite Spanish and European authorities' initiatives (European Commission, 2018a; European Parliament, 2015; Government, 2020). In the current situation, firms that have already taken measures to protect the environment must take another step to adopt the broader concept of CE.

The CEInt construct was used to assess the level of intensity with which CE activities were being implemented. Table 4 shows the average intensity values (on a scale from 0 to 5). The intensity values yielded by the sample are, as a rule, fairly low (<1); energy efficiency yields the highest value with 1.59, followed by eco-design multifunction (0.99), dematerialisation (0.96) and eco-design durability (0.91); energy valorisation of waste and exploitation of renewable energy yield the lowest intensity values (<0.3), probably as a result of the legal framework currently in force in Spain (Aranda-Usón et al., 2018; Gimeno et al., 2018).

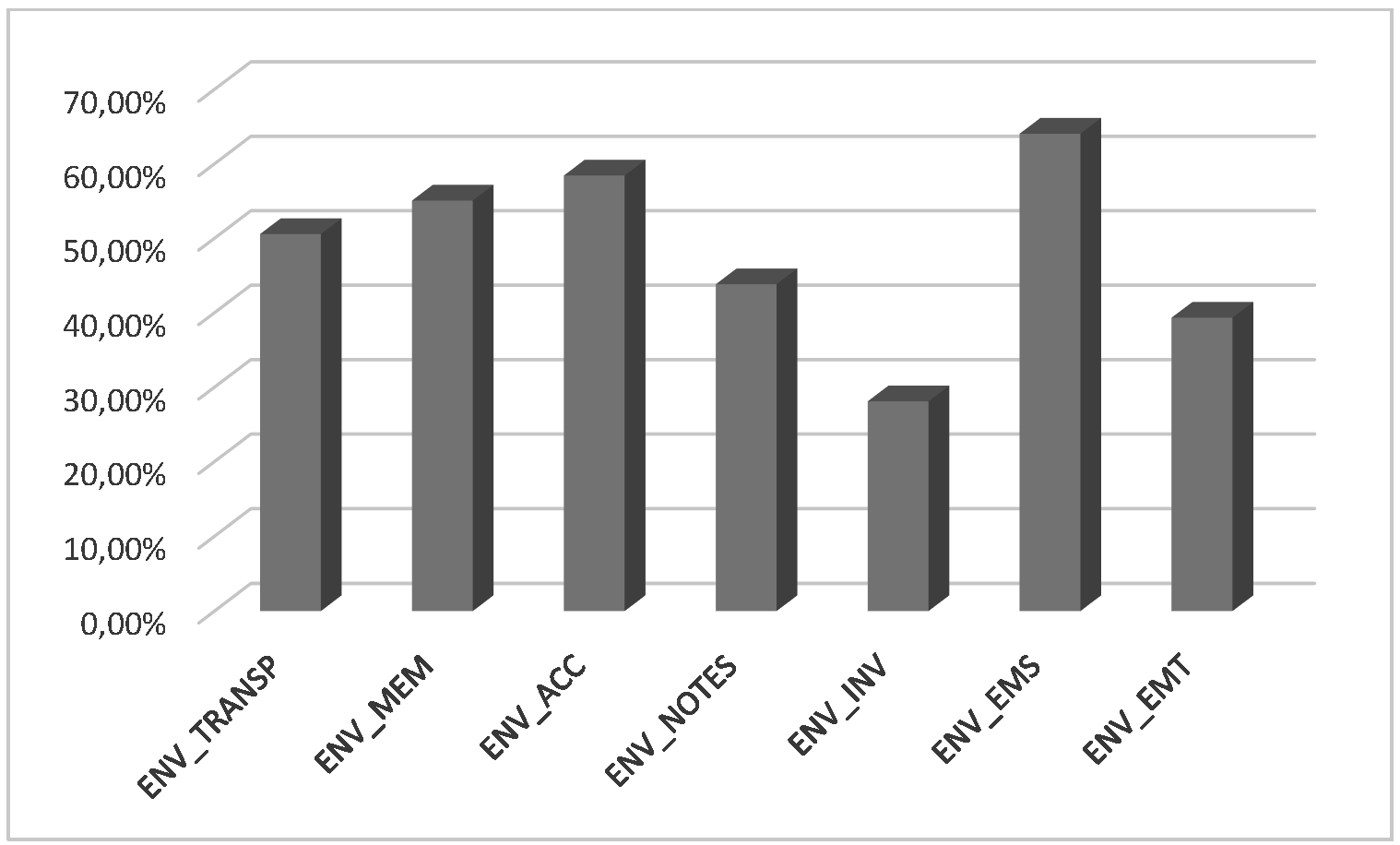

The construct related to the accounting practices (Table 6) illustrates that the level of EMAR is generally low in the sample, with an average value of the number of items presented of 3.39 (48.47%).

Table 6. Level of EMAR practices in companies

| Item | no. | % | |

|---|---|---|---|

| ENV_TRANSP | 45 | 50.56 | |

| ENV_MEM | 49 | 55.06 | |

| ENV_ACC | 52 | 58.43 | |

| ENV_NOTES | 39 | 43.82 | |

| ENV_INV | 25 | 28.09 | |

| ENV_EMS | 57 | 64.04 | |

| ENV_EMT | 35 | 39.33 | |

| Environmental Management Accounting and Reporting | 3.39 (48.47%) |

Specifically, EMAR-related items are observed in less than 60% of the sample (Figure 2). Implementation of environmental management systems (EMS) yields the highest value with 64.04%, followed by the preparation of sustainability reports (MEM), with 55.06%, and public transparency and accountability policies (TRANSP) with 50.56%. Concerning financial-accounting issues, such as the itemisations of environmental costs, provisions and investments are observed in 52 firms (58.43%).

Figure 2. Analysis of EMAR items in companies

In response to the RQ, possible relationships between the CE-related activities and the EMAR practices and the intensity of this relationship were calculated using Student's t (Table 7).

Table 7. t-test of the relationship between EMAR and EC

| CE Index t-Test Independent sample | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Levene’s Test for Equality of Variances | t-test for Equality of Means | ||||||||

| categorised | F | Sig. | t | df | Sig. (2-tailed) | Mean Difference | Sth. Error Difference | ||

| by | |||||||||

| Transparency Policy | σ1 = σ2 | .347 | .557 | -3.084 | 87 | .003 | -1.739 | .564 | |

| CSR Report | σ1 = σ2 | .039 | .844 | -3.508 | 87 | .001 | -1.960 | .559 | |

| Env Accounts | σ1 ≠ σ2 | 4.203 | .043 | -1.516 | 87 | .134 | -.938 | .619 | |

| Env Inv cash flows | σ1 = σ2 | 4.658 | .034 | 0.737 | 87 | .463 | 0.486 | .659 | |

| Env notes | σ1 = σ2 | .278 | .599 | -1.743 | 87 | .085 | -1.025 | .588 | |

| Env Manag System | σ1 = σ2 | .317 | .575 | -1.777 | 87 | .079 | -1.080 | .608 | |

| Env Manag Tools | σ1 = σ2 | .050 | .823 | -0.932 | 87 | .354 | -0.564 | .605 | |

| EMAcc (>= 3) | σ1 = σ2 | .023 | .881 | 3.301 | 87 | .001 | 1.955 | .592 | |

| EMAcc (>= 4) | σ1 = σ2 | .859 | .357 | 2.963 | 87 | .004 | 1.677 | .566 | |

| EMAcc (>= 5) | σ1 = σ2 | .859 | .357 | 2.963 | 87 | .004 | 1.677 | .566 | |

The results of the t-test3 suggest that firms that implement more developed EMAR practices also show a higher range of CE-activities (CEI). The only significant difference observed in the EMAR construct concerns the implementation of circularity practices among firms that publish a transparency policy and CSR report and those that do not (Table 7).

Table 8. t-test of relationship intensity between EMAR practices and of CE-related activities in companies

| CE Intensity t-Test Independent sample | ||||||||

|---|---|---|---|---|---|---|---|---|

| Levene’s Test for Equality of Variances | t-test for Equality of Means | |||||||

| F | Sig. | t | df | Sig. (2-tailed) | Mean Difference | Sth. Error Difference | ||

| Transparency | σ1 = σ2 | .076 | .783 | -1.975 | 87 | .051 | -2.597 | 1.315 |

| CSR Report | σ1 = σ2 | .022 | .883 | -2.323 | 87 | .023 | -3.046 | 1.311 |

| Env Accounts | σ1 = σ2 | .965 | .329 | -1.505 | 87 | .136 | -2.026 | 1.346 |

| Env Inv cash flows | σ1 = σ2 | .329 | .568 | 1.074 | 87 | .286 | 1.595 | 1.486 |

| Env notes | σ1 = σ2 | .037 | .847 | -1.549 | 87 | .125 | -2.070 | 1.336 |

| Env Manag System | σ1 = σ2 | .051 | .821 | -2.057 | 87 | .043 | -2.814 | 1.368 |

| Env Manag Tools | σ1 = σ2 | .714 | .400 | -0.413 | 87 | .681 | -0.568 | 1.375 |

| EMAcc (>=3) | σ1 = σ2 | 2.184 | .143 | 3.506 | 87 | .001 | 4.667 | 1.331 |

| EMAcc (>= 4) | σ1 = σ2 | .361 | .549 | 1.990 | 87 | .050 | 2.617 | 1.315 |

| EMAcc (>= 5) | σ1 = σ2 | .361 | .549 | 1.990 | 87 | .050 | 2.617 | 1.315 |

Table 8 presents the Student's t-test for variable CEInt, which reveals the weight of CE practices. These results are similar to those yielded by CEI variables, although in this case, the implementation of EMS seems to have a significant effect on CEInt (Table 8). Therefore, the performance of EMS could favour the development of more CE activities and help the closing of circles. In addition, the obtained results are line with the results obtained by other studies such as those of Portillo-Tarragona et al. (2018) for the interrelation between EMS and eco-innovation; or the analysis developed by Shih et al. (2018) focused on the between EMS with eco-innovation in circular agri-business.

In summary, we observe that the companies that implement 3 EMAR practices or more have a higher level of circularity measured by both CEI and CEInt (Tables 7-8).

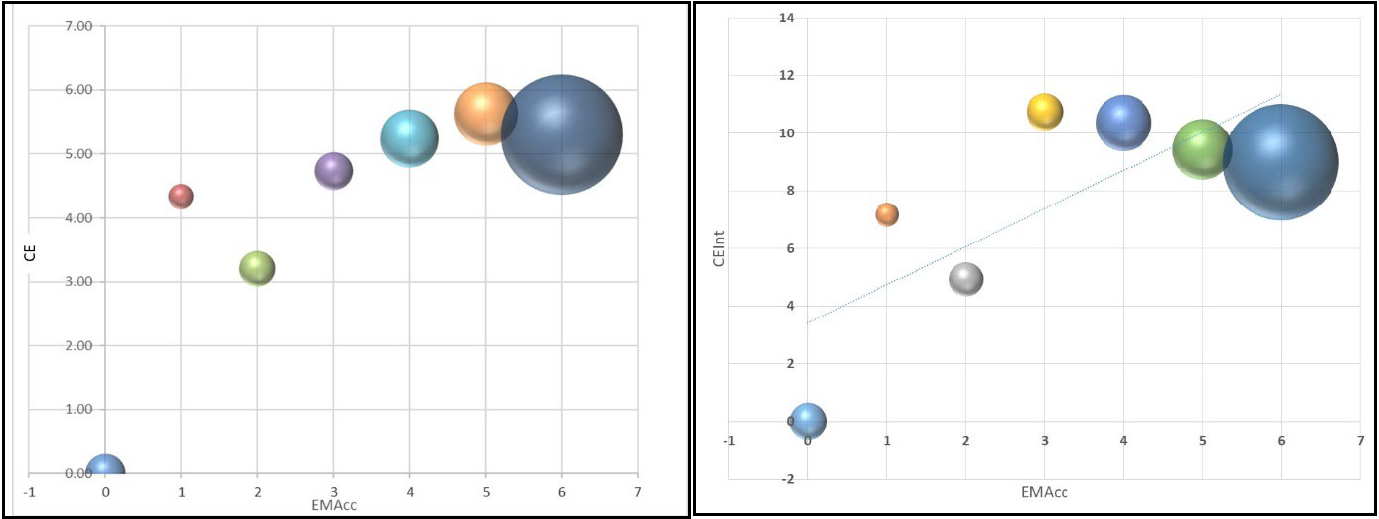

The preliminary statistic-descriptive analysis yields a moderate correlation (0.354) between the CE index (CEI) and the environmental management and accountability index (EMAcc) (significance 0.01). The correlation between the intensity of CE and EMAcc is somewhat weaker (0.266, sig 0.05). The correlations are moderate but statistically significant (Table 9), in line with Scarpellini et al. (2020) between several EMS tools -including environmental management accounting- and circular eco-innovation.

Table 9. Pearson’s correlation coefficient

| Pearson correlation | p-value | |

|---|---|---|

| CEI - EMAcc | 0.354 | 0.001 |

| CEInt - EMAcc | 0.266 | 0.012 |

Figure 3 shows the correlation between CEI and EMAcc. The size of the bubbles reflects the average size of firms in terms of the workforce for each of EMAcc's seven levels, which suggests that larger firms tend to have more developed EMAcc and CEI. These results are similar to previous studies, meaning that size is a significant variable in sustainability practices (Llena et al., 2007; Marco-Fondevila et al., 2018).

Figure 3. Relationship between CEI and EMAcc, and between CEInt and EMAcc weighted by the companies' size

It can be argued that the EMAcc and CE index are moderately correlated, which means that companies with a higher EMAcc index tend to undertake more CE-related activities in the application of the RBV framework. Different firms' resources and capabilities favour more circular behaviours, as demonstrated by other authors (Aranda-Usón et al., 2019; Scarpellini et al., 2020). Thus, the firms' size also seems to be a significant variable in circularity. The larger the firm, the greater degree of the CE, although statistical correlation tests in our study do not corroborate this result. Based on these results, we can emphasise the need to continue investigating the relationship between the scope of circularity and the intensity of CE practices, which must be analysed jointly.

As general considerations, the recent enactment of UE directives (European Commission, 2015, 2018b; European Parliament, 2015; Government, 2020), and the adoption by member states of the European Green Deal (European Comission, 2019) could contribute to implementing policies conducive to closing material loops at the micro-level. The progressive implementation of CE practices suggests that regulations could also play an essential role in triggering imitative behaviours among firms operating in similar geographical or economic environments, in line with an Institutional theory framework (DiMaggio & Powell, 1983; Higgins & Larrinaga-González, 2014; Scott, 2014). In addition, the role of specific mediating instruments could be explored to link technical processes for the material loops closing to the CE mobilising capital budgeting decisions (Miller & O'Leary, 2007).

5. Main conclusions

This study increases our understanding of the internal measurement of CE-related activities in firms from an environmental accounting perspective for the use of EMAR practices as tools in a circular model.

Our results present a novel perspective of environmental accounting practices in a CE context based on a double theoretical perspective. This study reveals that incorporating increasingly intensive CE practices is supported by implementing a more significant number of EMAR practices, such as EMS, transparency policies, CSR report disclosure. However, the results indicate that the level of implementation of EMAR practices is still low and is mainly related to financial, environmental accounting and, to a lesser extent, to other environmental management tools from a circular perspective. Therefore, the application of the Institutional theory to this topic needs to be investigated in future studies. Even though some EMAR practices are applied, they are not implemented to meet the targets on non-financial reporting and the CE implementation promoted by the EU and other national and international institutions.

Although this study is not specifically theory-driven, for academics, the institutional mechanisms such as new regulations and norms or mimetic isomorphism seem to explain some accounting practices adopted by firms in a CE model. These considerations also represent an input for policymakers to define specific plans for introducing particular rules for reporting in a CE context at the micro-level.

From another perspective, RBV allows analysing more circular behaviours of companies since resources and capabilities could increase the CE-related activities adoption significantly. Greater levels of implementation of CE and related practices (e.g. EMAR, LCC, MFCA and other tools to measure material flows) at the micro-level is likely to increase the scope of circularity-related accounting, as one of the main contributions of this research.

This paper presents a broader perspective for practitioners than previous studies on CE measurement and its relationship with environmental accounting and reporting. By creating three measuring indices, the relationships between the CE practices and environmental accounting and management can be measured and dimensioned to fill a gap in the literature related to the lack of specific indicators to specifically account for the closing of material loops at a micro-level. In addition, it can be stated that firms should focus on the accounting of internal CE-related activities and then move to adopt environmental accounting practices based on a circular approach.

Limitations of this study are mainly related to measuring an incomplete range of CE-related activities and the set of the environmental accounting and management practices that could be applied to the CE by businesses. The number of companies that integrate the sample is also limited as the geographical scope of this study. These limitations are partially offset by a large amount of data available, including some variables that are rarely considered in CE-related studies at the micro-level.

Future studies would have to consider financial-economic and social variables concerning CE adoption by businesses and their implications in terms of environmental accounting because the introduction in businesses of concepts related to the CE and decoupling will foster the debate about the measurement of monetary value vs physical economy value in the framework of sustainability.