Impact of curricular internships in accounting on university students: an empirical study in Spain

ABSTRACT

Various organizations, commissions and committees highlight the importance of teaching future accounting professionals through the combination of theoretical training and professional practice. The university must guarantee an accounting profession through graduates who can respond to the needs and global changes of the society. Curricular internships, conducive to experiential learning, allow the student to integrate classroom learning with professional practice, as well as to translate abstract theoretical concepts into reality. An increasing number of universities include the subject of internships within their curricula. All of this makes it interesting to analyse the impact these internships have on university students. This article presents, through factor analysis and the technique of structural equations, a model that comprehensively evaluates the impact of curricular internships in the accounting field on students. The information necessary to estimate the model was obtained through a questionnaire presented to students at the end of their internship period. The survey was completed by 279 students belonging to the Degrees in Business Administration and Management and in Economics at the Autonomous University of Madrid.

Keywords: Higher education; Accounting education; Curricular Internships in Accounting; Integral Evaluation; Curricular integration; Structural equations.

JEL classification: A22; I2; M4.

Impacto de las prácticas curriculares en contabilidad en los estudiantes universitarios: un estudio empírico en España

RESUMEN

Diversas organizaciones, comisiones y comités destacan la importancia de la enseñanza de los futuros profesionales de la contabilidad mediante la combinación de la formación teórica y la práctica profesional. La universidad debe garantizar una profesión contable a través de graduados que puedan responder a las necesidades y cambios globales de la sociedad. Las prácticas curriculares, propicias para el aprendizaje experiencial, permiten al estudiante integrar el aprendizaje en el aula con la práctica profesional, así como trasladar a la realidad conceptos teóricos abstractos. Cada vez son más las universidades que incluyen la asignatura de prácticas dentro de sus planes de estudio. Todo ello hace interesante analizar el impacto que estas prácticas tienen en los estudiantes universitarios. En este artículo se presenta, mediante análisis factorial y la técnica de ecuaciones estructurales, un modelo que evalúa de forma exhaustiva el impacto de las prácticas curriculares en el ámbito contable sobre los estudiantes. La información necesaria para estimar el modelo se obtuvo a través de un cuestionario presentado a los estudiantes al final de su período de prácticas. La encuesta fue cumplimentada por 279 estudiantes pertenecientes a los Grados en Administración y Dirección de Empresas y en Economía de la Universidad Autónoma de Madrid.

Palabras clave: Educación superior; Educación contable; Prácticas curriculares en contabilidad; Evaluación integral; Integración curricular; Ecuaciones estructurales.

Códigos JEL: A22; I2; M4.

1. Introduction

Interest in the academic training of future professionals in the accounting field has been steady from the eighties to the present. Higher accounting education, as Beaver pointed out in 1987, results from the interrelationship between research, teaching and business practice. Several organizations, committees and commissions (AAA, 1986; AECC, 1990; IFAC, 1994) have addressed the global challenges of accounting education. The emergence of global economies and markets has emphasized the importance of international accounting education and practice (Rezaee et al., 1997). The well-known Bedford Report, Future Accounting Education: Preparing for the Expanding Profession, already referred to the need for a change in the accounting teaching process and indicated the importance of students doing internships in the professional field, recommending that they form part of the curricula of teachings related to the accounting field (AAA, 1986). In July 2012, the American Accounting Association (AAA) together with the American Institute of Certified Public Accountants (AICPA) created the Pathways Commission to study the future structure of higher education in relation to the accounting profession. This Commission published the report Charting a National Strategy for the Next Generation of Accountants (Pathways Commission, 2012). Special emphasis was placed on the need to educate future professionals, combining their theoretical training with professional practice. To achieve this combination of theory and practice, this Commission sought to achieve, among others, the objectives of integrating professional guidance into educational programmes and fostering the relationship between teachers and professionals (Bruce et al., 2012). Therefore, the university cannot stay out of the workplace and must guarantee an accounting profession by developing graduates who respond to global needs and changes (Evans et al., 2010). To remain competitive, it is essential that the accounting curriculum provides opportunities for students to develop a broad set of knowledge and skills aligned with the new emerging requirements of this professional role (Dean et al., 2020).

The incorporation of professional internships within the curricula of universities (also called curricular internships), on the one hand, contributes to adequate training of students with a view to their future incorporation into the professional world. On the other hand, internships favour a greater alignment between the knowledge and skills acquired in the academic world with the demands of the labour market and social demands. Curricular internships are a relevant part of the students' training process since they enrich student training by complementing academic learning (theoretical and practical) with experience in work centres (Zabalza, 2011). Hite & Bellizi (1986) affirm that the most common benefit of internship attachments for students is providing a valuable learning experience that complements their coursework. In addition, these types of work-based learning experiences can be effective in achieving more complete education (Farinelli & Mann, 1994) by complementing academic work. As practice requires direct learning from students, it engages them as active mediators of their own learning (Wynd, 1989). Likewise, it has been argued (Coleman, 1976) that these empirical methods increase student motivation (Beard & Morton, 1998) and lead to a greater sense of achievement and self-efficacy (Bernstein, 1976) and a greater sense of responsibility in their future professional development (Williams, 1990). In short, carrying out internships in companies allows students to integrate classroom learning with professional practice, as well as to translate abstract theoretical concepts into reality (O'Hara & Shaffer, 1995; Ciofalo, 1988; Nevett, 1985).

In Europe, to harmonize different university systems, the European Higher Education Area (EHEA) was created in 2001. This supposed a new ordering of official university teachings with special emphasis on carrying out curricular internships by university students. Due to this change in regulations, the incorporation of curricular internships in university degrees is increasingly common. In Spain, as set out in current regulations (art. 3 of Royal Decree 592/2014, of July 11), it is considered essential and mandatory to carry out curricular internships by university students. The main objective is, on the one hand, to allow students to apply and complement the knowledge acquired in their academic training through the acquisition of skills. On the other hand, it facilitates access to the labour market. A large number of educational institutes are coming to the opinion that internship programmes are excellent for the career and professional preparation of students (Anjum, 2020). Furthermore, as stated by several authors (Swift & Kent, 1999; Hodgson, 1999; Cook et al., 2004; Cable & Healy, 2007; Lam & Ching, 2007), internship programmes are rewarding to students, educational institutes and employers. In this sense, it is interesting to analyse the impacts that the inclusion of professional internships within the curricula of the degrees has: on the students who perform them, in the organizations where they are carried out and in the university that offers them.

Therefore, the objective of this paper is to analyse the impact that carrying out curricular internships related to Accounting1 has on students of the Degree in Business Administration and Management (BAM) and Economics (ECO) of the Faculty of Economic and Business Sciences (FEBS) of the Autonomous University of Madrid (AUM). Through a questionnaire completed by 279 students, a model is presented using the structural equations technique, which shows the comprehensive evaluation of the impact that curricular internships have on i) learning in terms of skills (generic and specific), ii) reflection of the learning acquired through the realization of reports, and iii) the elucidation of the choice of the future professional career within or outside the accounting field. The results obtained are interpreted through the theory of experiential learning (Kolb, 1984, 2014; Raelin, 1997). The estimated model shows that the development of the practices had an impact on the acquisition and development of skills, as well as on the crystallization of the future professional. However, students do not perceive that the realization of memory encourages them to reflect on learning.

The structure of the remainder of this article is as follows. After this brief introduction, Section 2 and 3 provide the theoretical framework and the context. Section 4 explains the materials and methods employed. Section 5 presents the results obtained, and finally, the last section presents the main conclusions that can be drawn from this study.

2. Theoretical Framework

2.1. Previous studies

There are several studies that analyse the impacts of accounting internships for students, the organization in which they are carried out, and the university that offers them (Cable & Healy, 2007). Next, this section focuses on the impact of the internship on students.

Taylor's (1988) article analyzed three hypotheses concerning the effects of college internships on individual participants: (a) greater crystallization of vocational self-concept and work values, (b) less reality shock, and (c) better employment opportunities. The study is based on the premise that internships can help students to crystallize their vocational self-concept by facilitating the identification of vocationally relevant skills, interests and values (Hall, 1976). In other words, the completion of internships helps clarify decisions about the choice of professional career and assists in their transition to professional life (Tay & Teo, 1995). The work of Cable & Healy (2007) presents some studies on the impacts of accounting internships on students. According to Burnett (2003), internships are one of the learning methods that are most heavily promoted in accounting programmes. In this work, a survey of accounting practitioners regarding undergraduate accounting education was conducted. The practitioners overwhelmingly ranked three- to four-month internships as the most effective outside learning activity. O'Shaughnessy & Naser-Tavakolian (2000) concluded that accounting internships improved the subsequent academic performance of undergraduate students. Their research suggests that the skills, knowledge, and motivation that students gained from their internship experience had a significant positive impact on their performance in subsequent business courses.

In 2008, Beck & Halim conducted an exploratory study to determine the impact of internships on accounting students. This study is centred upon the business attachment (internship) programme for accounting students at one of the universities in Singapore. To carry out their research, they analysed the impact on i) the identification of what the interns have learned in terms of professional skills; ii) the elucidation of the ways in which the students have learned from the experience; and iii) the determination of whether the experience has helped the students make their choice of careers. The methodology used qualitative data, quantitative analysis, and hypothesis testing. The sample consisted of 250 accounting students from a Singapore university who had completed eight weeks of internships at the end of the second year of a three-year degree programme. Previously, the university and the host organization agreed on the work plan to be developed by the student during the internship. An academic tutor and a professional tutor were involved in the work plan. In addition, the students had to write in a diary or logbook those events that they considered had provided them with significant learning and finally submit a report detailing what they had learned. The theoretical framework for the explanation of the results obtained was based on experiential learning (Kolb, 1976, 1984), as well as on Goleman's (1995) theory of emotional intelligence. The results obtained from the study concluded that personal and interpersonal skills were the most significant learning outcomes acquired by students. Of lesser importance were technical skills. Furthermore, the undergraduate perceived that what they had learned would support their future professional development and that the internship had prepared them for their first job and helped them choose their career.

The work of Muhamad et al. (2009) examines interns' perceptions of selected issues relating to internship attachment before and after internship attachment. The issues were focused on what interns have learned, the process by which they learned, the effect of what has been learned on their expectations of their future profession, and choices of their future career. To carry out their research, 156 students who were involved in internship attachment for the academic session of 2007/2008 completed a questionnaire. Most of the interns performed their internship attachment in accounting/auditing firms. In terms of location, 68.6% of interns chose to do their internship in Kuala Lumpur/Selangor. The main conclusions drawn from their work show that, in general, the interns perceive the internship attachment as not able to give them the expected benefits. However, the internship is regarded as successfully providing guidance to them in choosing their career path as well as in enhancing their knowledge of public sector accounting.

More recently, Anjum's work (2020) evaluated the impact of internship programmes on the professional and personal growth of business students in Pakistan. To do this, through a questionnaire, they analysed the impact on i) professional development, ii) professional skills, iii) personal growth of business students and iv) personal capabilities of business students. The study data comprise 800 business administration students from 4-year degree programmes from 15 Pakistani universities. The results of the study showed that internship programmes had an impact on the professional growth and skills of the business students of Pakistan, affecting their personal development, skills, and capabilities.

2.2. The Theory of Experiential Learning

Experiential learning is increasingly important as a methodological strategy to face new training demands, focused on the development of competencies and the promotion of the ability to learn to learn. The growing interest in finding new ways of teaching and learning that promote the development of competencies justifies the special attention that is being paid to the integration of learning experiences outside the classroom. Experiential learning offers a unique opportunity to connect theory and practice since it allows the transfer of knowledge from the academic world to the professional reality of students (Romero Ariza, 2010).

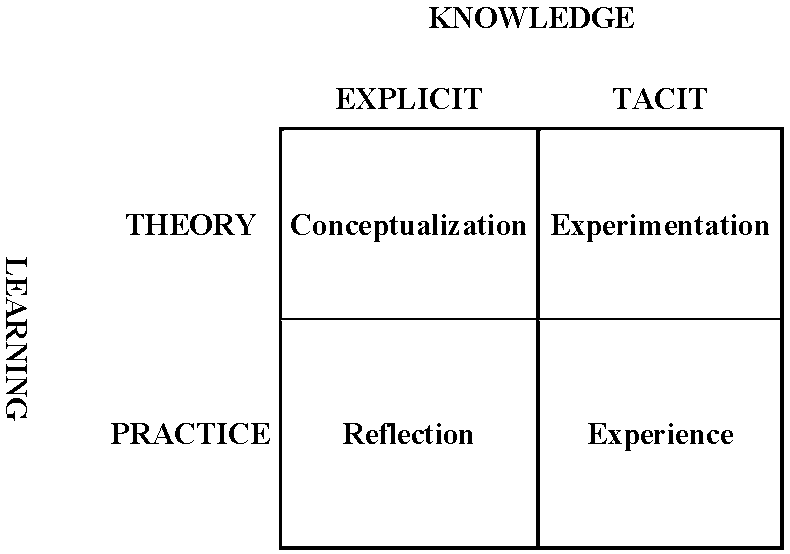

Several authors over the years have developed different models to explain the theory of experiential learning. Dewey (1938) addressed this aspect of experiential learning when he conceptualized experience as an organizing focus for lifelong learning and development. For Dewey, true education is achieved through experience. For him, experiential learning is active and generates changes in the person and in their environment. In other words, it not only goes "inside the body and soul" of the learner but also uses and transforms the physical and social environments to extract what contributes to valuable experiences and thus establishes a strong link between the classroom and the community (Díaz Barriga, 2003). Dewey's work, along with the insights of others regarding necessary cognitive, affective and environmental conditions needed for adults to constructively and effectively learn, such as those later identified by Knowles (1980), supports Kolb's assertion (1984) that learning should be defined as a process whereby knowledge is created through the transformation of experience (Yardley et al., 2012). Kolb, in 1984, proposed a model where the individual takes and understands the information of the experience (concrete experience and abstract conceptualization) and transforms it (reflective observation and active experimentation), that is, interprets and acts based on that information. Kolb (2014) identifies experiential learning as the method that offers a framework within which the links between education, work and personal development are strengthened. That is, on the one hand, experiential learning addresses the skills that the workplace demands and, on the other hand, responds to educational objectives, which allows for the integration of work within the classroom with the real world. Likewise, the author recognizes that students integrate real-world experiences into their personal worlds by interpreting their experiences and giving personal meaning to plan new actions. For this author, internships, among others, are educational strategies and/or spaces that promote experiential learning (Gleason and Rubio, 2020). In 1997, Raelin presented a comprehensive model of learning based on work (Figure 1), which allows for us to understand the totality of its dynamics, that is, how learning is produced and transferred at work. This model contemplates four types of learning that are similar and compatible with the learning styles proposed by Kolb. In this model, explicit and implicit forms of knowledge are combined, as well as theoretical and practical learning, at the individual and collective levels.

Figure 1. Model of learning based on work at individual level.

Conceptualization refers to the underlying theory concerning the performance of the internship, materialized in explicit knowledge (which can be expressed verbally). Through experimentation, the initial conceptual knowledge of the student may be seen to be modified, acquiring tacit knowledge, and epistemic component that cannot normally be manifested orally and which is profoundly rooted in the action and the participation in a specific context, susceptible to being used in the resolution of problems and in adopting rational decisions in new situations. After the experience, the tacit knowledge is reinforced, but reflection is necessary so that the tacit knowledge inherent in the experience may come to the surface, and therefore be explicitly stated.

In addition, Raelin affirms that one of the tools that can help students who carry out internships to reflect more on their individual development is the daily. Writing daily gives participants, the opportunity to break out of their habitual ways of thinking and do so through reflective withdrawal and re-entry (Raelin, 1997).

Itin (1999) also proposed what has been called the diamond model, which integrates the phases of experiential learning proposed by Dewey as well as a framework of multidirectional "environment-educator learner" interrelationships. This author describes experiential learning as a formative process in which the individual is physically, socially, intellectually, cognitively, and emotionally involved through a concrete experience.

However, there is currently no consolidated or widely accepted theoretical framework to explain experiential learning (Romero Ariza, 2010). Recently, some authors (Chisholm et al., 2009) have tried to establish a conceptual model for the systematic study of learning linked to the performance of professional tasks (work-based learning). To do this, these authors reviewed different previous theories on experiential learning, using the model proposed by Dewey in 1938 and later taken up by Itin in 1999 as a starting point.

3. Context

3.1. European Higher Education Area: Lifelong and Competence-based learning

The Bologna Declaration, an agreement signed in 1999 by the ministers of education in the European Union in the Italian city of Bologna, led to the creation of the EHEA, whose main purpose was the harmonization of different university systems, which served as a framework for reference to the educational reforms that many countries were to initiate in the early years of the twenty-first century. One of the main measures contemplated within the EHEA was the change in teaching methodologies aimed at lifelong and competence-based learning. The adaptation of education systems to the needs of today's society has made competence-based learning firmly established in european and international educational policies (Calabor et al., 2018). The EHEA model raises skills as a central element that the student must acquire during their training period. Royal Decree 1393/2007 on the Organization of University Teaching modified by different regulations (RD 861/2010, RD 96/2014, RD 43/2015) and the European Framework for Higher Education Qualifications (Royal Decree 1027/2011) incorporated references to two types of competencies in university teaching: i) specific competences related to knowledge, skills and attitudes within a specific subject or discipline and ii) generic or transversal skills that are related to personal development and do not depend on a specific thematic or disciplinary area but rather penetrate all domains of professional and academic performance. These types of skills must be closely linked to the social and labour demands of the current market, which is why they are increasingly important in university education (Acebrón, 2008; UNESCO, 2013; Martínez & González, 2018). The consensus opinion is that university courses can no longer be entirely content-driven and limited to specific technical skills. If graduate students are to succeed as knowledge professionals in a highly changeable global business environment, they must exhibit a range of technical and generic skills (De Lange et al., 2006). However, as mentioned, the EHEA model not only contemplates competence-based learning but also lifelong learning. The model proposed by Kolb on experiential learning can serve to understand part of the methodological keys that form the basis for developing the European model of lifelong learning. The skills and attitudes learned through this experimental approach help individuals be professionals committed to lifelong learning and the development of the person (Schön, 1998), that is, responsible for their own lifelong learning and performance (Hicks, 1996). One of the subjects that promotes experiential learning is curricular internships (Kolb, 2014). By their very definition, through experience, these internships allow the student to exchange between the academic and professional world, thus developing the transversal and specific skills of the degree.

The current context of Spanish universities in terms of "curricular internships" is presented below.

3.2. Curricular internships in Spain

Since the beginning of the 20th century, Cooperative Training Programs or Work Integrated Learning have been developed in advanced economies, with a notable expansion of these to all industrialized countries in the 70s and 80s, especially in America, Europe and Oceania (Durán et al., 2015).

In these Cooperative Training Programs, university students normally and alternately develop their studies between the university and a company as a result of an agreement signed between both parties, in order for the company to participate in the specialized and practical training of students. In this way, they will obtain a well-rounded training, the result of the combination of theoretical knowledge with others of a practical nature relating to their future profession and join the professional world at the conclusion of these Programs with minimal experience (Royal Decree 1497/1981).

In Spain, curricular internships in accounting are carried out mainly by students who are studying in the bachelor's degrees in BAM and in Finance and Accounting (FA), as well as in ECO. These degrees in Spain are assigned 240 European credits and are studied over four years, differing from the general trend of degrees in the field of Business and Economics in European universities. In Europe, these degrees are achieved with the passing of 180 (ECTS) European credits and have a duration of 3 years (Rodríguez Ariza, 2002).

3.2.1. Regulatory framework

As mentioned in the Introduction, RD 592/2014, from July 11, is the regulation that regulates the external academic internships of university students in Spain. The main aspects taken into account in the development of the internships are detailed below:

- Objectives pursued:

As stated in article 3 of this Royal Decree, with the completion of external academic internships, it is fundamentally intended to achieve the following purposes: i) contribute to the comprehensive training of students by complementing their theoretical and practical learning and contrasting and applying knowledge acquired from business reality, ii) encourage the development of technical, methodological, personal and participatory skills, and iii) obtain practical experience that facilitates insertion into the labour market and improves future employability.

- Modalities:

There are two types of external academic internships: curricular and extracurricular. Curricular internships are configured as academic activities that are part of the Study Plan in question. On the other hand, extracurricular internships are those that students can carry out on a voluntary basis during their training period and that are not part of the corresponding curricula.

- Work plan and evaluation:

To carry out external internships, students will have a tutor from the collaborating entity and an academic tutor from the university. The student, to successfully complete her internship, must submit a final report2 to her academic tutor, who will be in charge of evaluation. The structure of the report must present the following aspects: a) personal data of the student; b) collaborating entities where they have carried out the internships and locations; c) specific and detailed description of the tasks, work carried out and departments of the entity to which they have been assigned; d) assessment of the tasks carried out with the knowledge and skills acquired in relation to university studies; e) list of the problems raised and the procedure followed for their resolution; f) identification of the contributions that, in terms of learning, the internships have provided; and g) evaluation of internships and suggestions for improvement.

With respect to the duration and weight of external internships, according to article 12 of RD 1393/2007 of October 29, these will have a maximum extension of 25 percent of the total credits (hours) of the degree. In addition, it recommends that they be offered preferably in the second half of the degree program.

3.2.2. COOPERA Program at the UAM

In the 1985-1986 academic year, the UAM launched the precursor Educational Cooperation Program in Spain, sponsored by the Fundación Universidad-Empresa and the Círculo de Empresarios. This project attempted to bring the studies of the FEBS in line with the levels of quality and social integration achieved by other university centers in countries with a higher economic and educational development. Initially, it was called the Educational Cooperation Program, but considering that at present Cooperative Training Programs are entered into for the performance of all external internships for university students, the first is referred to as COOPERA (Durán et al., 2015).

COOPERA3 is aimed exclusively at students during the last two years of the bachelor's degrees in BAM and ECO from the FEBS of the AUM (this university does not offer the Bachelor's Degree in Accounting and Finance). This programme is a pioneer in the alternating training model, characterized by combining the student's training periods between the company and the university. Access to COOPERA is competitive and therefore an Admissions Committee intervenes to analyze the applications, in which the academic record, level of English, command of other languages, motivation letter and other curricular merits are especially valued, and there is also a personal interview.

The external internships carried out by its students are curricular, compulsory and last eight months. To implement a teaching system that allows its students to develop their training in the best possible conditions, from September 1 to July 30 of the two courses included in the Program, students will alternate the time dedicated to the university and the company according to the following calendar:

Table 1. Internship schedule

| Cuatrimestre 1 | Cuatrimestre 2 | Cuatrimestre 3 | |

|---|---|---|---|

| 3rd year | Teaching | Internships | Teaching |

| 4th year | Internships | Teaching | Teaching |

The internships are allocated 24 ECTS (equivalent to 480 hours) of the total of the BAM and ECO degrees. At the end of the second period, in the fourth year, the students' practices are evaluated by the academic and professional tutor. The writing of the internship report (70%) and the periodic monitoring of their performance (10%) are scored by the academic tutor. The evaluation by a professional tutor carrys a weighting of 20% of the final grade.

It is worth mentioning the high quality of company internships in different professional areas (accounting, auditing, finance, etc.) of the COOPERA Program. Each academic year, an average of 20 companies from different economic sectors participate. These companies financially remunerate internship students at approximately 700 euros gross per month.

4. Research method

In line with several of the premises analysed in previous studies presented and aligned with the model proposed by Raelin (1997) and the current regulations on curricular internships followed by a Spanish university (AUM), the objective of this work is to comprehensively evaluate the impact of carrying out curricular internships related to accounting in BAM and ECO students from the FEBS of the AUM. To do this, a model is presented using the structural equations technique, which provides a comprehensive evaluation of the impact that curricular internships have on i) the identification of what they have learned in terms of generic or transversal skills, ii) the identification of what they have learned in terms of specific skills (accounting), iii) reflection of the learning acquired through the realization of the report, and iv) the elucidation of the choice of future professional career within or outside the accounting field.

4.1. Material and method

4.1.1. Questionnaire

The information necessary to achieve the objectives of this work was obtained through a questionnaire (Appendix 1) presented to students at the end of their internship periods. The survey consists of approximately 50 Likert-type items, each rated on a five-point scale (1 = strongly disagree, 5 = strongly agree) and is divided into nine sections. The first includes demographic data and the activity carried out in the internships. The second includes questions on general and accounting training related to the preparation of the report. In the third and fourth sections, students' perception of the development of generic or transversal and specific competencies developed, respectively, is requested. The fifth and sixth sections request opinions to identify the positive aspects and those for improvement. Finally, in the seventh, eighth and ninth sections, questions are asked about the contribution of internships in elucidating the choice of future professional careers.

The generic or transversal skills (question 3 of the questionnaire) were selected and summarized from the information provided by the teaching guides of the Internship subjects of the BAM and ECO degrees of the FEBS of the AUM. Furthermore, as these skills are related to personal development and are closely linked to the social and labour demands of the current market, in turn, we classify them (Table 2): i) "ethical commitment"; ii) "learning capacity and responsibility"; iii) "communication skills"; and iv) "teamwork" (Freixa et al., 2012).

Table 2. Relationship between general or transversal skills of the degree and personal skills required by the professional world

| GENERIC OR TRANSVERSAL SKILLS OF THE DEGREE | PERSONAL SKILLS OF THE WORLD OF WORK |

|---|---|

| Ethical commitment | |

Critical and self-critical ability Knowledge and application of the code of ethics | Critical sense and self-criticism Criticism of professional intervention |

| Learning ability and responsibility | |

Responsibility Capacity for analysis, synthesis, global views and application of knowledge to practice Ability to make decisions and adaptation to new situations Ability to manage failure, stress control and crisis situations | Commitment/responsibility/maturity (application of rules and regulation of own behaviour) Adaptability and flexibility Decision making, initiative, participation |

| Communicative skills | |

Ability to understand and express themselves orally and in writing, mastering the specialized language Ability to search, use and integrate Information Interpersonal communication skills positive | Expressing ideas clearly Information management, documentation, discriminate and process data with a purpose Listen-communicate, interpret language verbal and non-verbal, attitude of listen with professionals and users, empathic capacity. Assertiveness |

| Teamwork | |

Ability to collaborate with others and to contribute to a common project Ability to collaborate in interdisciplinary teams and in multicultural teams | Coordination, teamwork, networking Negotiate/know how to resign, collaborate with professionals for the benefit of users, know how to make the most of time and effectiveness of actions, knowing how to work: individually, as a team and as a network |

Elaboration from Freixa et al. (2012).

From the table above, it can be deduced that the generic communicative skills (GCSs) are those made up of the item "communicative skills", and the generic non-communicative skills (GNCSs) encompass the remainder, that is, those included in the items "Ethical commitment", "Learning ability and responsibility" and "Teamwork".

Next, Table 3 presents the generic skills asked in the questionnaire and classified according to Freixa et al., 2012.

Table 3. Generic Skills

| Generic communicative skills (GCSs) | |

|---|---|

| Ability to communicate fluently, orally and in writing, in a foreign language | Communicative skills |

| Ability to use and apply information and knowledge from the classroom to my work environment | Communicative skills |

| Ability to search for information, using computer tools, web management and data analysis | Communicative skills |

| Ability to communicate fluently, orally and in writing, in Spanish for the public presentation of works, ideas and reports | Communicative skills |

| Generic non-communicative skills (GNCSs) | |

| Critical and self-critical capacity | Ethical commitment |

| Ability to work in an interdisciplinary and/or international team | Teamwork |

| Ability to make decisions | Learning ability and responsibility |

| Ability to manage and resolve conflicts | Learning ability and responsibility |

| Ability to adapt to different work environments | Learning ability and responsibility |

| Ability to increase my self-esteem when performing my job | Learning ability and responsibility |

| Ability to know how to manage time effectively | Teamwork |

| Ability to know how to perform under pressure | Learning ability and responsibility |

| Ability to handle difficult situations at work | Learning ability and responsibility |

The specific skills (question 4 of the questionnaire) were selected and summarized from the information provided by the teaching guides of the subjects related to the accounting field of the degrees in BAM and ECO of the FEBS of the AUM.

4.1.2. Sample

The population under study corresponds to the students of the COOPERA Program taught at the FEBS at the AUM. Table 4 shows the detailed description of the students who carried out curricular internships and completed the questionnaire anonymously. The study period comprises three academic years: 2016-2017, 2017-2018 and 2018-2019. In total, 410 students participated, of which only those who had carried out internships in the Accounting area were selected, that is, a total of 279 students.

Table 4. Sample description

| Degree | |||||||

|---|---|---|---|---|---|---|---|

| BAM | ECO | Total | |||||

| Accounting profile | Non-accounting profile | Accounting profile | Non-accounting profile | Accounting profile | Non-accounting profile | ||

| Academic years | 2016-2017 | 68 | 33 | 31 | 12 | 99 | 45 |

| 2017-2018 | 58 | 32 | 30 | 10 | 88 | 42 | |

| 2018-2019 | 55 | 28 | 37 | 16 | 92 | 44 | |

| Total | 181 | 93 | 98 | 38 | 279 | 131 | |

The sample has taken into account the two internships carried out by the students in the corresponding academic years (3rd and 4th). The consideration of the two courses in our analysis attends to the very concept of experiential learning. In other words, this type of learning is a holistic process in a spiral rather than circular way, since the experience is returned in a recurrent and continuous manner and the individual undergoes a transformation along the way (Kolb, 1984, 2014). In the first internship period (3rd year) the student acquires an experience that is then repeated again in the second period (4th year), but in this case the starting point of the learning is different. Following the model proposed by Raelin (1997), before starting their internships, third-year students start with generic and specific knowledge (concrete conceptualization), which can be modified throughout the internship (experimentation) and, in turn, this will allow the acquisition of tacit knowledge. The 4th year student also starts with previous theoretical knowledge on the one hand, and with tacit knowledge reinforced by the experience of the first internship period on the other. After completing the second internship period, the student will have to develop memory (reflection) and that tacit knowledge inherent to the experience may become explicit.

All the above leads us to include the analysis of the two internships carried out by the same student in 3rd and 4th year. His perceptions on the acquisition of knowledge and skills could be different after the performance of internships in both periods (experimentation) as well as in the elucidation of the professional career. This statement is not extendable in the case of memory as an instrument of reflection (since the current evaluation system of COOPERA does not contemplate its realization in the first period). The questions in the questionnaire related to these topics were only answered by the 4th year students.

4.1.3. Factor analysis and Structural Equation Model

Factor analysis assumes that in a given context, there is a small number of latent variables or constructs, that is, unobservable that influence the broad set of observable variables. The purpose of the confirmatory factor analysis is to statistically test the capacity of the proposed factorial model to reproduce the data collected in the sample. The researcher must specify a certain number of correlated latent variables, as well as a series of observable variables to measure the latent variables (Hair et al., 1999). The first step consists of specifying the measurement model, which implies identifying the set of relationships to be examined, as well as determining how the variables should be specified in the model, taking into account that it requires a theoretical or empirical foundation. Next, the modification or re-specification of the model is carried out, and its parameters are estimated. The general fit of the model is also evaluated, analysing the extent to which the theoretical model is confirmed with the sample data. Numerous measures of goodness of fit are commonly used to evaluate the measurement model, such as the normalized chi-square, the normalized fit index (NFI), the comparative fit index (CFI), the incremental fit index (IFI) or the normalized goodness-of-fit index (AGFI). Once the general fit of the model is achieved, its reliability and convergent and discriminant validity are evaluated, as pointed out by numerous authors (Fornell & Larcker, 1981; Anderson & Gerbing, 1988, Byrne, 1994; Chau & Lai, 2003).

The reliability of the model is assessed at two levels: on the one hand, the reliability of the observable items, and on the other hand, the reliability of the constructs is valued. The reliability of the items used in the model indicates the amount of variance due to the underlying variables rather than measurement errors. A reliability greater than 0.5 is considered evidence of reliability (Chau, 1997). Other authors point out that the standardized loads for each item of the scale used should be greater than 0.7, although a value greater than 0.5 is also acceptable (Fornell & Larcker, 1981; Hair et al., 1999). The reliability of the constructs refers to the degree to which an observable variable reflects an underlying factor or variable, and a value greater than 0.7 is considered acceptable (Hair et al., 1999). Once it has been verified that the measurement scale meets the required levels of reliability, its validity is checked. Validity can be defined as the level at which the measurement scale accurately represents the concept to be measured (Hair et al., 1999). Convergent validity assesses the degree to which the measure of the items that include the same concept is correlated. A high correlation indicates that the measurement scale measures the desired concept. Therefore, the items of the measurement scale must have a strong load on the construct to be measured. Many authors suggest the use of the average variance extracted to assess convergent validity (Fornell & Larcker, 1981; Byrne, 1994). On the other hand, discriminant validity measures the theoretical difference between the different constructs, which must have low correlations with each other. Following Fornell & Larcker (1981), the discriminant validity can also be analysed using the mean variance extracted (AVE).

Through the combination of confirmatory factor analysis and analysis of causal relationships, structural equation models constitute a complete and hybrid analysis tool, which is why they have been frequently used in academic research for multivariate confirmatory analysis (Kline, 1998). The use of structural equations is most appropriate when an investigation deals with multiple constructs or latent variables. Once the reliability and validity of the measurement model have been verified, the causal relationships between the latent variables must be identified through the analysis of causal relationships so that the analysis allows for determining the direct or indirect influence of some latent variables on others and how they are related (Byrne, 2016). This work uses the IBM SPSS Amos 26.0 computer program.

5. Results

This section presents the results obtained after applying factor analysis and the structural equations technique.

The results obtained after applying the exploratory factor analysis are presented below. Table 5 shows the descriptive analysis for the generic and specific skills in accounting.

Table 5. Descriptive analysis of "generic and specific skills (accounting)"

| Skills* | Mean | Std. Deviation | Coefficient of variation (%) |

|---|---|---|---|

| v3.1 Ability to communicate fluently, orally and in writing, in a foreign language | 3.11 | 1.198 | 38.54 |

| v3.2 Critical and self-critical capacity | 4.00 | 0.751 | 18.77 |

| v3.3 Ability to work in an interdisciplinary and/or international team | 4.15 | 0.946 | 22.82 |

| v3.4 Ability to make decisions | 3.87 | 0.869 | 22.48 |

| v3.5 Ability to manage and resolve conflicts | 3.92 | 0.870 | 22.18 |

| v3.6 Ability to use and apply information and knowledge from the classroom to my work environment | 3.30 | 1.097 | 33.24 |

| v3.7 Ability to search for information, using computer tools, web management and data analysis | 4.18 | 0.783 | 18.75 |

| v3.8 Ability to communicate fluently, orally and in writing, in Spanish for the public presentation of works, ideas and reports | 3.79 | 1.067 | 28.16 |

| v3.9 Ability to adapt to different work environments | 4.27 | 0.766 | 17.94 |

| v3.10 Ability to increase my self-esteem when performing my job | 4.06 | 0.837 | 20.60 |

| v3.11 Ability to know how to manage time effectively | 4.24 | 0.697 | 16.43 |

| v3.12 Ability to know how to perform under pressure | 4.33 | 0.771 | 17.83 |

| v3.13 Ability to handle difficult situations at work | 4.16 | 0.838 | 20.15 |

| v4.1 Prepare and analyse external and internal economic-financial information for management control and decision-making, considering the international, national and sectoral economic context in which the company is immersed | 3.60 | 0.964 | 26.78 |

| v4.2 Understand and know how to apply the fundamentals of commercial law and the tax system with special incidence in the business field | 2.79 | 1.131 | 40.47 |

| v4.3 Know and apply the national accounting regulations (General Accounting Plan) and that of the European Union (International Accounting Standards, IAS/International Financial Reporting Standards, IFRS) in economic operations carried out by companies and groups of societies | 3.40 | 1.177 | 34.60 |

| v4.4 Understand the fundamentals of the valuation of companies and their assets | 3.58 | 1.052 | 29.36 |

| v4.5 Ability to apply the basic knowledge of the financial management of companies, as well as the functioning and structure of financial markets | 3.40 | 1.033 | 30.41 |

* The symbol given to each of the competencies refers to: "v": variable or item, and the number refers to the order in which it appears in the survey (Appendix 1).

As can be seen in Table 5, in general, the perceptions of students about the acquisition and development of competences after the internships obtain a higher average score of 3 points and some even exceed 4 (on a five -point scale). Except for the following "Understand and know how to apply the fundamentals of commercial law and the tax system with special incidence in the business field", which obtains an average value of 2.79. The best rated generic competency was "Ability to know how to perform under pressure" (4.33), followed by "Ability to adapt to different work environments" (4.27). And the specific competences with the highest scores awarded by the students were those related to prepare and analyse external and internal economic-financial information (3.60) followed by "Understand the fundamentals of the valuation of companies and their assets" (3.58).

The above competencies were used in a factor analysis using the principal components method with varimax rotation and Kaiser normalization. The objective of this analysis was to reduce the high number of competencies to a lower number (factors) and confirm whether they were grouped according to any classification already proposed in the bibliography. Table 64 shows that the three factors explain 54.25% of the total variance, which is an acceptable value for the social sciences. In addition, the 0.902 value of the KMO sample adequacy measure, the significance of the Bartlett sphericity test, together with the Cronbach alpha coefficients, indicate that the results analysed below are adequate, and therefore, they can be grouped into the competencies considered under three types. Factor one is made up of 9 items, which refer to "non-communicative generic skills" (GNCSs). Factor two is correlated with "Generic Communication Skills" (GCSs). Finally, the third factor, which includes 5 items, focuses on "Specific Accounting Skills" (SASs).

Table 6. Factor analysis for "generic and specific skills (accounting)"

| Skills | Factor | ||

|---|---|---|---|

| GNCSs | GCSs | SASs | |

| v3.12 Ability to know how to perform under pressure | 0.807 | ||

| v3.13 Ability to handle difficult situations at work | 0.803 | ||

| v3.11 Ability to know how to manage time effectively | 0.730 | ||

| v3.10 Ability to increase my self-esteem when performing my job | 0.666 | ||

| v3.5 Ability to manage and resolve conflicts | 0.661 | ||

| v3.4 Ability to make decisions | 0.587 | 0.455 | |

| v3.2 Critical and self-critical capacity | 0.546 | ||

| v3.9 Ability to adapt to different work environments | 0.520 | ||

| v3.3 Ability to work in an interdisciplinary and/or international team | 0.500 | 0.407 | |

| v3.8 Ability to communicate fluently, orally and in writing, in Spanish for the public presentation of works, ideas and reports | 0.765 | ||

| v3.1 Ability to communicate fluently, orally and in writing, in a foreign language | 0.738 | ||

| v3.7 Ability to search for information, using computer tools, web management and data analysis | 0.545 | ||

| v3.6 Ability to use and apply information and knowledge from the classroom to my work environment | 0.540 | ||

| v4.5 Ability to apply the basic knowledge of the financial management of companies, as well as the functioning and structure of financial markets | 0.818 | ||

| v4.4 Understand the fundamentals of the valuation of companies and their assets | 0.804 | ||

| v4.3 Know and apply the national accounting regulations (General Accounting Plan, PGC) and that of the European Union (International Accounting Standards, IAS/International Financial Reporting Standards, IFRS) in economic operations carried out by companies and groups of societies | 0.761 | ||

| v4.1 Prepare and analyse external and internal economic-financial information for management control and decision-making, considering the international, national and sectoral economic context in which the company is immersed | 0.701 | ||

| v4.2 Understand and know how to apply the fundamentals of commercial law and the tax system with special incidence in the business field | 0.687 | ||

| % of variance explained | 37.756 | 10.069 | 6.421 |

| % cumulative variance | 37.756 | 47.825 | 54.246 |

| Cronbach's alpha | 0.854 | 0.641 | 0.809 |

| KMO and Bartlett's Test | |||

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy. | 0.902 | ||

| Bartlett's Test of Sphericity | Approx. Chi-Square | 2049.234 | |

| df | 153 | ||

| Sig. | 0.000 | ||

Next, following the objective of the study, the same previous analyses are repeated for the evaluation of the impact of the internships in the reflection of the learning acquired through the elaboration of the report and in the elucidation of the choice of the future career professional.

In Table 7, it can be observed that, in general, the preparation of the report is not well valued in terms of its usefulness, bordering on approval in all sections. Specifically, the aspects that are least valued and are also the ones with the greatest dispersion are those that refer to controlling their progress, reflecting on their experience and understanding what they have learned.

Table 7. Descriptive analysis for “report” (reflective learning (RL))

| Report (RL)* | Mean | Std. Deviation | Coefficient of variation (%) |

|---|---|---|---|

| v2.2.1 Memory has allowed you to reflect on your experiences during the internship. | 3.05 | 1.179 | 38.58 |

| v2.2.2 Memory has helped you monitor your progress. | 2.88 | 1.200 | 41.62 |

| v2.2.3 Memory has helped you remember what you learned. | 3.18 | 1.268 | 39.83 |

| v7.11 The performance of the memory of internships has allowed me to reflect on my experience and understand what I learned. | 2.93 | 1.224 | 41.83 |

* The symbol given to each of the questions referring to the "Report" refers to: "v": variable or item and the number refers to the order in which it appears in the survey (Appendix 1).

When applying the factor analysis (Table 8), it is observed that the four items can be grouped into a single factor (it has a high KMO and a Cronbach's alpha of 0.918) that is highly correlated with the reflective aspects that memory practice must have.

Table 8. Factor analysis for "report"

| Report (RL) | Factor | |

|---|---|---|

| RL | ||

| v2.2.2 Memory has helped you monitor your progress. | 0.924 | |

| v2.2.1 Memory has allowed you to reflect on your experiences during the internship. | 0.907 | |

| v2.2.3 Memory has helped you remember what you learned. | 0.889 | |

| v7.11 The performance of the memory of internships has allowed me to reflect on my experience and understand what I learned. | 0.866 | |

| % of variance explained | 80.361 | |

| Cronbach's alpha | 0.918 | |

| KMO and Bartlett's Test | ||

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy. | 0.842 | |

| Bartlett's Test of Sphericity | Approx. Chi-Square | 817.051 |

| df | 6 | |

| Sig. | 0.000 | |

Finally, the aspects that are related to the future choice of the student's professional career are analysed once they have completed their studies. The results are collected in Tables 9 and 10.

In Table 9, it can be observed that the opinions in which they agree the most are also those with the highest average score. For example, after completing the internship, the students have a clearer vision of their choice of their professional future (3.89). However, there is an assessment that does not reach the approved level, although those who are thinking about choosing an accounting profession present a strong dispersion.

Table 9. Descriptive analysis for "future election (general and accounting)"

| Future election (general and accounting)* | Mean | Std. Deviation | Coefficient of variation (%) |

|---|---|---|---|

| v7.8 I have come to have a clearer vision of my choice about my professional future | 3.89 | 1.085 | 27.92 |

| v7.10 I have come to know more clearly and realistically the accounting profession and my future professional career, if I finally decide to dedicate myself to the accounting profession | 3.84 | 1.189 | 30.96 |

| v8.1 I know what to expect from my future career after graduation | 3.84 | 0.987 | 25.73 |

| v8.2 I am looking forward to a professional career in accounting | 2.82 | 1.247 | 44.26 |

| v8.3 I am convinced of my career choice (general election) | 3.79 | 1.118 | 29.48 |

| v8.4 I am thinking of pursuing an alternative career to accounting | 2.89 | 1.317 | 45.53 |

* The symbol given to each one of the questions referring to the “Future Choice (general and accounting” refers to: “v”: variable or item and the number refers to the order in which it appears in the survey (Appendix 1).

When performing the factor analysis with these items (Table 10), the results allow us to conclude that two factors that explain 57.16% of the total variance. In addition, the value 0.746 of the sample adequacy measure, together with the Cronbach coefficients, indicates that the results are adequate and that, therefore, the "Future election" can be grouped into two factors. The first factor is composed of three items, which refer to the general future election (GFE). The second factor is correlated with the future election in the field of accounting (AFE).

Table 10. Factor analysis for "future election (general and accounting)"

| Future election (general and accounting) | Factor | |

|---|---|---|

| GFE | AFE | |

| v8.3 I am convinced of my career choice (general election) | 0.756 | |

| v7.8 I have come to have a clearer vision of my choice about my professional future | 0.751 | |

| v8.1 I know what to expect from my future career after graduation | 0.732 | |

| v8.4 I am thinking of pursuing an alternative career to accounting | -0.803 | |

| v8.2 I am looking forward to a professional career in accounting | 0.404 | 0.609 |

| v7.10 I have come to know more clearly and realistically the accounting profession and my future professional career, if I finally decide to dedicate myself to the accounting profession | 0.408 | 0.527 |

| % of variance explained | 39.108 | 18.049 |

| % cumulative variance | 39.108 | 57.157 |

| Cronbach's alpha | 0.680 | 0.526 |

| KMO and Bartlett's Test | ||

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy. | 0.746 | |

| Bartlett's Test of Sphericity | Approx. Chi-Square | 249.418 |

| df | 15 | |

| Sig. | 0.000 | |

After performing the factor analysis, it is verified that each factor (GNCSs, GCSs, SASs, RL, GFE and AFE) is measured by at least three items, a requirement for the proper functioning of the model (Luque, 2000). In addition, almost all of the factors present values higher than 0.7 (Cronbach's alpha), which guarantees the reliability of the constructs. The only ones that do not reach 0.7 are the "future accounting choice" and the "general communication competencies". The reason may be the inclusion of an item that in turn was correlated with various constructs. However, especially in the construct "Accounting Future Choice", the value of alpha is poor, although it is acceptable5.

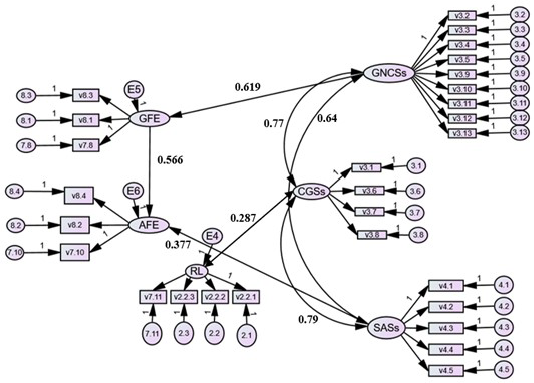

Next, Table 11 and the Figure 2 presents the estimates and the structural equation model.

Table 11. Factor loading of latent variables, indicators of reliability and internal consistency

| Indicators | Constructs | Lambda | Standardized Lambda | Composite Reliability | AVE |

|---|---|---|---|---|---|

| v3.2 | Generic non-communicative skills (GNCSs) | 1,000 | 0.625 | 0.882 | 0.455 |

| v3.3 | 1,320 | 0.619 | |||

| v3.4 | 1,336 | 0.706 | |||

| v3.5 | 1,396 | 0.754 | |||

| v3.9 | 1,017 | 0.612 | |||

| v3.10 | 1,171 | 0.620 | |||

| v3.11 | 0.968 | 0.623 | |||

| v3.12 | 1,268 | 0.723 | |||

| v3.13 | 1,425 | 0.762 | |||

| v3.1 | Generic communicative skills (GCSs) | 1,000 | 0.391 | 0.655 | 0.331 |

| v3.6 | 1,492 | 0.657 | |||

| v3.8 | 1,276 | 0.551 | |||

| v3.7 | 1,065 | 0.639 | |||

| v4.1 | Specific Accounting Skills (SASs) | 1,000 | 0.646 | 0.836 | 0.506 |

| v4.2 | 1,122 | 0.640 | |||

| v4.3 | 1,293 | 0.687 | |||

| v4.4 | 1,385 | 0.818 | |||

| v4.5 | 1,223 | 0.751 | |||

| v2.2.1 | Reflective learning (RL) | 1,000 | 0.875 | 0.921 | 0.745 |

| v2.2.2 | 1,075 | 0.911 | |||

| v2.2.3 | 1,096 | 0.865 | |||

| v7.11 | 0.908 | 0.797 | |||

| v7.8 | General future election (GFE) | 1,000 | 0.547 | 0.704 | 0.448 |

| v8.1 | 1,341 | 0.781 | |||

| v8.3 | 1,236 | 0.659 | |||

| v7.10 | Accounting Future Election (AFE) | 1,000 | 0.630 | 0.308 | 0.256 |

| v8.2 | 0.939 | 0.573 | |||

| v8.4 | -0.348 | -0.205 |

χ2(315): 1.093, p-value: 0.124; GFI: 0.912; RMSEA: 0.018; AGFI: 0.886; CFI: 0.938.

For analysis of the reliability and internal consistency of the model, the composite reliability indices and the values of the extracted variance (AVE) were calculated. Compound reliability is a measure of the internal consistency of the constructs (Bagozzi & Yi, 1988), so that values greater than 0.5 would confirm the internal consistency, except for the one that refers to the "accounting future election" factor as already commented with anteriority. Therefore, internal consistency is confirmed since the standardized lambda coefficients exceed the value of 0.5, with the exception of items v3.1 and v8.4. Regarding the discriminant validity, which measures the precision with which the analysis instrument represents the variables, the values of the extracted variance are also considered acceptable, since they exceed the value 0.5 (Hair et al., 1999; Wu & Lin, 2000) with the exception of generic communication skills (GCSs) and accounting future election (AFE).

In relation to the structural adjustment of the model, a series of measures were analysed to assess the adjustment of the proposed conceptual model. The chi-square coefficient, as well as the degrees of freedom, are generally used to evaluate the models (Qiu, 2003), as well as other indices of goodness of fit, such as GFI, AGFI or RMSEA. According to the results obtained for the model, the chi-square obtains a value of 344.173 (DF = 315, p = 0.124) and a goodness of fit index (GFI) of 0.912, which can be considered a reliable indicator of the model (Bollen, 1989; Hair et al. 1999). The RMSEA (root mean square error of approximation) reaches a value of 0.018, which is close to 0.05 and therefore evidence of an acceptable fit of the general model (Bagozzi & Yi, 1988). The incremental adjustment measures, as well as the parsimony measures, also indicate a good adjustment since the former are all very close to 0.9 or very close, as is the case for the AGFI index (Hair et al. 1999).

Figure 2. Estimated Structural equation model

The estimated model (Figure 2) shows the comprehensive and related evaluation of the impacts that the internship has had on the students. Analyzing the results obtained using the theory of experiential learning and aligned with the model proposed by Raelin (1997), it is observed that the internships (experimentation) have had an impact on generic and specific competences in the accounting area. These students started with previous knowledge received during the degree (conceptualization) and that after carrying out internships this has been reinforced, causing them, in turn, to acquire tacit knowledge. In addition, this knowledge acquired through the competences analyzed after the experience (internships) has influenced the crystallization and elucidation of the students' professional future: i) Generic non-communicative skills directly and positively influence future elections by 61.9%; ii) The general future election has a significant and positive impact (56.6%) on the choice of a profession related to the accounting area; and iii) The acquisition of specific skills in the accounting field has a positive and significant impact on the choice of an accounting profession in the future (37.7%). However, students do not perceive that reflection, materialized through the development of memory, helps in bringing the tacit knowledge inherent in the experience to the surface. The completion of the report has no impact on professional choice, and it seems that it is detached from the model except for the positive, albeit low, impact existing between the acquisition of generic communication skills and the preparation of the report (28.7%).

6. Conclusions and implications

The creation of the European Higher Education Area served as a frame of reference for the educational reforms that many countries began in the early years of the 21st century. The main measures contemplated within the EHEA were the change in teaching methodologies aimed at lifelong and competence-based learning. The model proposed by Kolb (1984) on experiential learning can facilitate understanding of the methodological keys that served as the basis for developing the European model of lifelong learning. One of the subjects that promotes experiential learning is curricular internships (Kolb, 2014). These allow for students to exchange between the academic and professional world, thus working on the transversal and specific skills of their degrees. Furthermore, internships offer a realistic job preview for the accounting student (Beck & Halim, 2008). In fact, authors such as Roth & Roth (1995) point out that one of the advantages of such previews was the reduction of the turnover costs involved in replacing recruits who discover that the accounting profession is not for them.

Universities should ensure that curricular internships are meaningful learning experiences for their students (Bukaliya & Marondera, 2012). Internships have played an increasingly important role in education over the last decade (Tackett et al., 2001). In Spain, it is considered essential and compulsory for university students to carry out curricular internships. This work analyses the impact, individual and interrelated, that curricular internships have, in the accounting field, on BAM and ECO students at the Autonomous University of Madrid. The information necessary to carry out the analysis was obtained through a questionnaire presented to all students at the end of their internship periods. The questionnaire was completed anonymously by a total of 410 students, of which only those who had carried out internships in the accounting area (279 students) were selected. The fact that the questionnaire was distributed to all students (including those with a non-accounting profile) was a limitation of our work. For all students to be able to answer the questionnaire, general questions were included, which limited the inclusion of more specific items from the accounting field. This meant that the reliability of some constructs, as already mentioned in the previous section, was weak. The information provided by the completed surveys was analysed through factor analysis techniques and structural equation models. The estimated model (Figure 2) shows the comprehensive evaluation of the impact that internships in accounting have on students through the acquisition of skills, reflection on the learning acquired through the realization of the report, and the clarity of choosing your professional future. The interpretation of the model is explained using the theory of experiential learning following the model proposed by Raelin (1997). The students, before starting their corresponding internship periods, started with some knowledge acquired throughout the degree (conceptualization). This knowledge has been reinforced during the development of internships (experimentation) and tacit knowledge has emerged. The results obtained in this work, in line with previous studies (Taylor, 1988; Beck & Halim, 2008 and Muhamad et al., 2009) show that practices have had an impact both on learning in terms of generic and specific competences and on the crystallization of their professional future. However, the students have not perceived that the realization of memory has helped them to reflect and thus emerge from the tacit knowledge inherent to the experience.

The explanation of why the students do not perceive the elaboration of the report as useful could lie in the structure and in the aims pursued. In Spain, students of curricular internships upon completion must prepare and deliver a final report to their academic tutor. This report has two purposes: one purpose is to record the learning achieved with the internships, and the second is to evaluate and qualify the student (Royal Decree 592/2014). With curricular internships, it is intended that the student acquires, as a consequence of reflection, broader learning than that which she would obtain from the mere performance of the activities developed (Raelin, 1997). For this reason, from the point of view of learning, reports should be an introspective tool with which the student, after completion of an internship, connects reflection and action, generating significant knowledge from the association of their previous personal material and the new experience that gives meaning to what has happened, which will constitute a starting point for new learning (Lukinsky, 1990). Unfortunately, reality has shown us that in many cases, this is not the case and that the report is a simple record of the events that occurred during practice. This reality may be due to the dual purpose of the report, since its evaluative objective will inadvertently inhibit the learning that must promote the report, blocking reflection. Treating reports or diaries that simultaneously cover different purposes in the same way can lead to error, confusion and memory not fulfilling the role of reflective practice (Boud, 2001).

This work contributes to the existing literature by analysing the impact of carrying out curricular internships focusing on students. However, doing internships also has an impact on two other stakeholders: parent institutions and employers (Cook et al., 2004; Lam & Ching, 2007). Therefore, in future work, the impact that internships have on the other two agents involved could be analysed.

Appendix 1

Survey on the Evaluation of Curricular Internships